Data

What Is a Data Room? A Private Market Dealmaker’s Guide

Understand why private market deal teams need data rooms, the difference between a data room and a deal sourcing platform, and more.

.webp)

When it comes to the health and wellbeing of their pets, most owners are willing to spare no expense.

Last year, the pet care industry saw over $150B in sales of supplies, vet visits, treats, and more in the US alone. And it shows no signs of heeling. The global pet care market is projected to reach over $500B by 2030.

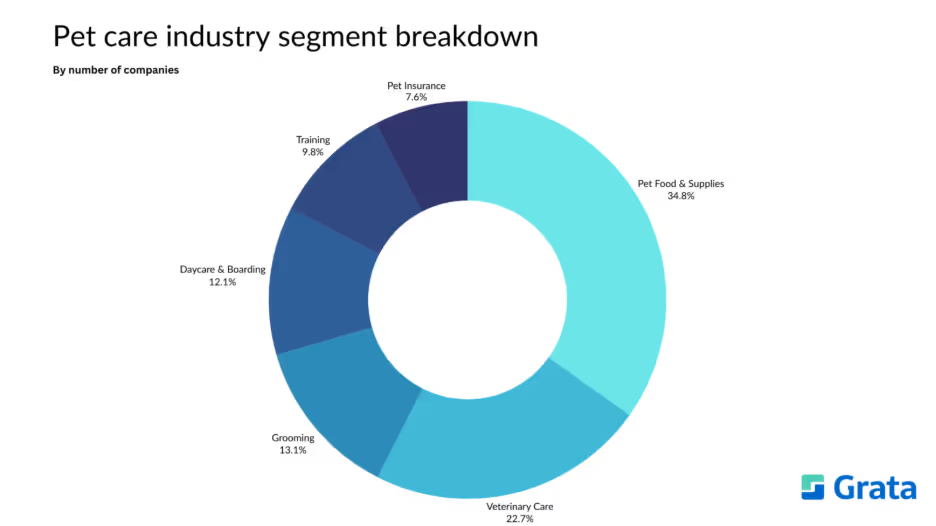

For dealmakers looking to fetch high returns, the pet care industry holds a wealth of opportunities across the veterinary care, pet insurance, daycare & boarding, food & supplies, grooming, and training segments.

In this PE Playbook, the Grata team has put together the latest need-to-know trends for investors considering making moves in the pet care market, including:

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

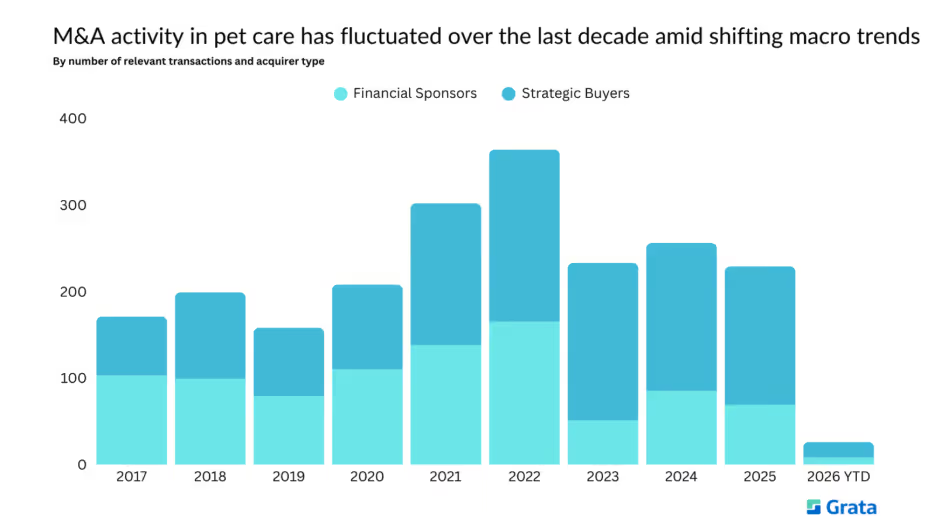

Source: Grata

Activity from financial sponsors and strategic buyers has ebbed and flowed over the course of the last 10 years. Deals peaked in 2022 as the pandemic-induced pet adoption boom reached a fever pitch. M&A in the pet care space has, for the most part, normalized to pre-pandemic levels since then.

