When it comes to total addressable market, no industry compares to death services.

Thinking about the end of life may be uncomfortable, but businesses in the death services space are working to provide as much agency, personalization, and comfort as possible.

The US death care market, in particular, is expanding and evolving as the aging population grows and demand for personalized and sustainable funerary services increases.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the death services market, including:

How shifting consumer preferences are affecting growth across segments

Industry fragmentation

Where investors have opportunities to improve the space

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Industry Overview

Market Distribution

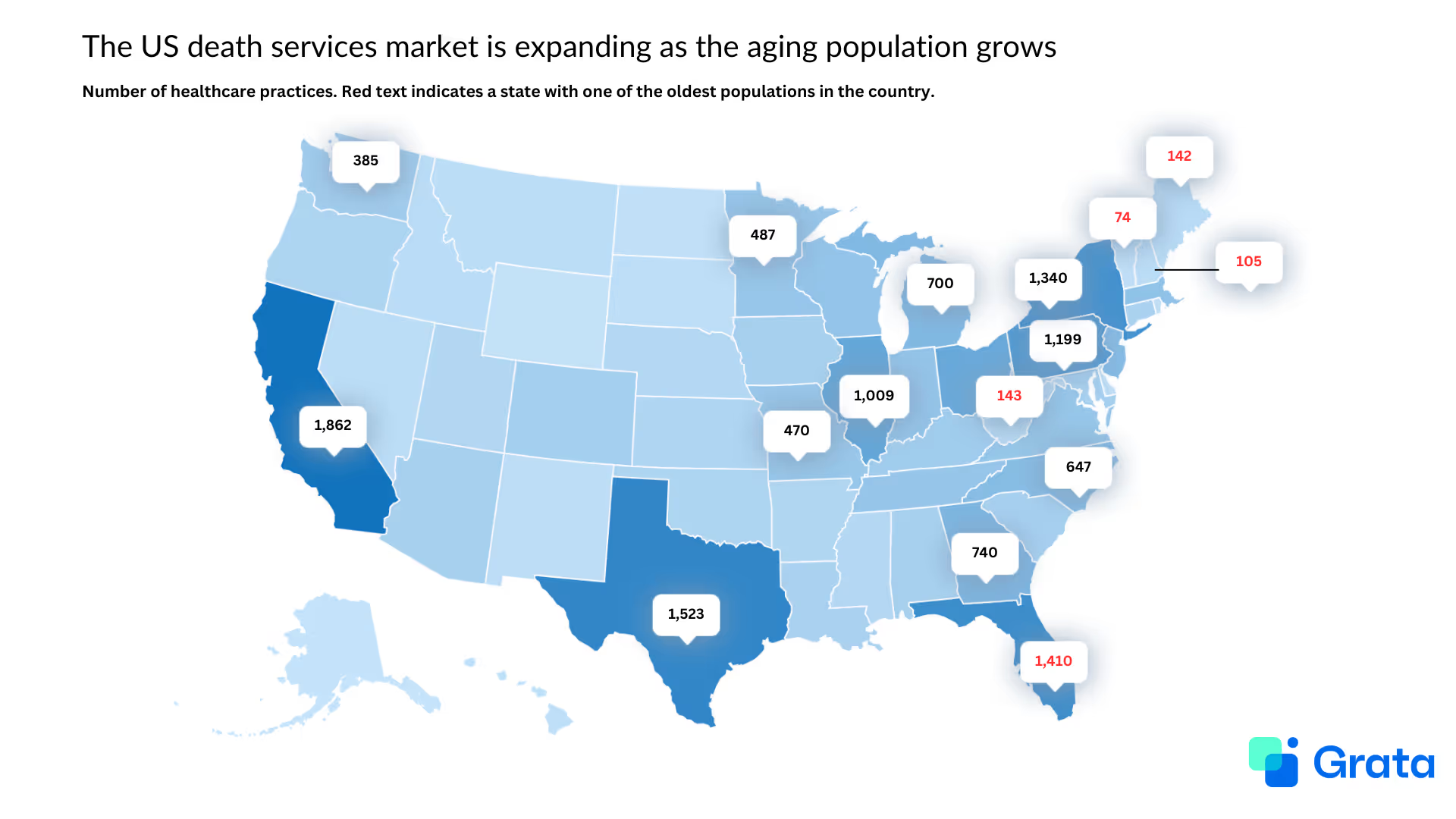

Geography

Source: Grata

One of the main factors contributing to the growth of the death services industry in the US is the expanding aging population. Currently, there are around 65M people aged 65 and older living in the country, according to Pew Research Center. That number is projected to rise to 84M in the next 30 years.

