AI & Automation

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

.webp)

.jpg)

As headlines like It’s Doom Time in Tech and Target Stock Down 30% In A Week, it’s important to remember that private equity doesn’t behave the same as public markets.

I don’t claim to have a crystal ball, but I do see stark differences between now and past recessions, specifically 2007, that lead me to believe that lower middle market deals will bounce back quickly from this dealmaking downturn.

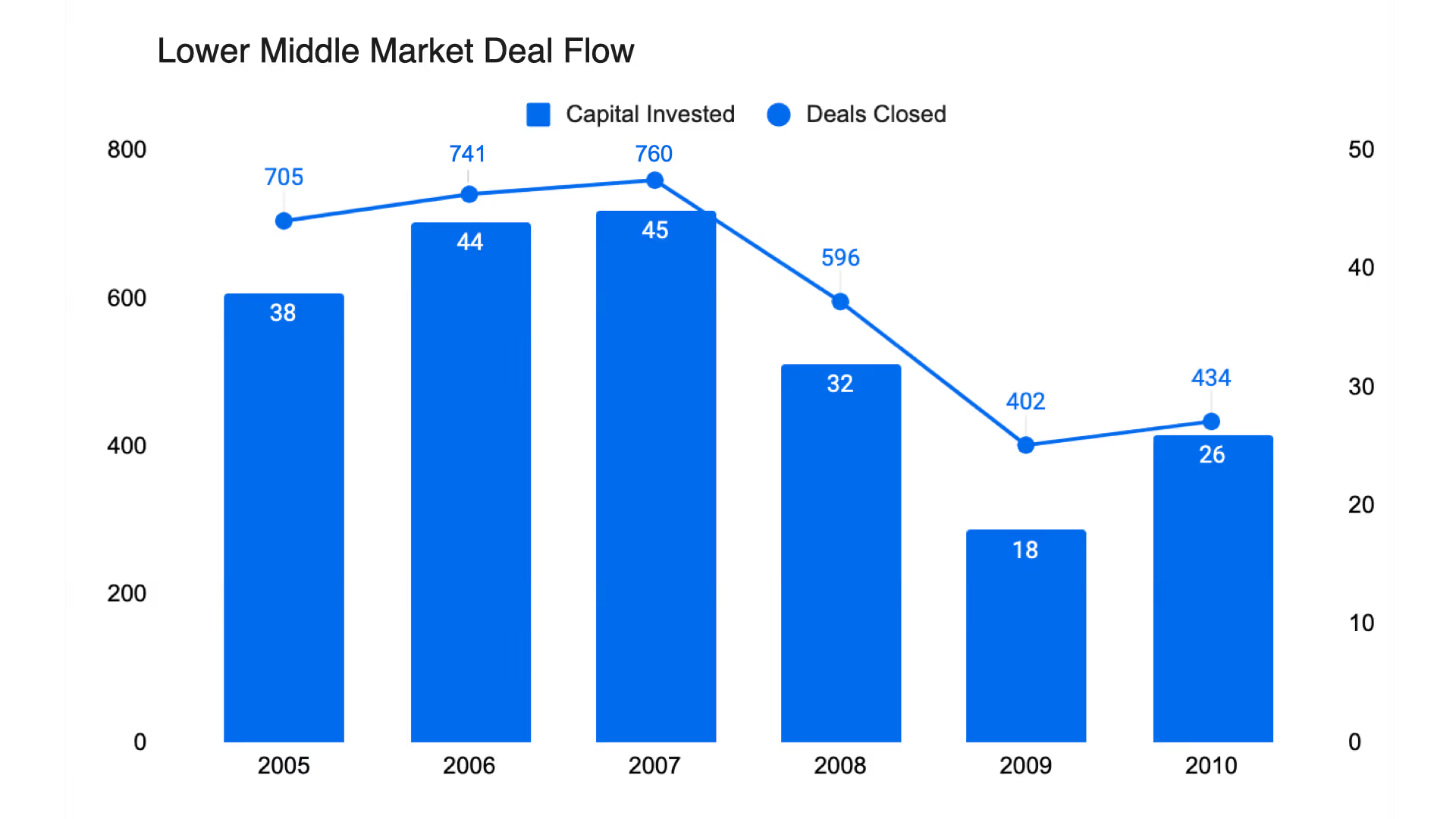

In 2009, we saw a 47% decrease in lower middle-market deals from 2007 highs.