Other contributing factors include:

Still, M&A activity in pet care is expected to rebound in 2026 due to:

Source: Grata

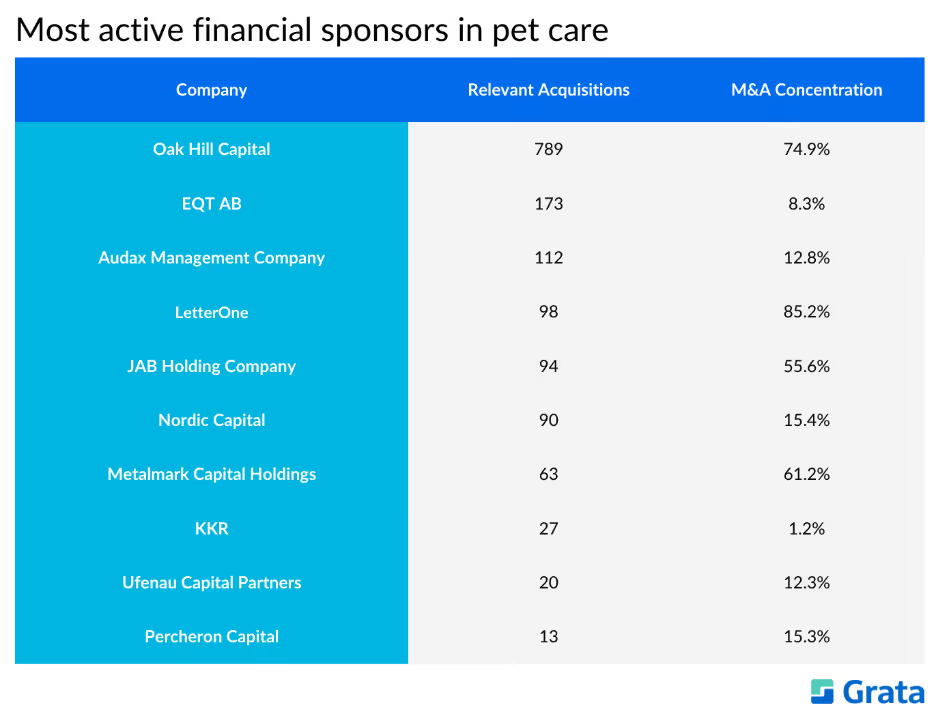

Oak Hill Capital tops the list of the most active financial sponsors in pet care with 789 relevant transactions. Its acquisitions primarily focus on veterinary care facilities.