Notably, some states have a larger aging population than others. Maine, New Hampshire, Vermont, West Virginia, and Florida are home to the oldest populations in the country.

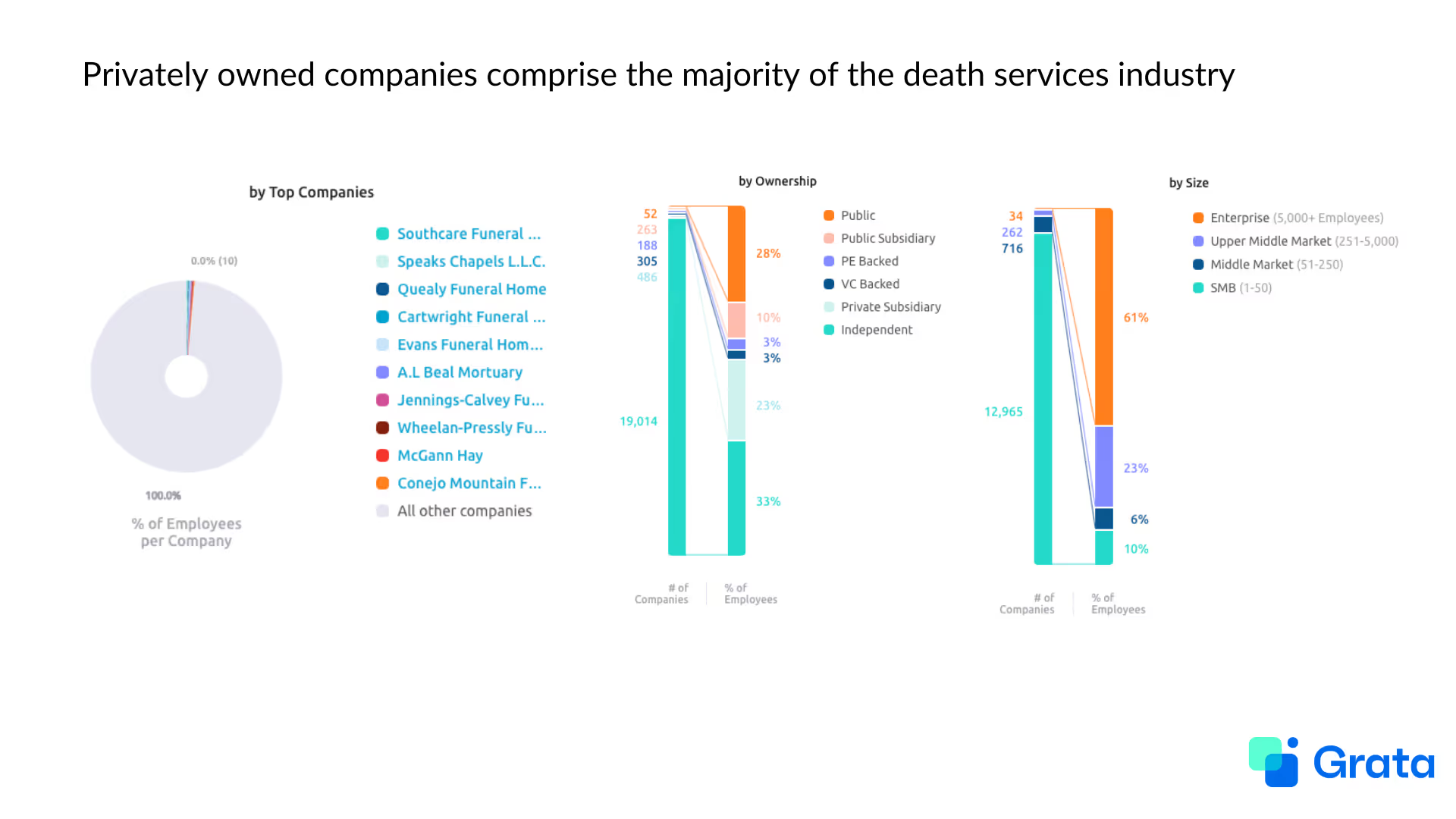

Ownership

Source: Grata

While public companies and their subsidiaries have a notable presence in the death services industry, the vast majority of companies in the space are privately owned. Currently, there are over 19,000 death services companies that could be strong acquisition opportunities.

