Sourcing

How to Identify Companies Preparing to Sell Before the Competition

Learn how to identify companies preparing to sell before a formal process starts, using behavioral signals that flag seller intent 6–12 months early.

General freight trucking might not be the first industry that comes to mind when you think about whitespace for deal sourcing, but that’s part of what makes the space interesting.

In our latest screen of US mid-market companies, general freight trucking stood out as a large, still-growing subsector with relatively light visible acquisition activity. That doesn't mean buyers are absent, but visible M&A penetration looks lower than you might expect given the size of the market and the recent growth profile.

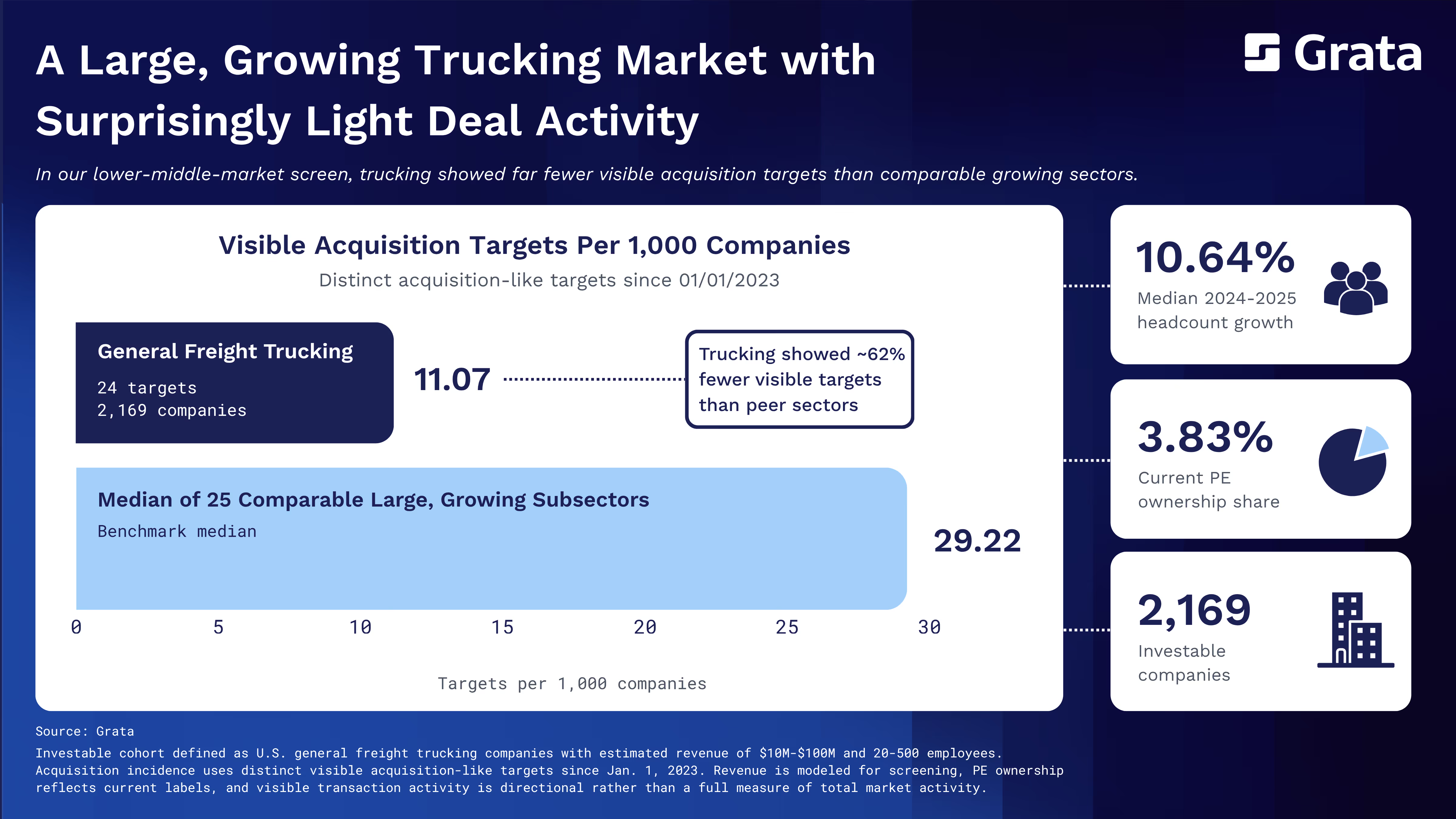

Our recent analysis focused on US-based companies in the General Freight Trucking industry (NAICS 4841) with estimated revenue of $10M-$100M and 20-500 employees. The cohort included 2,169 companies — a sizable pool of investable businesses.

What stood out was the gap between cohort size, recent growth, and visible target incidence. In the observed 2024-2025 employee panel, the subsector showed median headcount growth of 10.64%. But since 2023-01-01, only 24 distinct acquisition targets appeared in visible deal data. That works out to 11 visible targets per 1,000 companies.

To put that in context, we compared general freight trucking against 25 other large, growing subsectors screened on the same basis: U.S. companies, estimated revenue of $10M-$100M, 20-500 employees, and positive recent growth. Across that peer set, the median visible target incidence was 29 per 1,000 companies — more than double the level in general freight trucking.

Current PE ownership was also lighter than the peer median: 3.83% of general freight trucking companies were currently labeled as PE-owned, versus a 5.81% median across the comparable subsectors.

That combination makes the subsector worth paying attention to.

This is not a story about a niche market that happens to have low deal volume — it’s about a scaled market that still looks relatively light on visible acquisition activity and current PE ownership.

The founder and operator angle matters, too. A lot of mid-market owners hear the same story repeatedly: if a sector is attractive, it must already be crowded. This analysis suggests that is not always the case. In general freight trucking, the visible market picture looks more open than many other growing subsectors, even though the underlying company base is relatively large.

That said, the caveats are important:.

So, what is the right takeaway? In this cohort, general freight trucking looks like a scaled and growing subsector where visible acquisition activity and current PE ownership appear lighter than in many comparable markets. That makes a category that warrants closer examination for sourcing, coverage planning, and outbound market development.

In a market where many buyers are chasing the same well-worn narratives, that is tremendously valuable.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)