Source: Grata

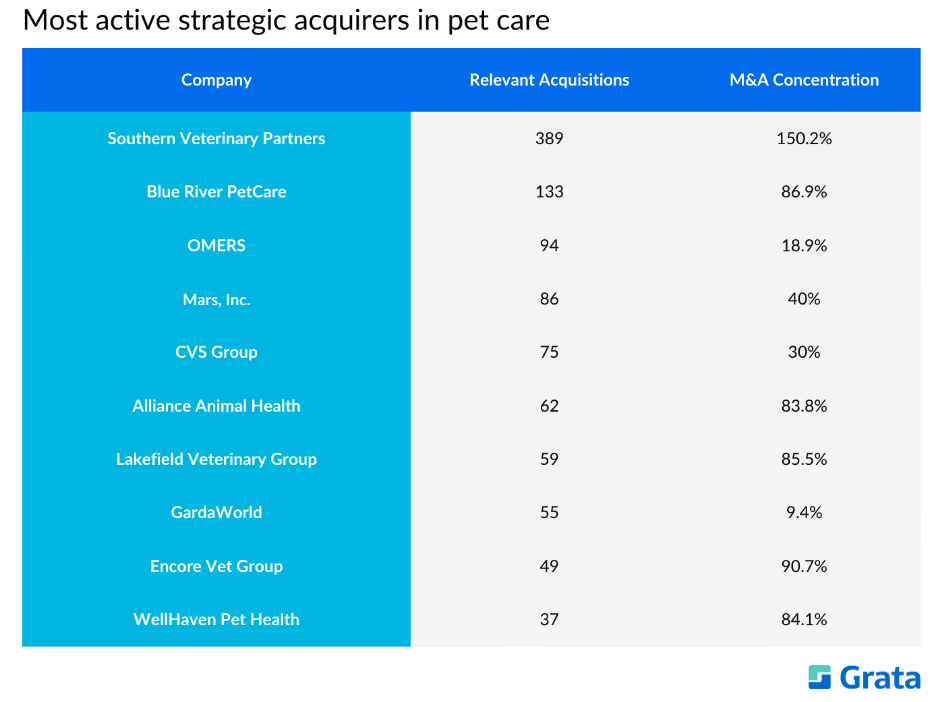

Southern Veterinary Partners is the most active strategic acquirer in the pet care industry, with 389 transactions. Most of its acquisitions have been in the veterinary care services sector.

Source: Grata

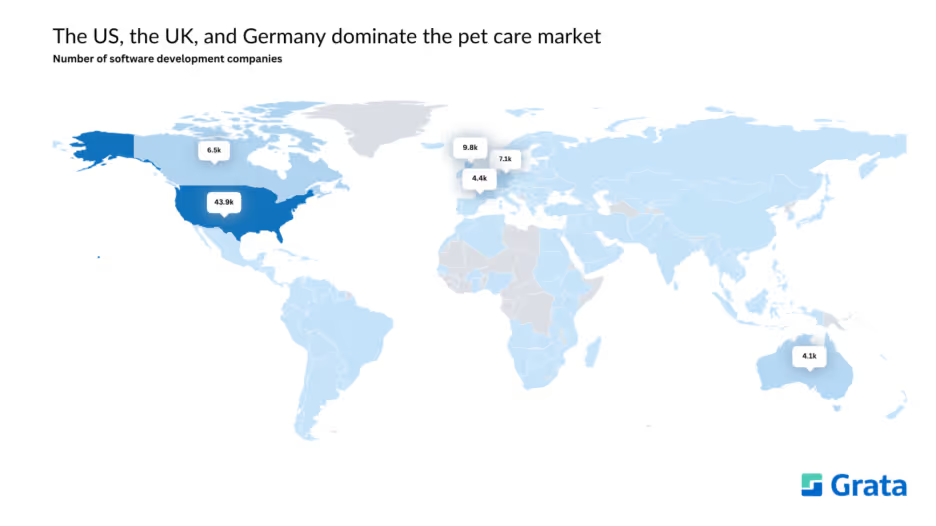

The US leads the global pet care market by number of companies, followed by the UK and Germany. Other major players in the space include Canada, France, and Australia.

Source: Grata

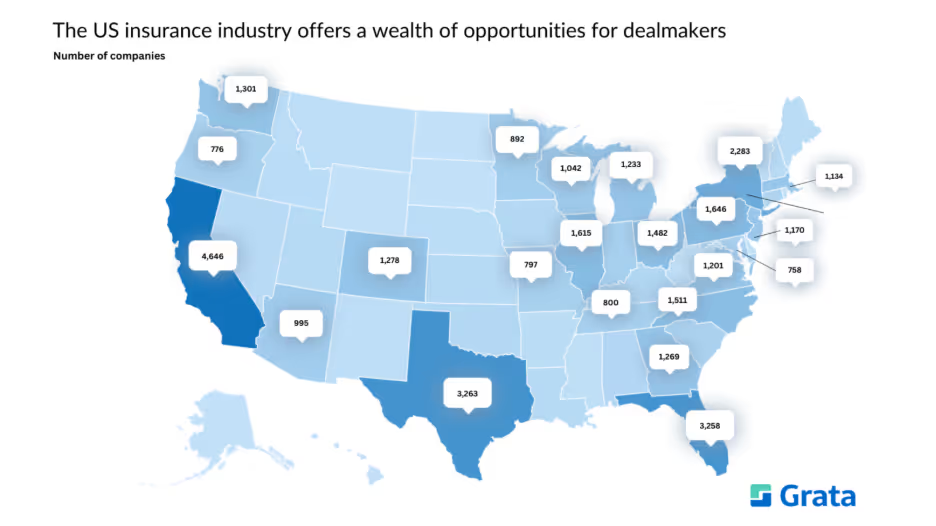

Dealmakers looking to make moves in the US pet care industry should prioritize areas with high costs of living and higher average income levels. People who live in these locations tend to have more disposable income to dedicate to their furry friends.

