What are the best private market opportunities in food processing? This playbook covers M&A trends, public and private company benchmarks, active financial sponsors, and target-rich segments including automation, packaging, cold chain logistics, waste reduction, and equipment.

Everybody has to eat. That’s why food processing is a $4T industry. It affects every household in the world, every single day.

For private market dealmakers, the infrastructure that powers the industry has a smorgasbord of opportunities. Automation systems, packaging technology, cold chain logistics, waste reduction, and processing equipment are quietly generating some of the most attractive returns in the middle market.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the food processing market, including:

How the industry is fragmented

Which market segments are seeing the most growth

Where to find deep geographic pockets of opportunity

Recent acquisitions in the space

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Key Insights into the Food Processing Industry

Strategic buyers have dominated food processing M&A over the last decade.

Automation is the fastest-growing food processing segment in the private sphere, with an average annual revenue growth rate of 18.7% — well above the 13.5% industry average.

The vast majority of the food processing industry is privately owned. Independent companies account for 28% of the landscape, while VC-backed and PE-backed companies at 14% and 9%, respectively. This points to a deep pool of first-time-seller opportunities for dealmakers.

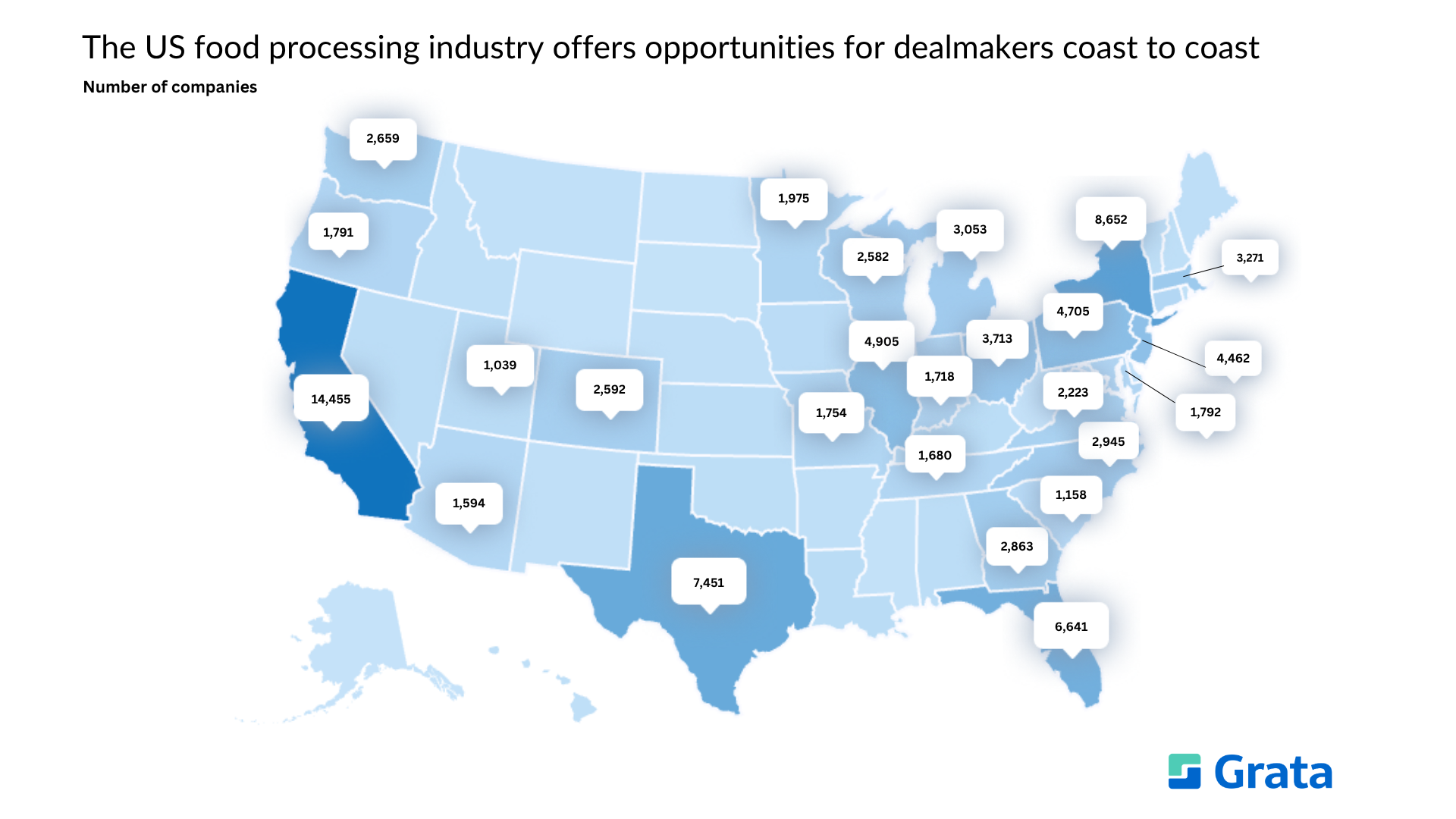

The US leads the global food processing market with approximately 107,000 companies, nearly 5x the size of the next-largest market. California, Texas, and New York are the top three states by company count.

M&A Trends in the Food Processing Industry

Transactions

Source: Grata

Deals in the food processing space have nearly doubled over the last decade, from 718 in 2017 to over 1,300 in 2025. Strategic buyers have dominated the scene due to a number of key factors, including:

Synergies are immediate and tangible. Acquiring companies can plug new brands directly into existing distribution networks, retail relationships, and manufacturing capacity.

There is no exit deadline. Strategic buyers hold permanently, so they can more easily absorb assets that need time to integrate or grow. PE firms are constrained by a 5–7 year hold period and need a credible exit path from day one.

Big food companies are always buying and selling. Heavy hitters like General Mills, Conagra, and Nestlé are constantly pruning slow growth brands and acquiring in high-growth categories. This creates a constant deal flow that isn't tied to market cycles.