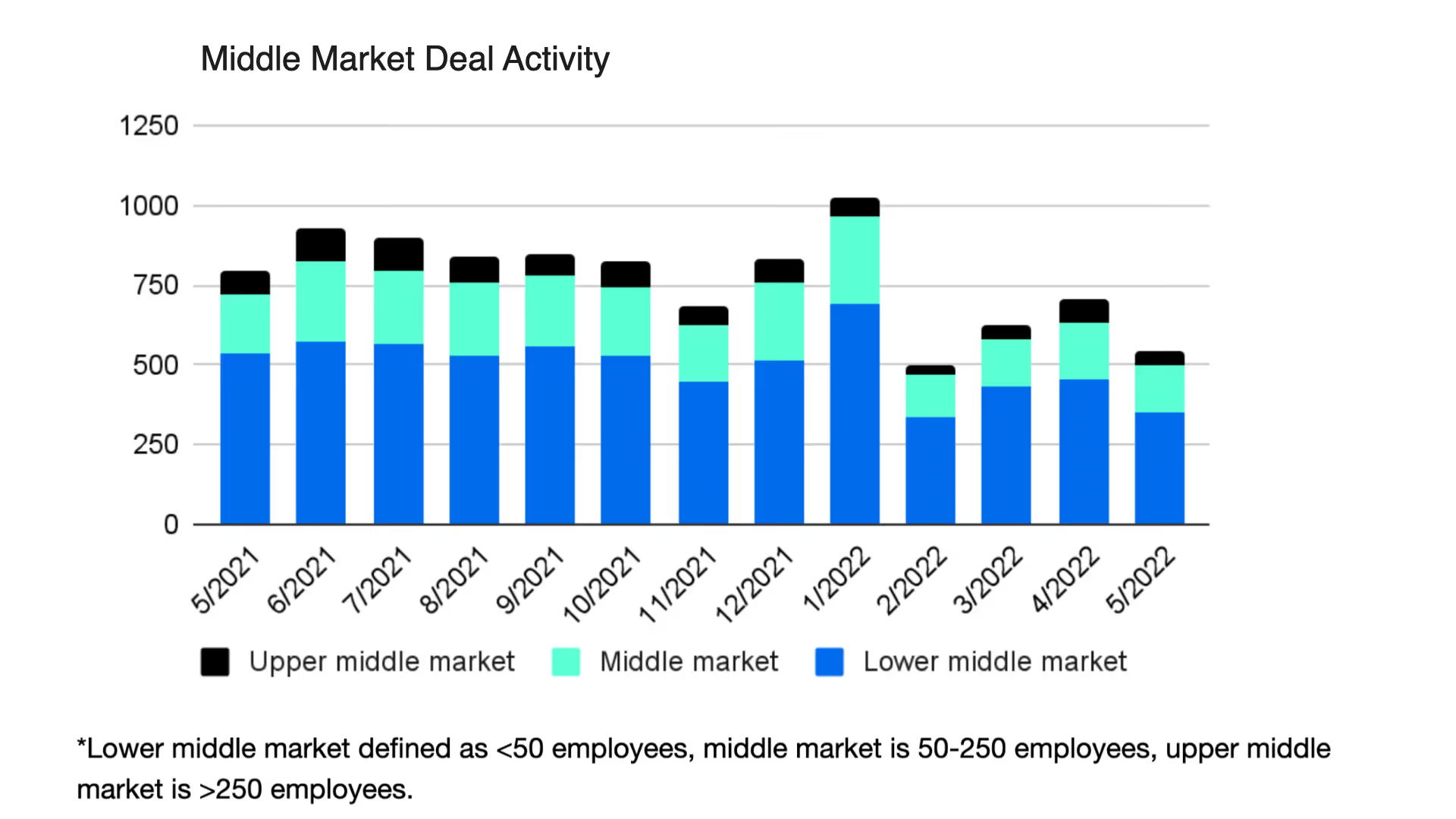

May 2021 to May 2022 saw a 31% decrease in the number of mid market deals, according to Grata. This trend has held consistent for the last 3 months.