Unsurprisingly, California, the richest and most populous state in the country, is home to the most pet care companies in the US. Californians spend the most money on their pets by far, at an average cost of $3,143 per year. Top spending categories include high-end pet food, luxury pet products, and veterinary care.

Florida, Texas, and New York — also among the wealthiest and most populous states — are the second, third, and fourth largest pet care markets in the US, respectively. Outdoor pet products comprise one of the main spending areas for pet owners in Florida and Texas, whereas New Yorkers typically spend more on premium pet food and pet insurance.

Pet care investors should also consider the South as a whole. The region has one of the highest rates of pet ownership in the country, and it has among the top shares of the grooming and boarding markets. Additionally, disposable incomes are on the rise as the region experiences population surges and business expansions. Combined, these factors are driving significant growth in the region’s pet care industry.

Source: Grata

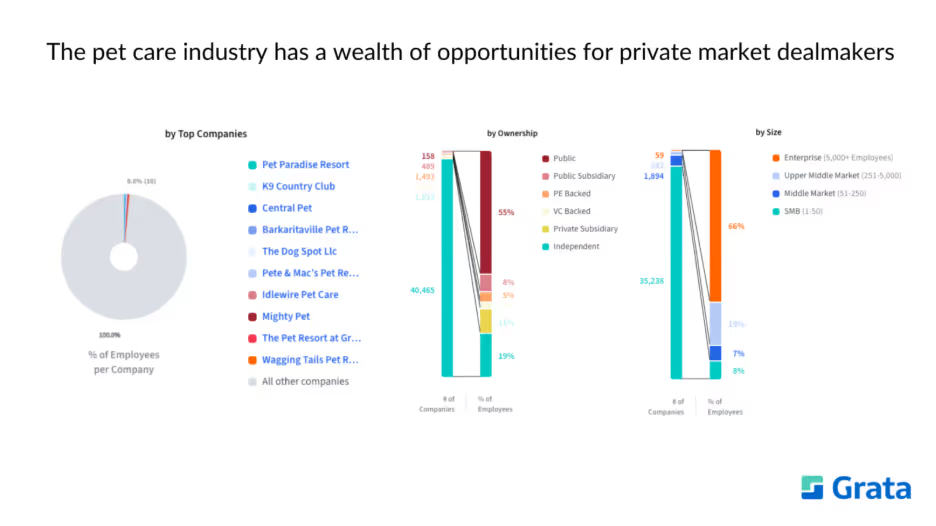

While public companies and their subsidiaries comprise over half of the pet care industry by ownership, the vast majority of companies operating in the space are independently owned. offering a deep pool of opportunities for private market investors.

Currently, there are over 40,000 private companies that are ripe for acquisition.

Source: Grata

This report focuses on the following segments of the pet care industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

