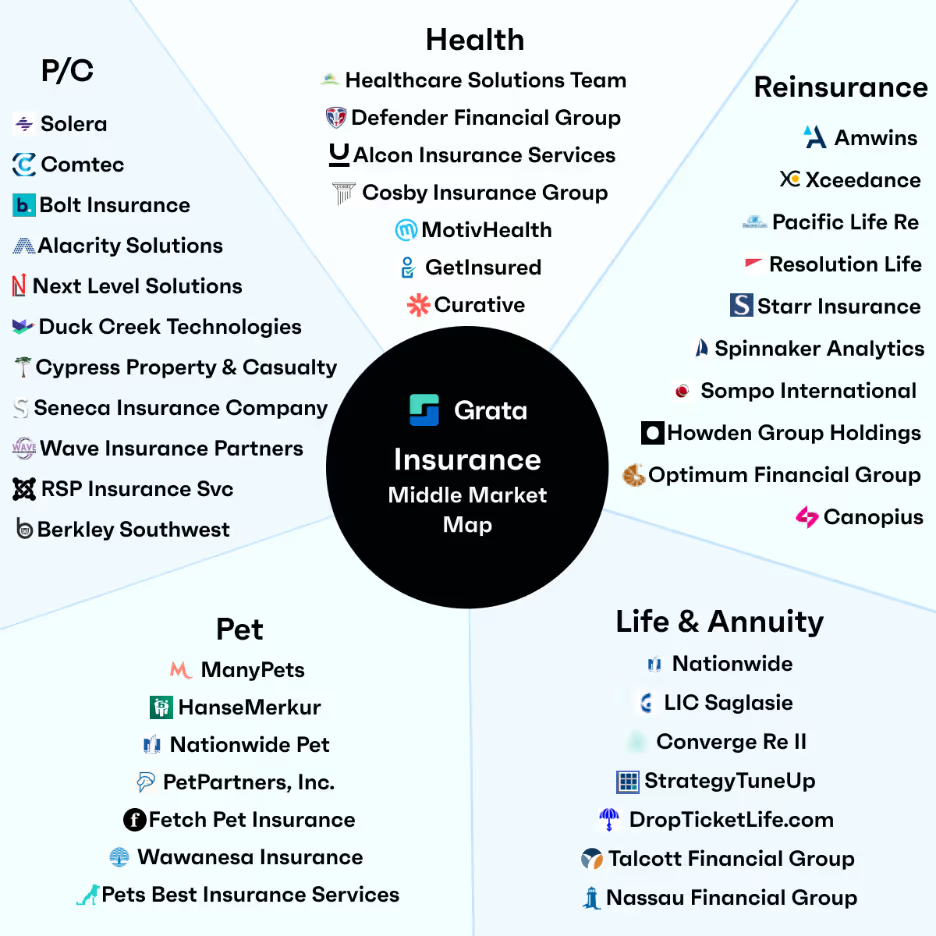

Learn all of the trends that private market dealmakers need to know about the insurance industry, from how the space is fragmented to high-growth sectors to geographical pockets of opportunity.

2026 is shaping up to be a big year for M&A activity in the insurance industry. Technology is a major force driving the momentum.

Insurers are acquiring AI and data analytics tools to streamline underwriting and claims processing. With digitization spreading across industries, insurers are snapping up firms offering expertise and solutions in specialized risk management. Additionally, insurance companies are leveraging M&A to consolidate and improve profitability amid rising costs.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the insurance market, including:

How the industry is fragmented

Which segments are seeing the most growth

Where to find pockets of opportunities around the world

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Key Insights into the Insurance Industry

M&A activity in the insurance industry has surged in the last 10 years driven by emerging AI and analytics solutions and a need for scale.