Consumer trends move faster than R&D cycles. By the time a large food company builds a specialty food brand organically, the trend has moved on. Acquiring allows them to keep up.

Food processing is operationally demanding for PE. Unless a financial sponsor has manufacturing expertise, the capital-intensive assets, thin margins, and operational complexity of running food processing plants tend to compress returns.

Most Active Financial Sponsors

Source: Grata

PAI Partners tops the list of most active financial sponsors in the food processing industry with 72 relevant acquisitions. Many of its deals in the space are related to co-manufacturing, which is when a company outsources the production of its food products to a third party.

Most Active Strategic Acquirers

Source: Grata

Grupo Bimbo leads all strategic acquirers with 47 relevant acquisitions. The majority of its deals in the food processing industry are food brands and manufacturers.

Food Processing Industry Overview

Market Distribution

Geography

Source: Grata

The US, the UK, and Germany lead the global food processing market by number of companies. Other key players include France, Canada, and Australia.

For sponsors with multi-geography mandates, the UK and Germany offer mature markets with strong regulatory frameworks and fragmented middle-market ecosystems that parallel the US opportunity.

Source: Grata

For US-focused dealmakers, there is no shortage of opportunity in the food processing industry. Here are some key factors and regions to consider:

California dominates in terms of sheer volume, with 14,455 food processing companies. The state’s target density makes it an appetizing place for roll-up strategies, though competition for quality assets is fierce. California's position as the country's largest agricultural producer creates high demand for processing equipment, packaging, and cold chain infrastructure throughout the Central Valley and along the coast.

Texas and Florida are standout growth markets. The combination of population growth, more food manufacturing companies moving south, and expanding distribution infrastructure make both states prime targets for platform builds and add-on acquisitions. Texas, in particular, has seen meaningful investment in food manufacturing capacity as companies diversify their supply chains away from coastal hubs.

New York is a Northeastern hub for specialty food distribution, food packaging innovation, and foodservice supply chain. The concentration of companies across New York, New Jersey, and Pennsylvania makes the area well-suited for regional roll-ups.