Source: Grata

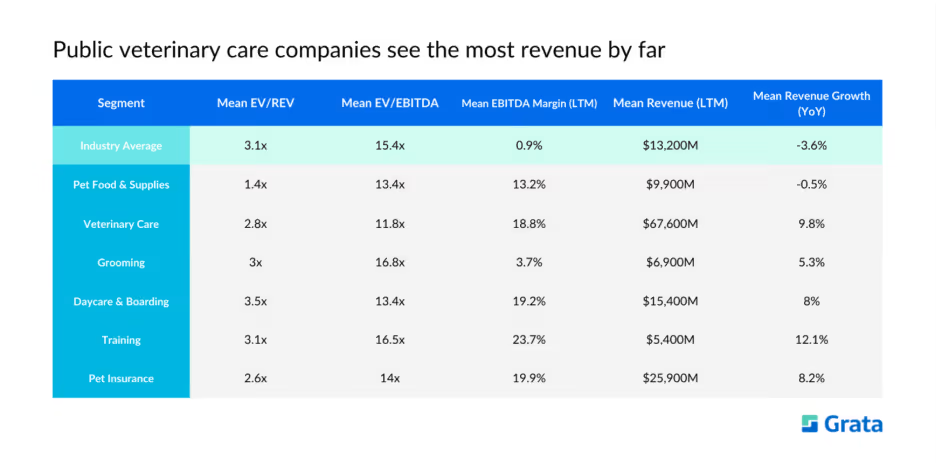

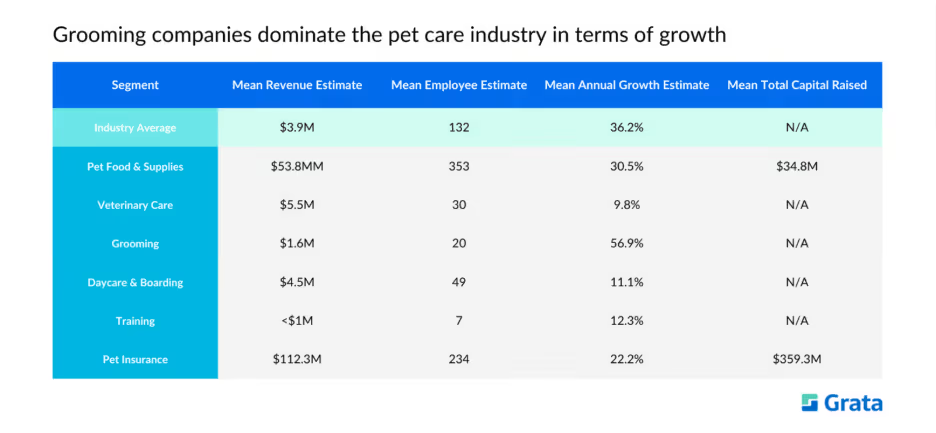

The veterinary care segment leads the industry in average revenue. It is also one of the top-performing sectors in terms of revenue growth. As mentioned in a previous section of this report, veterinary costs have increased by 24% between 2021 and 2026. This drove moderate revenue growth in 2025, even as the number of vet visits dropped.

Meanwhile, the pet training segment leads the pack in terms of growth, with an average annual rate of 12.1%. With pet ownership and the humanization of pets continuing to rise, behavioral training is in high demand. The pet training market is expected to grow at a CAGR of around 6% through 2026.

Pet insurance is another promising sector, as pet owners are increasingly purchasing plans for their cats and dogs. By the end of 2024, over 6.4M pets were insured in the US alone.

Companies in the food & supplies market typically see healthy margins, though they are seeing a slight decline in revenue growth amid rising costs for raw materials and supply chain issues.

Source: Grata

In the private sphere, grooming companies are seeing the highest average annual growth rate by a long shot. Millennial and Gen Z pet owners are big spenders when it comes to premium care for their furry friends. That includes grooming, which consumers are increasingly viewing as a health and wellness service rather than purely aesthetic. Modern grooming services also often provide dermatological treatments, flea and tick control, and more.

Dealmakers interested in the pet care industry should also consider the training sector. While it accounts for just 9.8% of the broader industry, and pet training companies see under $1M in average annual revenue, the sector is growing at a solid mean rate of 12.3%. Training facilities can also operate on relatively low costs, and they can become profitable quite quickly due to high demand.