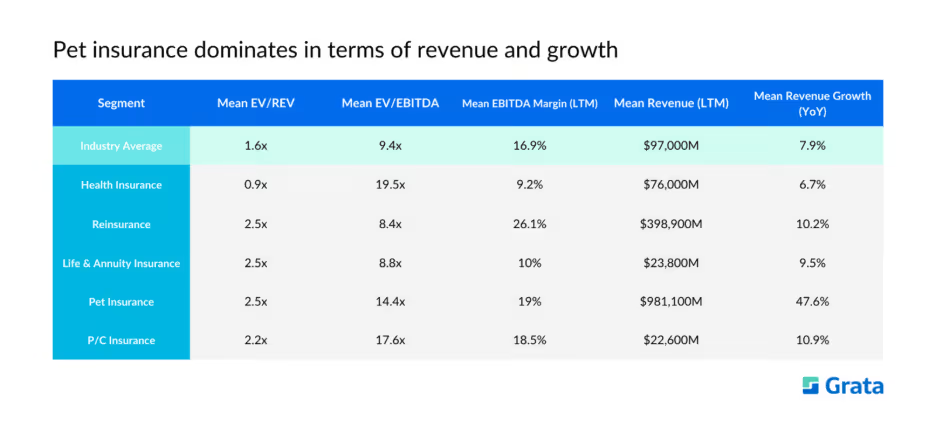

Pet insurance companies in both the public and private spheres dominate the industry in terms of average annual growth.

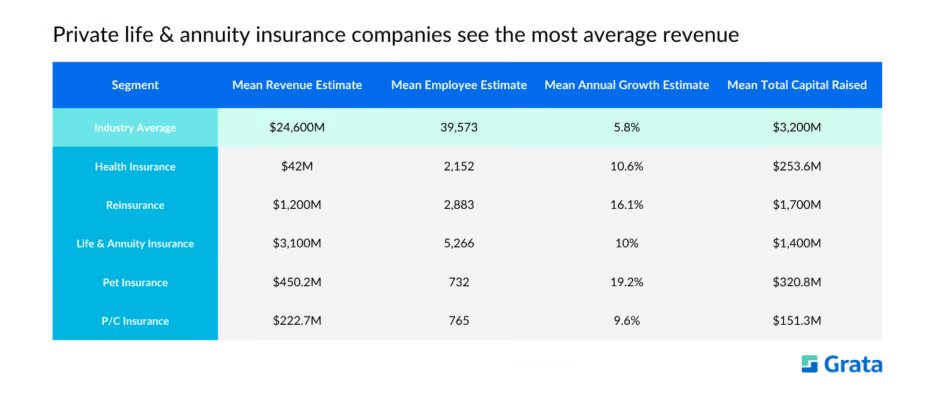

Private life & annuity insurance companies see the most average revenue by far.

US-focused dealmakers should look to states like Arizona, Virginia, and Indiana, which have some of the country’s highest rankings for favorable regulatory environments, low litigation rates, and ease of rate approvals.

M&A Trends in the Insurance Industry

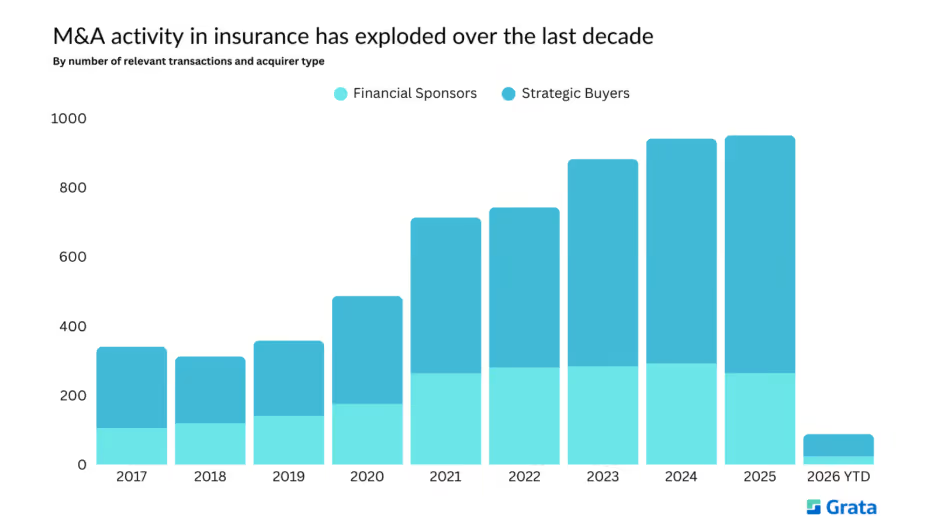

Transactions

Source: Grata

M&A transactions have increased dramatically since 2018. Growing digitization is a key factor behind the surge. Insurers have been particularly drawn to new AI, automation, and data analytics tools that help streamline processes.