It’s pretty clear dealmaking will slow down in 2022.

Part of this is due to the macroeconomic climate, but it also has to do with the unreal amount of deals (and valuations) in 2021. To quote Vito Sperduto, RBC Capital Markets, “Even if there’s a 20% drop-off in volume this year (2022), this will still be the second strongest year for PE’s on record.”

The simple factors of supply and demand are playing in certain private investors’ favor this time around.

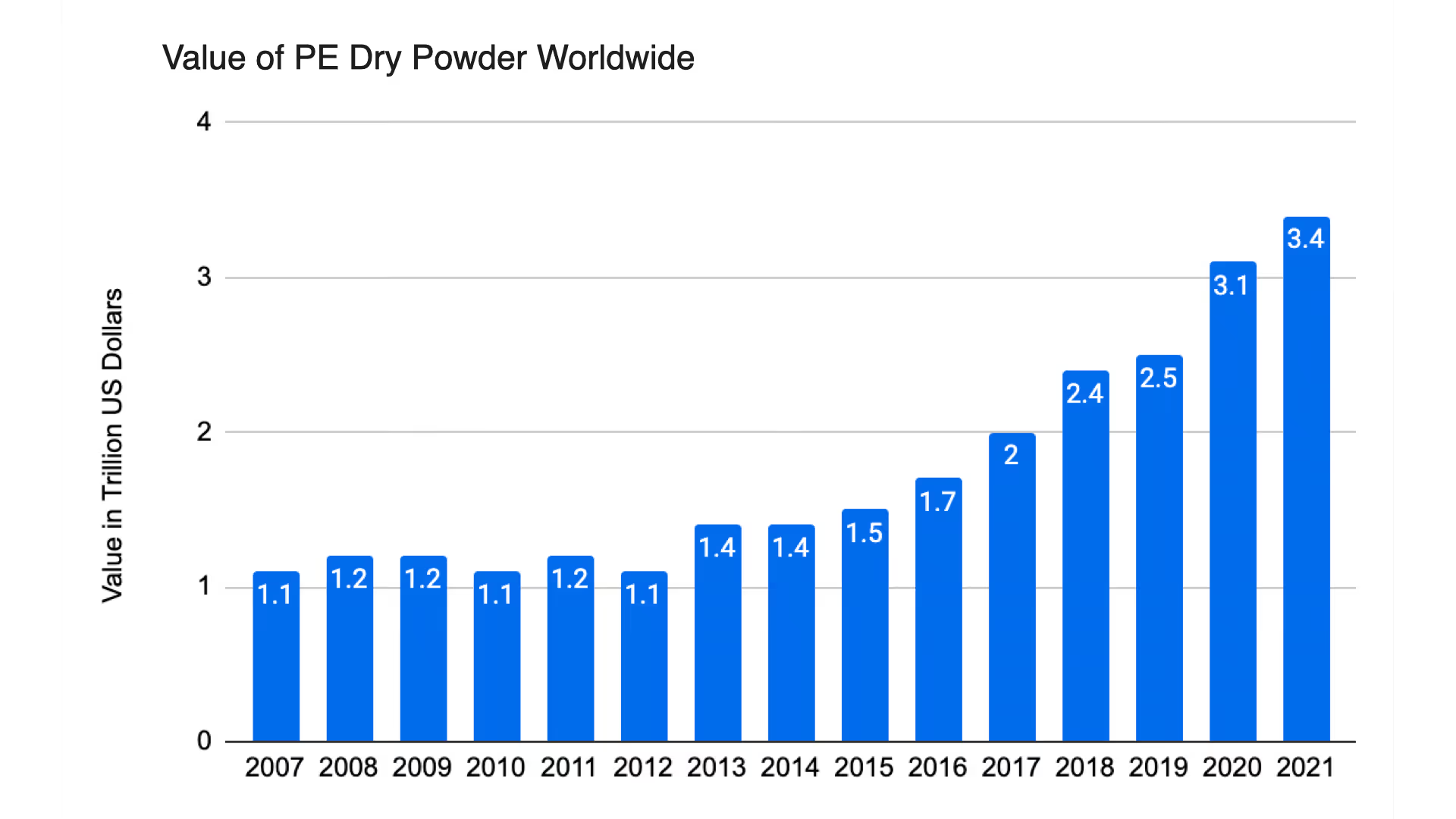

1. There’s more dry powder. General private equity demand starts with the amount of committed uninvested capital (also known as “dry powder”) in the market, and there’s an extensive amount of dry powder in private equity right now.

Dry powder has been on the rise for at least ten years. Investors in 2007 were looking at 1.1 trillion of dry powder. Today, there’s 3.4 trillion of dry powder. That’s right - there’s 3x more capital (a whopping 2.3 trillion more) waiting to be poured into private markets.

PE firms do not profit by holding cash. That 3.4 trillion needs to be invested, and a lot of that will be in 2022.