The Midwest continues to be the backbone of US food processing. The heartland boasts heavy concentrations of processing equipment manufacturers, automation firms, and supply chain companies. While Wisconsin and Minnesota are slightly smaller markets, they have outsized representation in dairy processing equipment and cold storage.

Food processing in the Southeast is seeing impressive growth. Florida, Georgia, and the broader Sun Belt are attracting new food manufacturing investment as companies follow population migration patterns south and seek lower operating costs.

Ownership

Source: Grata

The food processing industry is highly fragmented, with the overwhelming majority of companies being privately owned. Public companies and their subsidiaries represent just 34% by employee share despite their outsized revenue footprints.

Currently, there are over 200,000 food processing companies that are ripe for acquisition.

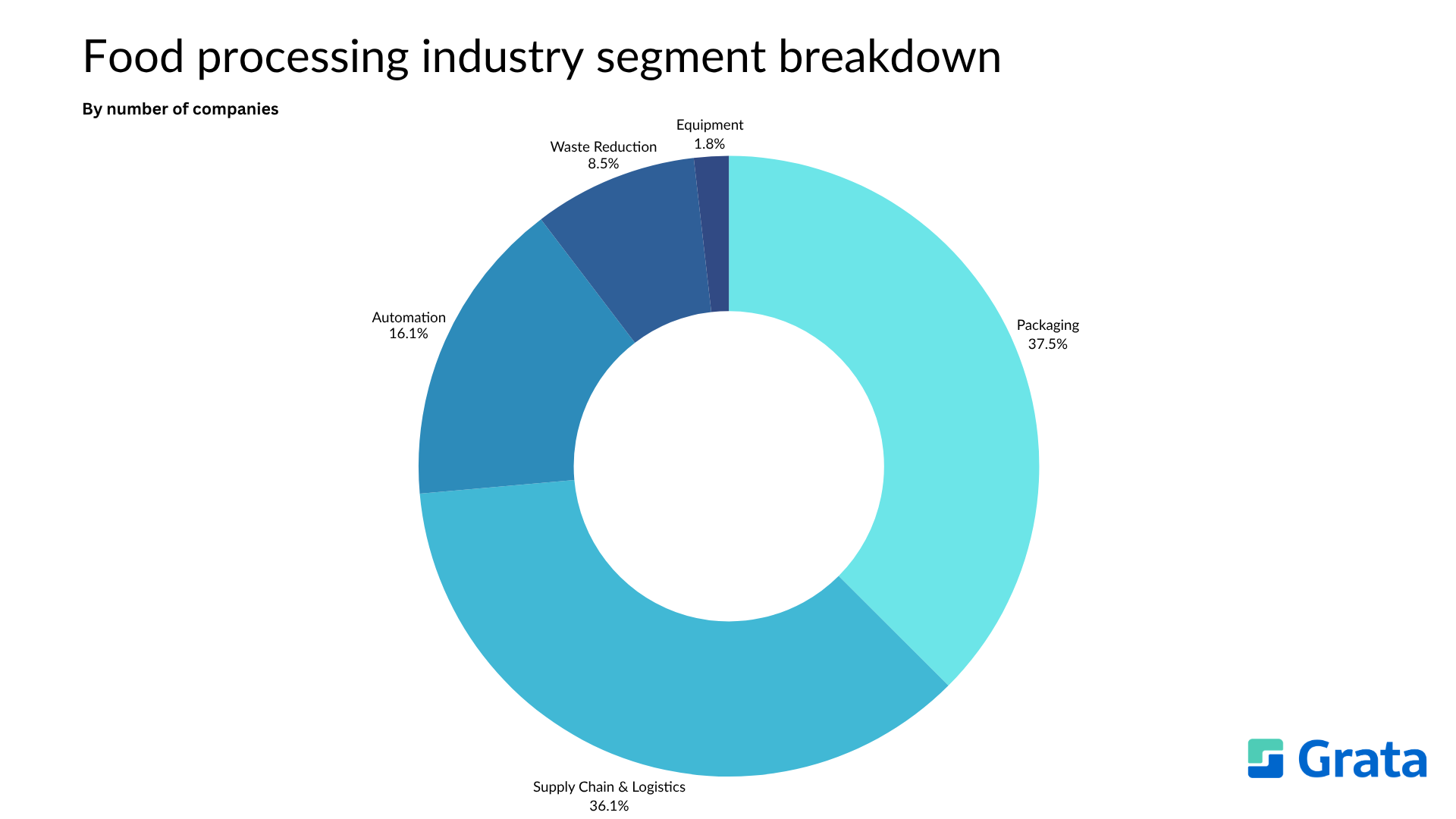

Segment Distribution

Source: Grata This report focuses on the following segments of the food processing industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