Societal and business risks from macro factors like cybersecurity, ransomware, and climate change have also risen over the last decade, driving insurers to acquire firms that offer specialized risk solutions.

Private equity firms have also been extremely active in the space. They have largely targeted managing general agents (MGAs) and managing general underwriters (MGUs) to support building platforms and expansion into new, high-growth product areas.

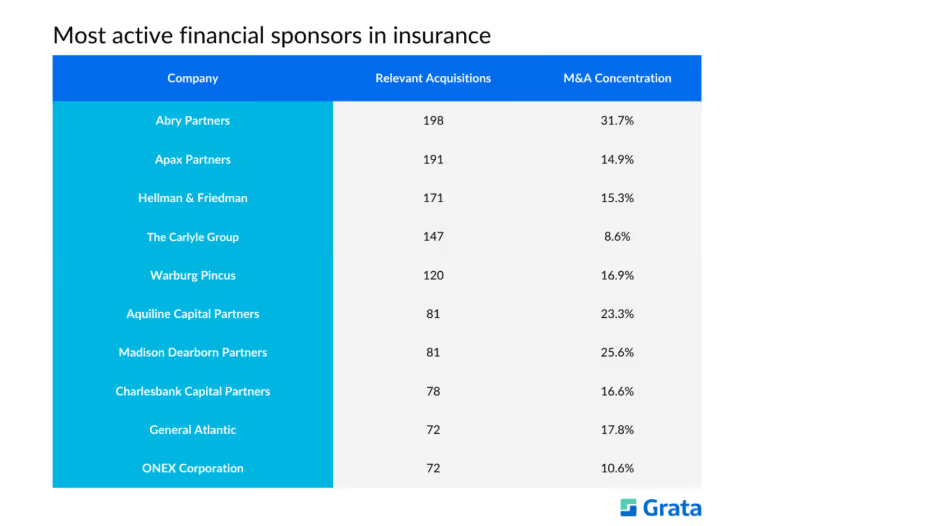

Most Active Financial Sponsors

Source: Grata

Abry Partners tops the list of most active financial sponsors in the insurance industry with 198 total relevant transactions. Many of the firm’s recent acquisitions targeted independent brokerages offering personal and commercial insurance products.

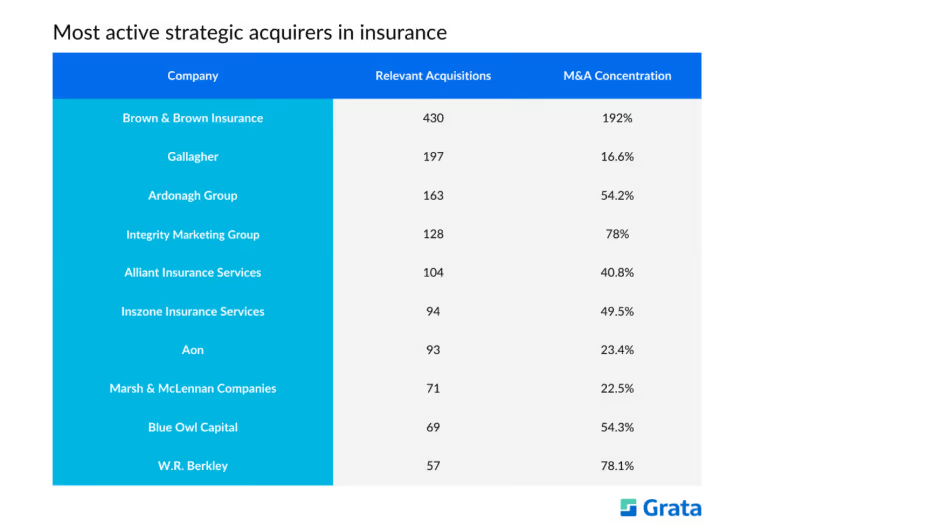

Most Active Strategic

Source: Grata

Brown & Brown Insurance is the most active strategic acquirer in the insurance industry, with 430 relevant deals. Its acquisitions cover a wide range of insurance solutions across the personal and commercial sectors.