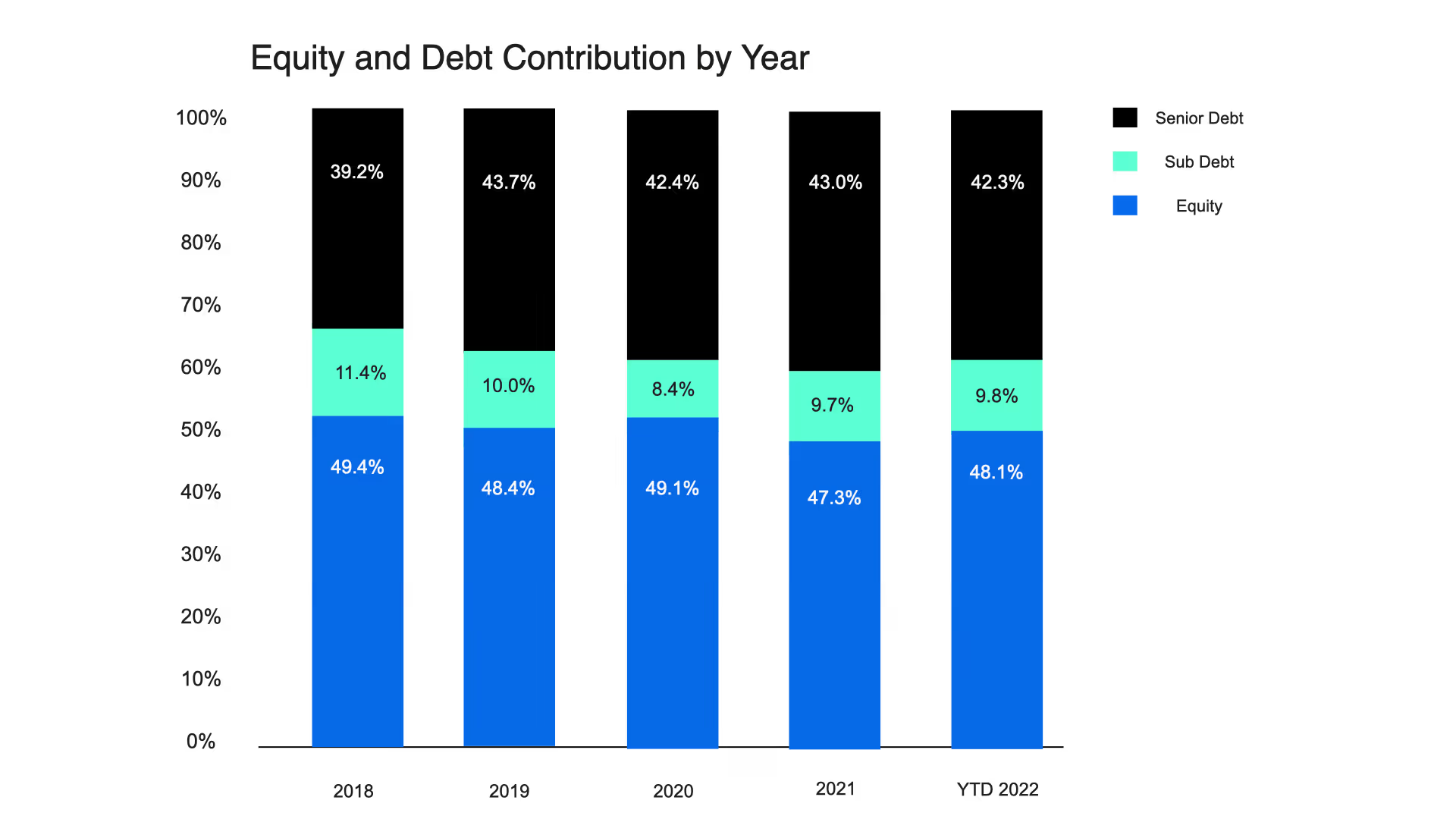

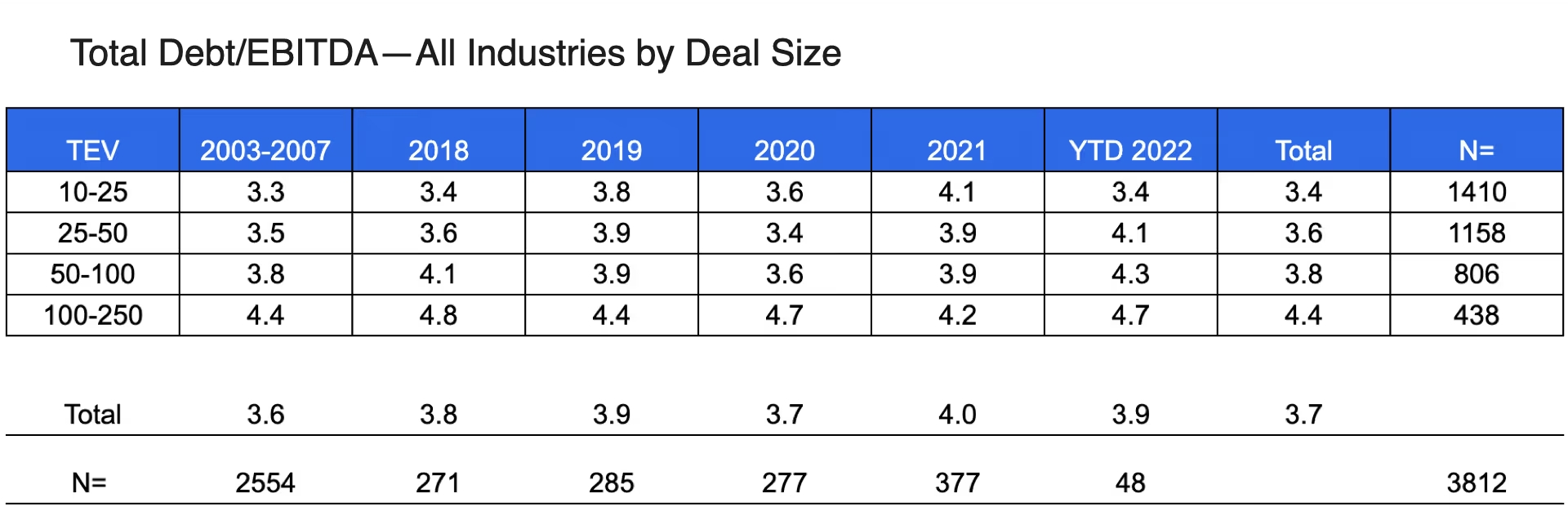

2. Higher interest rates will slow capital deployment. It’s obvious that higher interest rates decrease LBO returns. When returns are lower, investors move slower. However, according to GF Data, equity contributions as a percentage of deal value haven’t changed since they reset in 2011, averaging 47-50% of total enterprise value (TEV) and up from sub 43% in 2007 and before. That could mean reduced demand, but a lower impact than the financial crisis.