Automation

Packaging

Supply Chain & Logistics

Waste Reduction

Equipment

Food Processing Public Comparables

Source: Grata

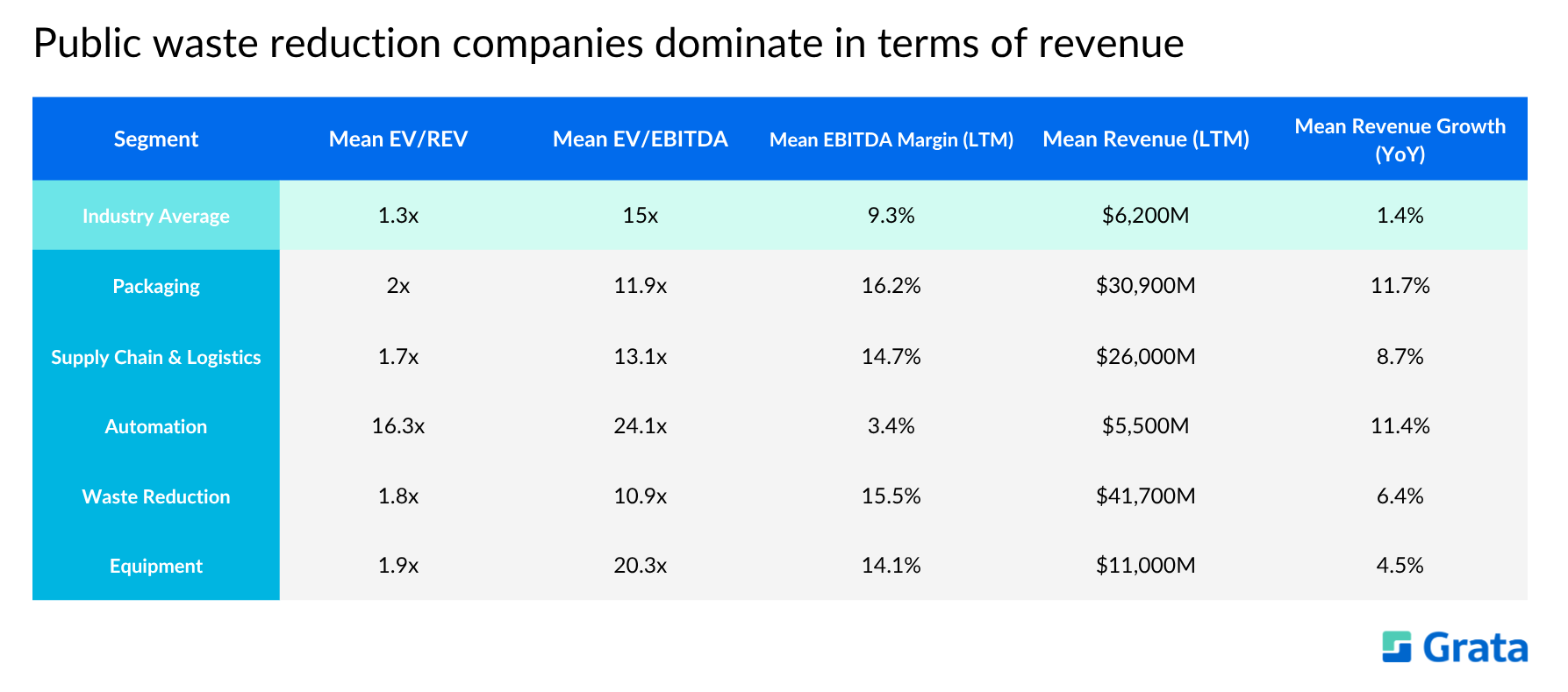

In the public realm, waste reduction companies see the most average revenue by far, at $41.7B. Players in this space tend to serve several industrial and manufacturing industries beyond food and beverage. They process enormous amounts of waste, and the economics of converting that waste into fuel or feed is well established. These companies also operate on long-term contracts, large physical infrastructure, and commodity sales rather than brand innovation.

Packaging companies lead the pack in terms of growth, an average rate of 11.7%. These companies are also earning a healthy average margin of 16.2%. Regulations play a key role here: governments across the US and Europe are forcing food companies to switch to recyclable and compostable packaging, which means packaging suppliers are seeing a wave of new orders that isn't likely to dissipate any time soon.

Meanwhile, supply chain and logistics companies are growing steadily at 8.7% with 14.7% margins. The fastest-growing piece of this segment is cold chain — the refrigerated trucks, warehouses, and distribution networks that keep perishable food safe between the factory and the store shelf. Demand for online grocery, meal kits, and ready-to-eat foods has grown dramatically, driving up demand for cold chain infrastructure in tandem.

Automation companies trade at the highest EBITDA multiples, though their current average margins are thin (3.4%). Food manufacturers are struggling to hire. In 2024, there were over 615,000 unfilled jobs in the US food manufacturing space alone. Companies that can't find workers are buying machines instead, and that shift is accelerating.

Equipment companies offer the best combination of high multiples (20.3x EBITDA) and real, current profitability (14.1% margins). Dealmakers should look to equipment businesses that ongoing maintenance contracts, spare parts, and upgrades in addition to machinery for steady revenue year after year.