Insurance Industry Overview

Market Distribution

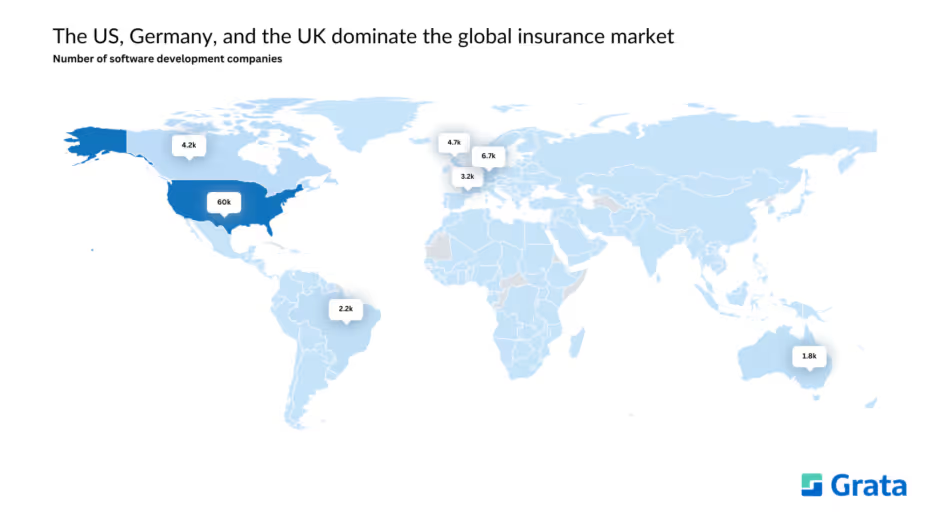

Geography

Source: Grata

The US, Germany, and the UK lead the global insurance market by number of companies. Other notable players include Canada, France, Brazil, and Australia.

Source: Grata

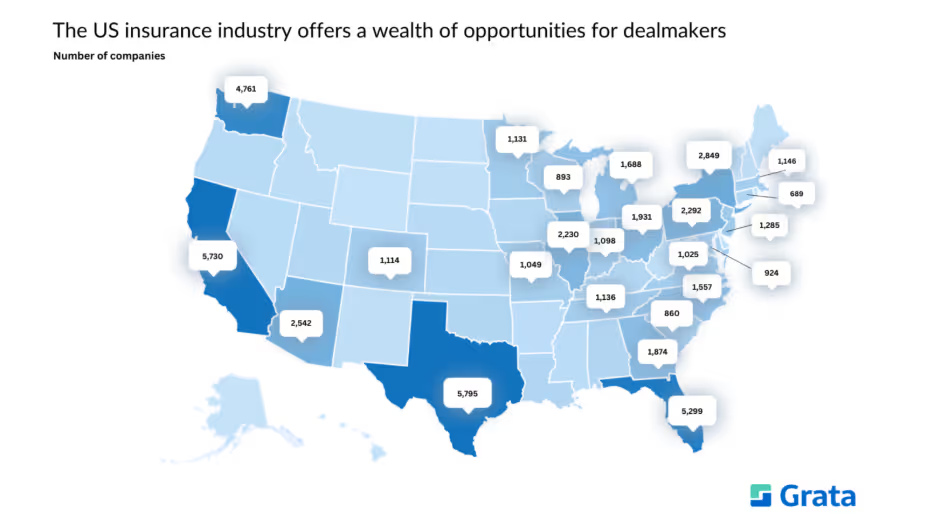

Private market dealmakers focused on the US have a plethora of opportunities to explore. Some key factors and regions to consider:

States with regulatory environments favorable to insurance companies include Arizona, Kentucky, Virginia, Nevada, and Indiana.