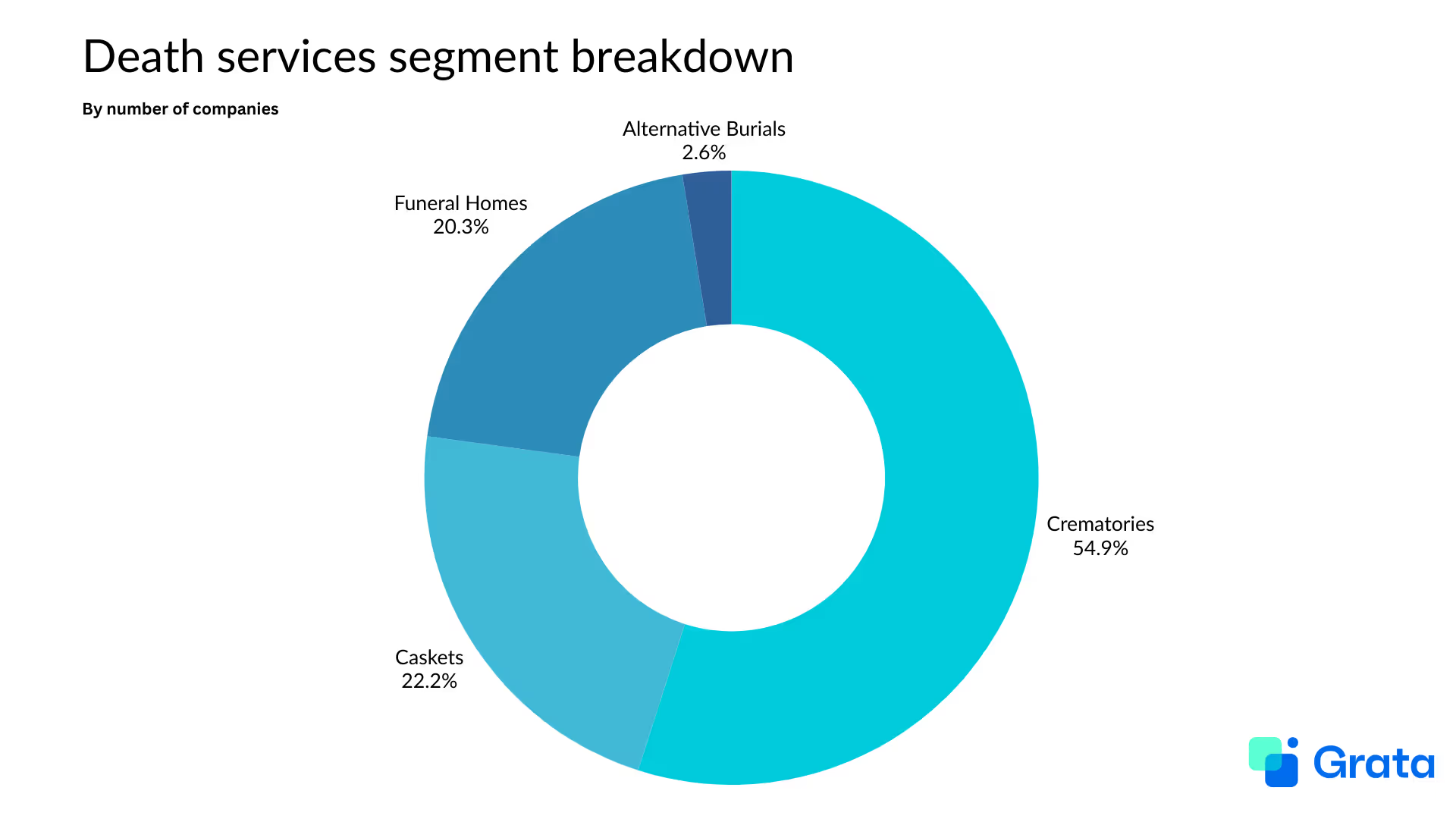

Segment Distribution

Source: Grata

This report focuses on the following segments of the death services industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

Crematories: Companies in this segment offer traditional cremation services.