Food Processing Private Comparables

Source: Grata

In the private sphere, the automation segment is growing the fastest by far, at an average rate of 18.7% per year. Most are founder-owned, and they specialize in a particular niche. Think: a company that makes vision inspection systems for meat plants, or robotic pick-and-place equipment for bakeries. Companies in this space are growing quickly with very little outside capital, which could make for excellent first-time seller opportunities for players looking to consolidate the space.

Supply chain and logistics companies see the second-fastest average growth rate at 11.5%. With operational scale and predictable customer relationships, these businesses could benefit from a PE owner investing in better technology and geographic expansion.

Meanwhile, the packaging sector leads the private food processing industry in terms of revenue by far. This segment has also raised the most outside capital, with an average of $1.2B. This signals that the segment is already well-covered by institutional investors. The remaining opportunity is in smaller regional packaging companies that haven't been acquired yet and are under pressure to help their food manufacturer customers become more sustainable.

That brings us to the wase reduction segment, which sits at the opposite end of the revenue spectrum with just $4.7M on average. This is also the only segment seeing negative growth. Most companies here are early-stage businesses still figuring out how to profitably turn food factory byproducts into usable materials like animal feed or compost. Still, this sector is worth paying attention to, especially for corporates. Food giants like Nestlé, Tyson, and Conagra have made public commitments to reduce food waste across their operations to comply with regulators and reduce costs. Acquiring a waste reduction company, or signing a long-term contract with one, lets them turn a disposal cost into a revenue stream.