Wyoming, Wisconsin, and Alaska are among the most ideal states for homeowners insurance providers due to relatively low risk of natural disasters and high profitability.

Maine, Wisconsin, and Ohio are among the top markets for auto insurance due to low average rates and healthy market competition.

The commercial health insurance markets in Oregon, Wisconsin, and Pennsylvania are highly competitive.

Big-name insurers dominate around 85% of the insurance markets in Delaware, Iowa, and Utah.

Dealmakers should look to states that leverage “no-file” or “use-and-file" systems, which allow insurance companies to set their rates with little interference from the state. Illinois is one such example.

Additionally, states with lower litigation rates against insurers typically allow for stronger underwriting profitability.

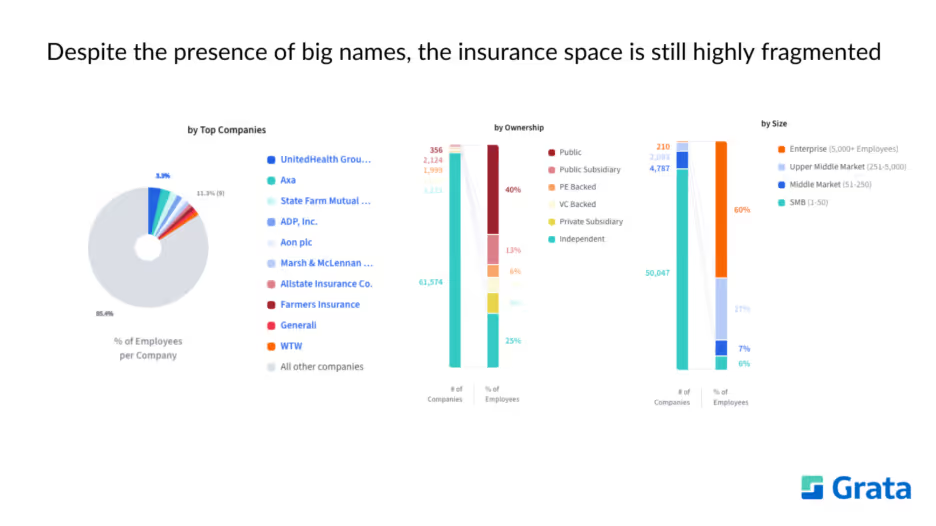

Ownership

Source: Grata

While the insurance industry is led by major players like UnitedHealthcare Group, the space is still highly fragmented. With over 65,000 privately owned companies currently in operation, dealmakers have a wealth of opportunities in the insurance industry.

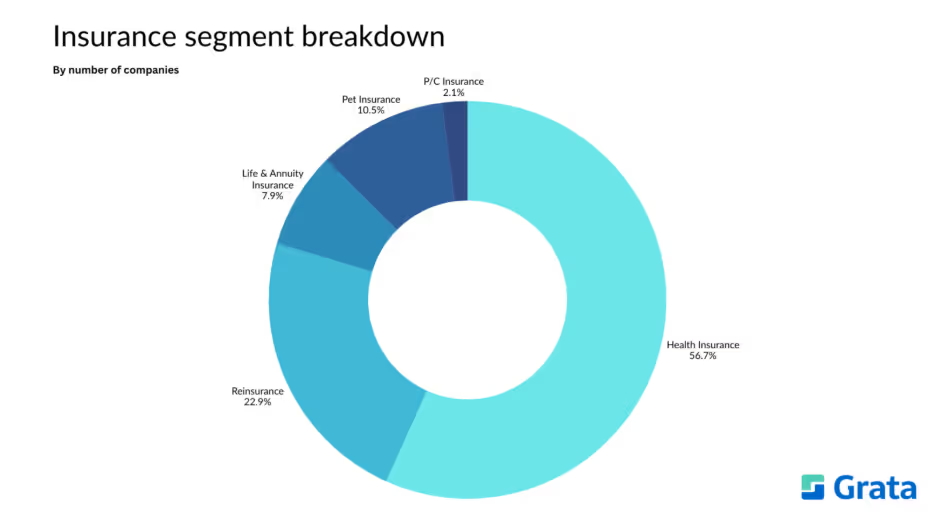

Segment Distribution

Source: Grata

This report focuses on the following segments of the insurance industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

The public insurance industry is full of high performers. Of the sectors analyzed in this report, pet insurance companies see the most average revenue and growth by a long shot. The average cost of a visit to the vet has surged by more than 60% in the last decade, pushing more consumers to enroll in insurance for their furry friends. Insurers are also increasingly offering more tailored plans that include wellness and alternative therapy services, as well as plans that cover a wider range of pet types.