3. Deals are getting smaller and less macroeconomic sensitive. “Rollups” and “tuck-ins” (collectively, “add-ons”) are the new strategy of choice for PE and corp dev, which lead to smaller deals. While deal leverage has risen over the last decade, smaller deals (<$100M) have less debt according to GF Data. Deals under $50M TEV average debt 3.4-3.6x EBITDA compared to deals >$50M TEV averaging 3.8-4.4x EBITDA. Add-on deals are less financially engineered and therefore less sensitive to interest rate hikes.

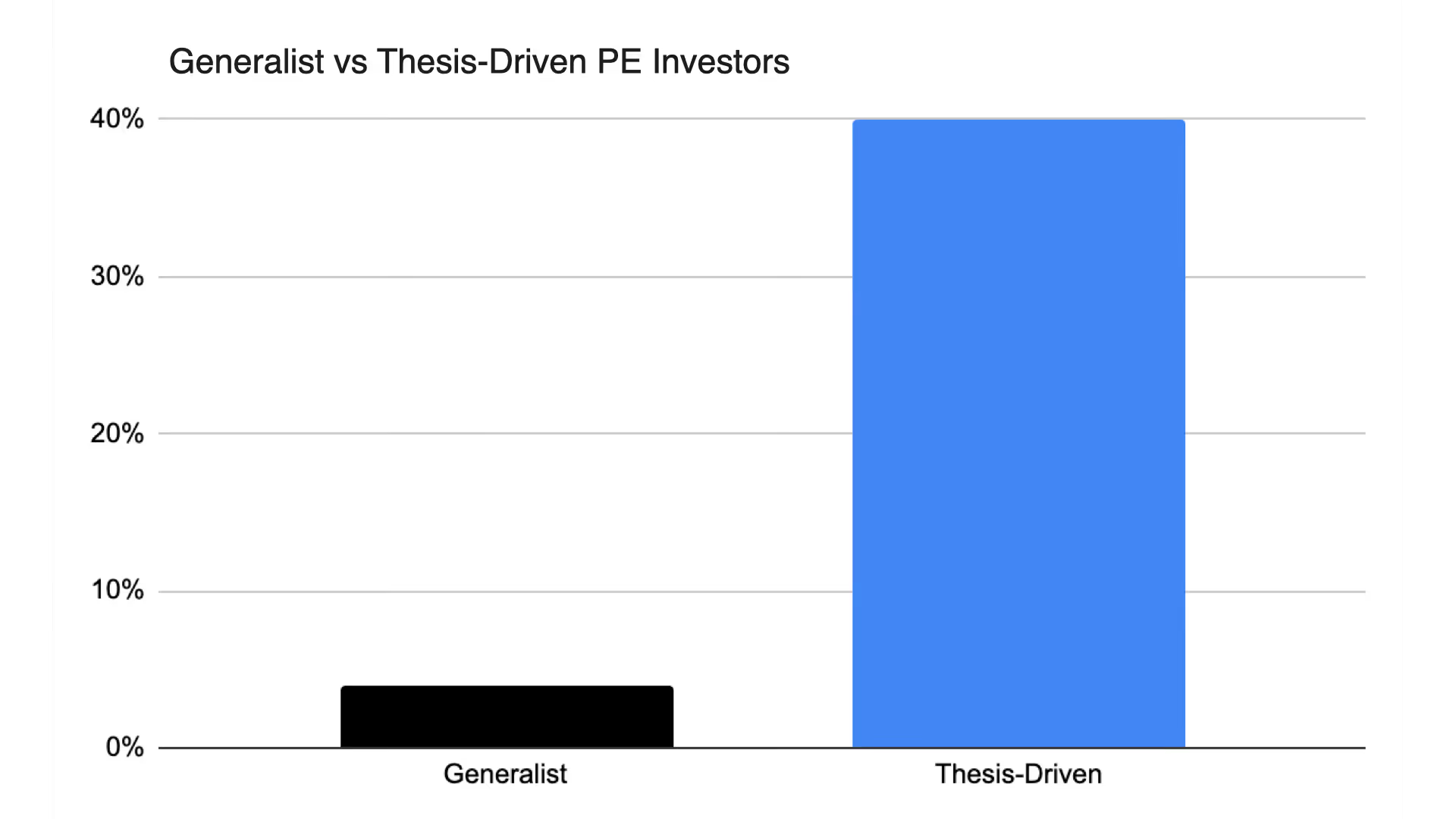

4. Thesis-driven investing is on the rise. Firms that are more thematic are less phased by short term volatility. They’re not swing or momentum investors - they take a long-term approach to value creation. Because of the large amount of capital in the markets, more firms have adopted thesis-driven investing to build expertise and differentiate themselves. Our research shows that true generalist investors are rare these days.