Caskets: The companies in this market manufacture and sell coffins and caskets for funerary services.

Funeral Homes: These companies offer funeral, visitation, and burial services to memorialize the deceased.

Alternative Burials: Companies in this sector provide less traditional funeral services and methods of handling human remains, including green burials, human composting, cremation jewelry, at-sea burials, cryogenic freezing, water cremation, and more.

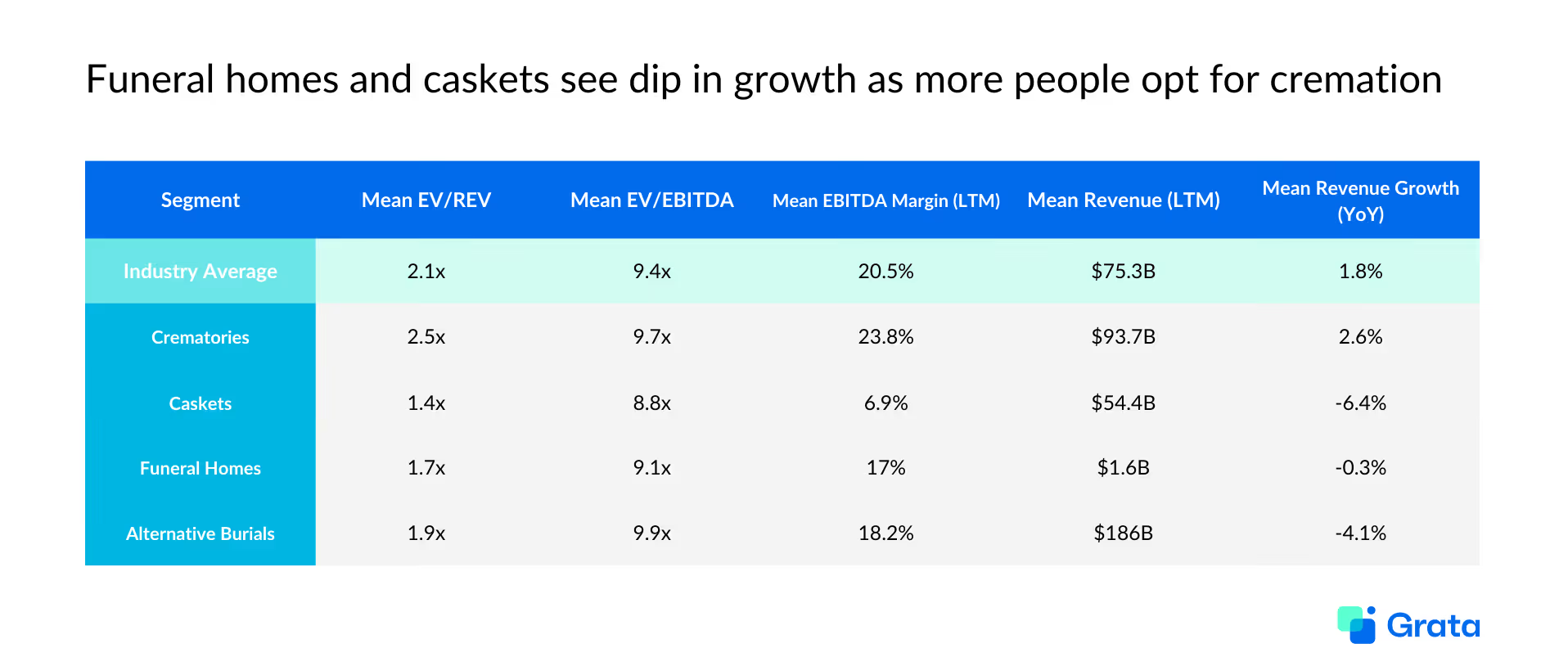

Public Comparables

Source: Grata

The funeral industry is undergoing a shift as consumers increasingly choose cremation over traditional burial services. Part of this has to do with cost. As of 2023, the median cost of a funeral with cremation was $6,280 while a funeral with a viewing and burial totaled around $8,300. Younger generations are also driving interest in more environmentally friendly options for funeral services, further contributing to the rise in cremation. As a result, the funeral homes and caskets sectors are experiencing a dip in average growth.