Meanwhile, reinsurance companies tend to see the highest EBITDA margins. Rising premiums and limited capacity drive up profitability per unit of risk. Additionally, reinsurers have low customer acquisitions costs and fewer administrative expenses compared to other types of insurers. This is because they work with smaller groups of large, corporate clients instead of many individual customers.

Insurance Private Comparables

Source: Grata

In the private realm, life & annuity companies bring in the most revenue on average. These firms make their cash by collecting premiums for policies that may not pay out for decades — if they pay out at all. That cash, or “float,” is invested in assets that accrue interest, such as bonds, stocks, and real estate. Additionally, as millions of Baby Boomers exit the workforce, demand for annuity products that guarantee income is on the rise. Sales are at record highs, especially for fixed-indexed annuities.

For dealmakers looking to establish themselves as leaders in a smaller niche, P/C insurance could be the right fit. P/C insurance companies account for just 2.1% of the industry, and they have raised relatively little capital. However, they generate just under $223M in average annual revenue, and they are growing at a healthy rate of 9.6% — notably higher than the industry average.

Notable Acquisitions in the Insurance Industry

Source: Grata

WTW Acquires Newfront Insurance

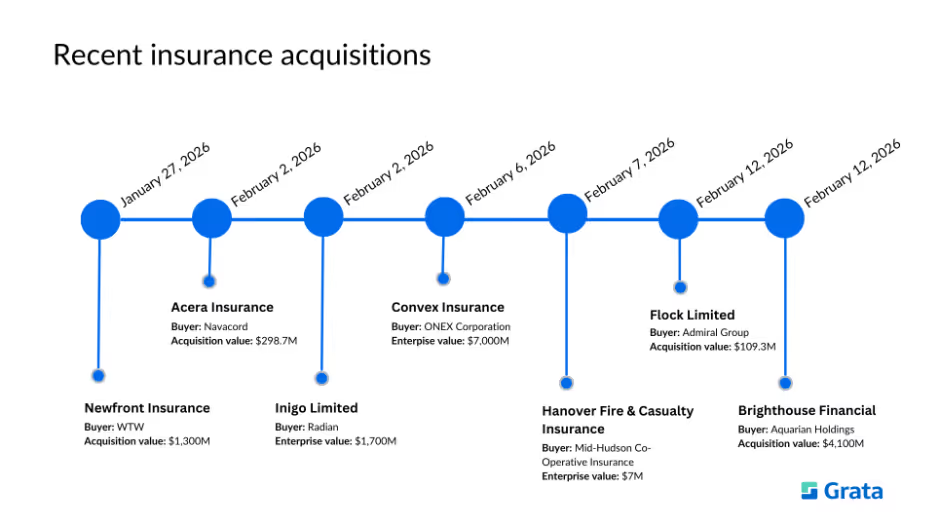

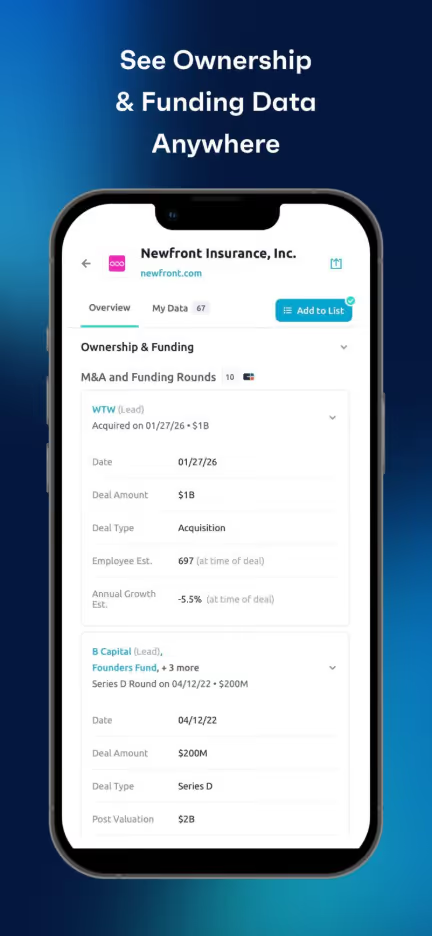

Last month, global advisory, broking, and solutions company WTW acquired Newfront Insurance for $1.3B. Newfront Insurance offers a suite of services including commercial property and casualty insurance, total rewards and benefits solutions, risk analytics, claims support, and proprietary technology platforms for streamlined policy management and data insights.

If you’re an investor interested in companies similar to Newfront Insurance, try these:

Learn more about this acquisition — or any of the others listed below — anytime, anywhere using the latest version of the Grata Go mobile app. Get all of the ownership and investment data you need right in the palm of your hand.

Navacord Buys Acera Insurance

Canada-based insurance brokerage network Navacord completed its acquisition of Acera Insurance in February. Acera is based in Calgary. It provides insurance brokerage and policy placement for personal and commercial customers. Its specific offerings include vehicle, home, travel, tenant, equine and specialty coverage, as well as business insurance and group benefits.

If you’re an investor interested in companies similar to Acera Insurance, try these:

Pennsylvania-based Radian, which provides private mortgage insurance and risk management services, bought Inigo Limited in February. Inigo provides commercial insurance and reinsurance. It was valued at $1.7B at the time of the deal.