Source: Grata

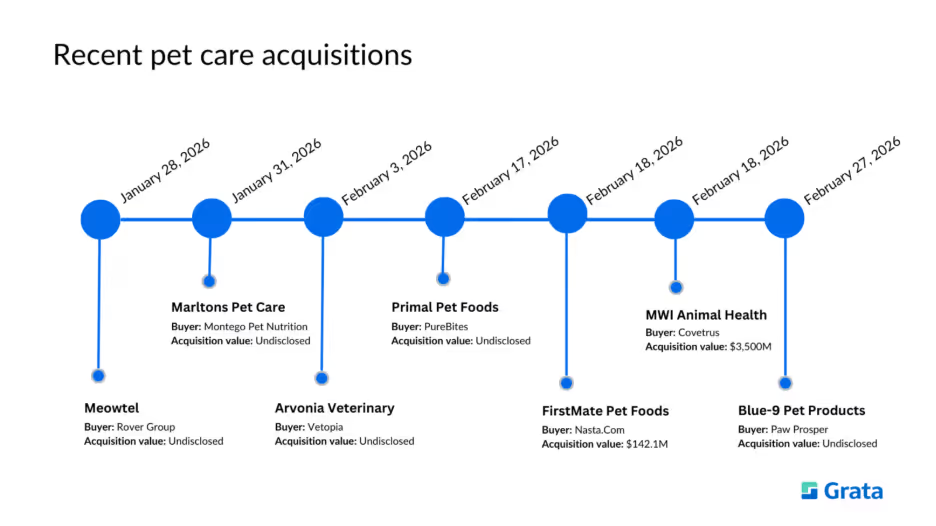

In January, Rover Group acquired Meowtel, an app-based marketplace that connects cat owners with vetted, background-checked cat sitters. Financial terms of the deal were not disclosed.

If you’re an investor interested in companies similar to Meowtel, try these:

Learn more about this acquisition — or any of the others listed below — anytime, anywhere using the latest version of the Grata Go mobile app. Get all of the ownership and investment data you need right in the palm of your hand.

Also in January, South Africa-based Montego Pet Nutrition purchased Marltons Pet Care. Marltons is also based in South Africa. The company produces and sells branded pet supplies, including a color-changing health-indicator crystal cat litter, as well as multiple cat and dog treat lines. Marltons sells direct to consumers online and through retail and veterinary channels.

If you’re an investor interested in companies similar to Marltons Pet Care, try these:

Vetopia, which operates a group of veterinary clinics in Europe, bought Arvonia Veterniary in February for an undisclosed amount. Arvonia provides veterinary surgery services, as well as accinations, neutering, dental treatments, surgical procedures, diagnostic imaging, laboratory work, and home visits.

If you’re an investor interested in companies similar to Arvonia Veterinary, try these:

Later in February, Canada-based pet food company PureBites acquired California-based Primal Pet Foods for an undisclosed amount. Primal Pet Foods manufactures and sells raw and raw-formulated food products for cats and dogs, including frozen raw diets, freeze-dried and dehydrated meals, raw bones and chews, supplements, and toppers.

If you’re an investor interested in companies similar to Primal Pet Foods, try these:

Premium pet food brand Nasta purchased FirstMate Pet Foods in February for just over $142M. FirstMate manufactures and sells dry and canned dog and cat foods and treats, including grain-friendly and grain-free lines, and limited-ingredient formulas.

If you’re an investor interested in companies similar to FirstMate Pet Foods, try these:

Maine-based Covetrus acquired MWI Animal Health, a wholesale distributor of animal health products and supplies, for $3.5B in February. MWI provides pharmaceuticals, vaccines, medical equipment, nutritional products, and practice supplies to veterinary clinics, livestock operations, companion animal practices, and other animal health providers.

If you’re an investor interested in companies similar to MWI Animal Health, try these:

In late February, Colorado-based pet health product brand Paw Prosper purchased Blue-9 Pet Products for an undisclosed amount. Blue-9 Pet Products designs and manufactures dog training equipment and accessories sold primarily to dog owners and professional trainers.

If you’re an investor interested in companies similar to Blue-9 Pet Products, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the pet care industry:

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

Grata makes it easy for dealmakers to find conferences, events, and trade shows in their industries. See attendee lists so you can set up meetings beforehand and make the most of your travel time. Check out which companies attended past events to find more potential targets.

Here are a few of the events related to the pet care industry that dealmakers can find and track in Grata:

If you’re an investor interested in making moves in the pet care space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

Schedule a demo today to get started.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)