The growing desire for less expensive, eco-friendly, and more personalized services is also contributing to the emergence of alternative burials. These include human composting, tree burials, alkaline hydrolysis (aka water cremation), at-sea burial, and more. Alternative burials tend to be less expensive than traditional burials because they do not require embalming, caskets, vaults, etc.

Currently, the alternative burials segment is still quite small, with just under 2,000 total companies operating in the space. For this reason, there are only two companies that are viable public comps, accounting for the space’s high average revenue and negative growth. However, the segment will likely gain momentum as consumer preferences continue to shift away from traditional funeral services.

Private Comparables

Source: Grata

For now, traditional funeral homes look to be the steadiest bet for dealmakers in the death services space. These facilities see the highest average revenue and a growth rate of 11.3% per year.

Crematories earn under $1M in average annual revenue. However, the segment sees the highest growth rate on average due to consumer preferences shifting away from traditional burials.

Alternative burials are the only segment analyzed in this report that has raised any significant amount of funding. This indicates the growing interest, particularly from younger generations.

Acquisitions

Top Roll-Ups

Source: Grata

The death services space has seen a significant amount of roll-up activity over the past several years. Carriage Services and Funeral Partners Limited lead with 59 investments in the space each. Independent funeral homes and directos account for the vast majority of their acquisitions.

Notable Acquisitions

Source: Grata

Funeral Homes: Funeral Partners Limited Acquires Joseph O’Connell Funeral Services

In May, Funeral Partners Limited acquired UK-based Joseph O’Connell Funeral Services for an undisclosed amount. Joseph O’Connell Funeral Services is a family-operated funeral home established in 2011.

If you’re an investor interested in companies similar to Joseph O’Connell Funeral Services, try these:

Funeral Partners Limited Acquires Nicholas O’Hara Funeral Directors

In June, Funeral Partners Limited purchased another UK-based, family-owned funeral home: Nicholas O’Hara Funeral Directors. The business was established in 1974. Financial terms of the deal were not disclosed. O’Hara’s children will reportedly continue to run the business post-acquisition.

If you’re an investor interested in companies similar to Nicholas O’Hara Funeral Directors, try these:

Scotmid Co-operative acquired Fosters Funeral Directors in September for an undisclosed amount. Fosters reportedly operates 24 funeral homes, bringing Scotmid’s total to 40. The facilities are primarily located in central Scotland.

If you’re an investor interested in companies similar to Fosters Funeral Directors, try these:

Caskets: Victoriaville & Co. Acquires Haven Line Industries

Victoriaville & Co. completed its acquisition of Pennsylvania-based Haven Line Industries in July. The deal reportedly supports Victoriaville’s plan to expand its business geographically and strengthen its service offerings

If you’re an investor interested in companies similar to Haven Line Industries, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. If you’re interested in sourcing live deals in the death services space, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

Get the Most Out of the Playbook

If you’re an investor interested in the death services space, Grata can help you put the insights in this report into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

From market trends to career advice, Grata’s content fuels smarter decisions.

Sourcing

Why Proprietary Deal Flow Is Getting Harder — and How Leading Teams Are Adapting

Proprietary deal flow is getting harder as generalist AI closes the access gap. See how verified private-market data and Seller Intent help dealmakers source before the competition does.

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

Hidden Gems: Actionable, Undiscovered Opportunities in the HVAC Industry

Discover 79 undiscovered HVAC companies with high Seller Intent scores. See ownership, geographic, and sector breakdowns from Grata's proprietary private market data.

.webp)

.avif)

.avif)

.avif)

.png)

.webp)