Notable Acquisitions in the Food Processing Industry

Source: Grata

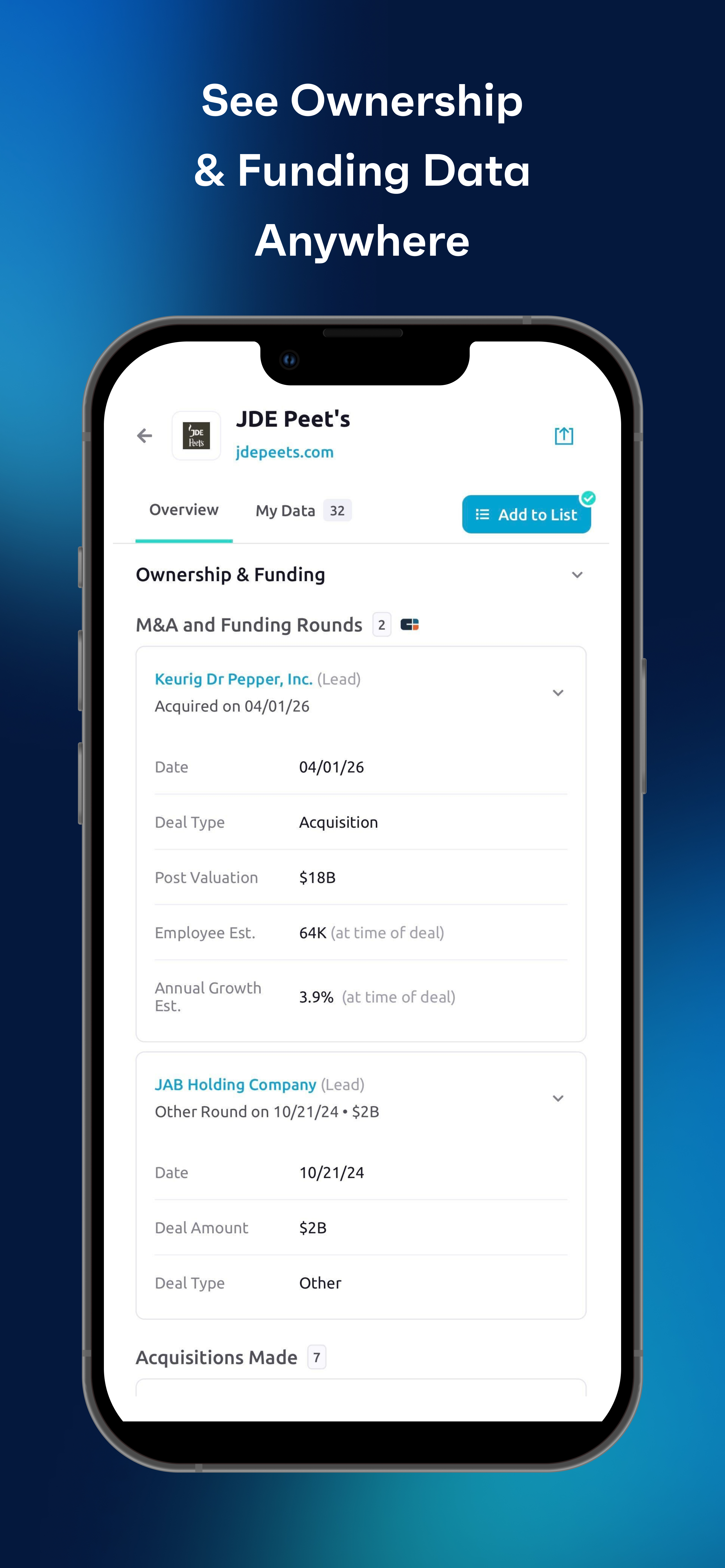

Keurig Dr Pepper Acquires JDE Peet's

In April, Keurig Dr Pepper acquired JDE Peet's, one of the largest coffee and tea companies in the world, for an enterprise value of $18.4B. The deal significantly expands Keurig Dr Pepper's international footprint and creates one of the most comprehensive hot beverage platforms globally. JDE Peet's brings a portfolio of iconic brands including Peet's Coffee, Douwe Egberts, Jacobs, and Tassimo across more than 100 countries.

If you're an investor interested in companies similar to JDE Peet's, try these:

Learn more about this acquisition — or any of the others listed below — anytime, anywhere using the latest version of the Grata Go mobile app. Get all of the ownership and investment data you need right in the palm of your hand.