If you’re an investor interested in companies similar to Inigo Limited, try these:

Private equity firm ONEX Corporation purchases Convex Insurance for $7B in February. Convex Insurance provides international specialty insurance and reinsurance and digital risk management solutions to commercial clients and intermediaries.

If you’re an investor interested in companies similar to Convex Insurance, try these:

Mid-Hudson Co-Operative Insurance Buys Hanover Fire and Casualty

Later in February, Mid-Hudson Co-Operative Insurance completed its $7.5M acquisition of Hanover Fire and Casualty Insurance. Hanover Fire and Casualty is based in Pennsylvania. It offers property and casualty insurance for residential customers, as well as equipment breakdown and service line protection.

If you’re an investor interested in companies similar to Hanover Fire and Casualty Insurance, try these:

UK-based insurance company Admiral Group purchased Flock Limited, a commercial motor fleet insurance provider, for $109.3M earlier this month. Flock Limited serves a range of fleet operators, including couriers, rentals, taxis/PCOs, trades/own-goods, telecoms, removals, and leasing.

If you’re an investor interested in companies similar to Flock Limited, try these:

Aquarian Holdings completed its $4.1B acquisition of Brighthouse Financial earlier this month. Brighthouse is a North Carolina-based insurance company that specializes in life and annuity products.

If you’re an investor interested in companies similar to Brighthouse Financial, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the insurance industry:

An insurance agency with $7.5M in revenue and an expected valuation of $1.1M

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

Insurance Industry Conferences

Grata makes it easy for dealmakers to find conferences, events, and trade shows in their industries. See attendee lists so you can set up meetings beforehand and make the most of your travel time. Check out which companies attended past events to find more potential targets.

Here are a few of the events related to the insurance industry that dealmakers can find and track in Grata:

Get the Most Out of the Playbook

If you’re an investor interested in making moves in the insurance space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

From market trends to career advice, Grata’s content fuels smarter decisions.

Sourcing

Why Proprietary Deal Flow Is Getting Harder — and How Leading Teams Are Adapting

Proprietary deal flow is getting harder as generalist AI closes the access gap. See how verified private-market data and Seller Intent help dealmakers source before the competition does.

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

Hidden Gems: Actionable, Undiscovered Opportunities in the HVAC Industry

Discover 79 undiscovered HVAC companies with high Seller Intent scores. See ownership, geographic, and sector breakdowns from Grata's proprietary private market data.

.png)

.webp)