According to Grata, less than 5% of PE firms are generalists. Compare that to 40% of PE firms that have true thesis-driven investment mandates.

While upper middle market deals may slow down, signs are pointing at a high demand for lower middle market deals.

Decreasing valuations are less enticing for business owners. Valuations in 2021 ballooned so much that the number of business owners willing to sell increased. Equity was cheap. It was an enticing market for owners to sell. Lower valuations make equity more expensive to “trade” for cash. If business owners don’t have a need for liquidity, it makes sense for them to hold on to their business.

However, boomers are reaching retirement and seeking liquidity. The single largest factor to consider is that baby boomers, born between 1946 and 1965, are hitting 60-75. That's the prime retirement age and pretty close to the 79 year average life expectancy in the US. According to the Federal Reserve Flow of Funds Report and research by Tiburon Strategic Advisors, boomers are expected to liquidate over $14 trillion in small business valuations. While not every deal will go to private equity, that’s still over 4x the amount of dry powder in need of liquidity.

Economic downturn increases the need for financing. Small businesses get hit hardest by financial turmoil. We don’t have to look as far back as 2007 to see this; it’s estimated that 200,000 small businesses went closed because of COVID. When an economic downturn hits, debt financing is harder to secure and equity becomes an easier option.

Private equity is creating their own supply (“proprietary dealflow”). According to Grata, there are <150,000 investor backed companies but another 8M+ bootstrapped companies in the US that have not had access to outside capital. While this seems like a lot of opportunity, Bain & Co and Sutton Place Strategies cited that the average private equity firm that relies on intermediaries sees only 18% of deals; thus, the importance of proprietary deal sourcing to keep dealflow high.

In the last few years, more private equity firms have formed business development teams and proprietary deals sourcing has become a core part of the industry’s strategy. In fact, looking at deals in the last year in Grata, the share of lower middle market deals has held steady through 2022 thanks to proprietary sourcing. We only expect this to go up in the next couple of years.

There are more middle market investors creating more deals. Competition is also growing. Not only have the number of private equity investors increased, but there are more crossover investors like family offices, hedge funds, asset managers and more - totaling to over 25 thousand private market firms. More participants doing more proprietary sourcing means deals will get done, even if the average deals per firm goes down.

The good news? Companies that fall under the US middle market banner account for 99% of all businesses and 50% of GDP, so even 25,000 firms can only make a drop in this ocean.

1. Tech will take a hit. Not an astonishing prediction after the headlines we’ve seen– but it’s important to note because this hit will cause shell shock in other industries.

2. The market will pause for a quarter, maybe two at most. It’s a safe bet that we’ll see the market go into shell shock for a bit, if we’re not already there.

3. The middle market bounce back will be quick. As public markets and VC investing become less attractive, the middle market becomes more attractive. There’s security and consistency in the private markets returns, not found as easily in startups or public markets. Private market investors are growing their BD (“proprietary sourcing”) efforts to find the middle market companies seeking succession, less affected by valuations, and in need of financing— but there’s a catch. Middle market investors will also need to differentiate themselves from the 25,000 other investors going after the same targets.

My prediction: proactive, thesis-driven middle market dealmakers will weather the 2022 downturn.

Nevin Raj is the chief operating officer and co-founder of Grata, a private company intelligence engine for middle-market dealmakers. Grata helps dealmakers unleash the true potential of the middle market with smarter search, relevant intelligence, and automated technology. With access to the right data at the right time, firms that leverage Grata uncover new investment opportunities, fill their pipeline with promising companies, and unlock the middle market.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)