International Paper Acquires North Pacific Paper Company

Later in April, International Paper acquired North Pacific Paper Company for $360M. North Pacific offers a broad range of high-quality papers, including recyclable, low-carbon packaging and graphic papers. The deal consolidates International Paper's position in the North American paper market and adds significant production capacity as it reshapes its portfolio following its acquisition of UK-based packaging group DS Smith.

If you're an investor interested in companies similar to North Pacific Paper Company, try these:

Also in April, Refresco, the world's largest independent beverage manufacturer, acquired SunOpta, a leading producer of plant-based and organic beverages, for $1.1B. The acquisition adds oat milk, almond milk, and organic juice production to Refresco's significant contract manufacturing capabilities.

If you're an investor interested in companies similar to SunOpta, try these:

In May, The Marzetti Company acquired Bachan's, a rapidly growing Japanese barbecue sauce brand, for $400M. Bachan's has been one of the standout specialty condiment success stories of recent years, quickly expanding from DTC to national retail distribution.

If you're an investor interested in companies similar to Bachan's, try these:

In May, Denmark-based biscuit and snack manufacturer Bisca A/S acquired East Coast Bakehouse, an Ireland-based baked snacks producer, for $15.2M. The deal reflects the continued cross-border consolidation trend in the better-for-you snack category, as European strategics seek to build out their portfolio of health-oriented formats.

If you're an investor interested in companies similar to East Coast Bakehouse, try these:

Also in May, Israel-based specialty ingredients group Turpaz acquired Phoenix for $100M, adding flavor and ingredient solutions for food manufacturers to its portfolio.

If you're an investor interested in companies similar to Phoenix, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the food processing industry:

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

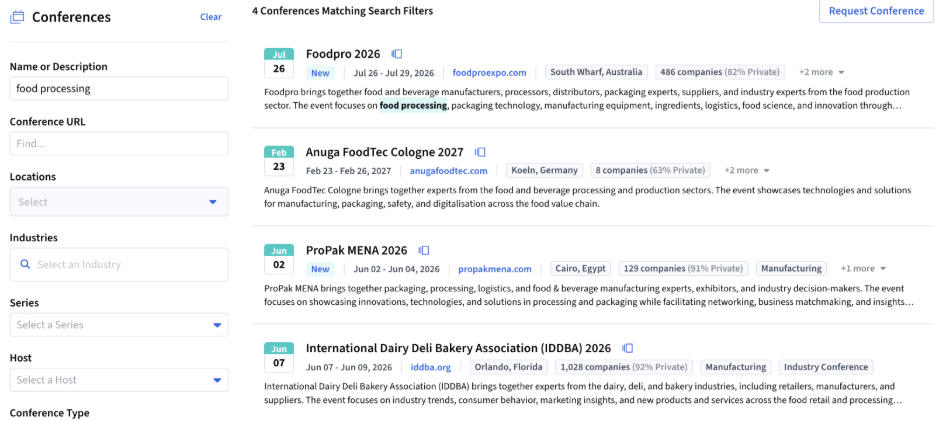

Food Processing Industry Conferences

Grata makes it easy for dealmakers to find conferences, events, and trade shows in their industries. See attendee lists so you can set up meetings beforehand and make the most of your travel time. Check out which companies attended past events to find more potential targets.

Here are a few of the events related to the food processing industry that dealmakers can find and track in Grata:

Source: Grata

Get the Most Out of the Playbook

If you’re an investor interested in making moves in the food processing space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

From market trends to career advice, Grata’s content fuels smarter decisions.

Sourcing

Why Proprietary Deal Flow Is Getting Harder — and How Leading Teams Are Adapting

Proprietary deal flow is getting harder as generalist AI closes the access gap. See how verified private-market data and Seller Intent help dealmakers source before the competition does.

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

Hidden Gems: Actionable, Undiscovered Opportunities in the HVAC Industry

Discover 79 undiscovered HVAC companies with high Seller Intent scores. See ownership, geographic, and sector breakdowns from Grata's proprietary private market data.

.webp)

.png)

.png)

.png)

.webp)