Data

What Is a Data Room? A Private Market Dealmaker’s Guide

Understand why private market deal teams need data rooms, the difference between a data room and a deal sourcing platform, and more.

.webp)

Farewell, summer — school is back in session.

Today’s classrooms look a lot different than they did even a decade ago. That’s largely because investment in education technology (ed tech) has increased over the last 10 years, bringing more digital tools to the classroom and beyond.

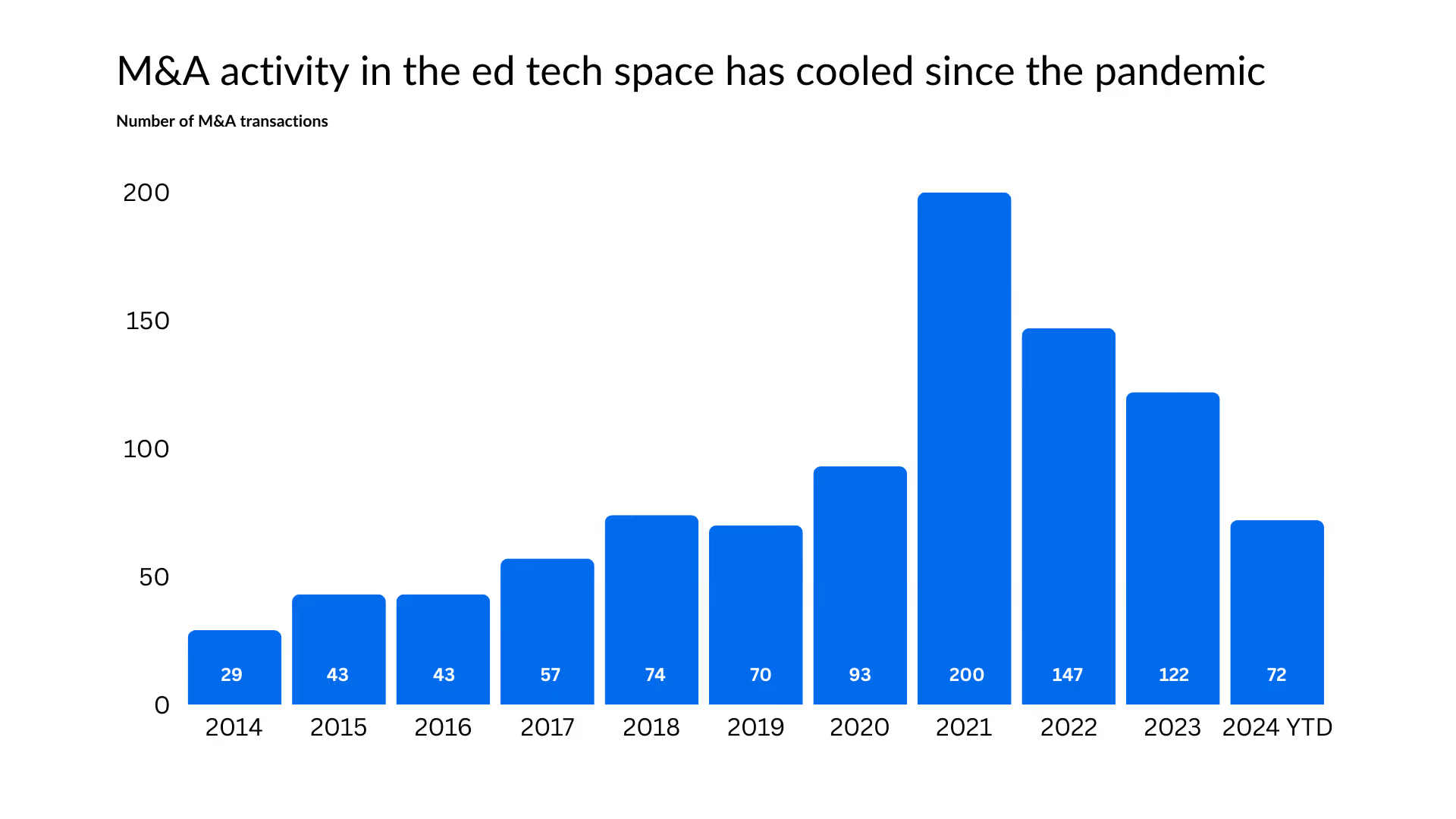

Private equity (PE) funding surged dramatically in 2020 and 2021, when classrooms were forced to go remote in the throes of the COVID-19 pandemic. Then, as the world reopened, and as investors tightened up their purse strings amid higher interest rates, that flurry of activity tapered off.

Source: Grata

So far in 2024, M&A transactions in the ed tech industry are at their lowest level since 2019. But that doesn’t mean PE investors should count ed tech out. With $2.6T of dry powder currently in PE, the space could still see an end-of-year bump.

And though funding totals are not expected to match pandemic levels, dealmakers can still find plenty of opportunities across in-demand segments like academic courses, early education, language acquisition, and career & technical certifications.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the ed tech market, including:

.avif)

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Source: Grata

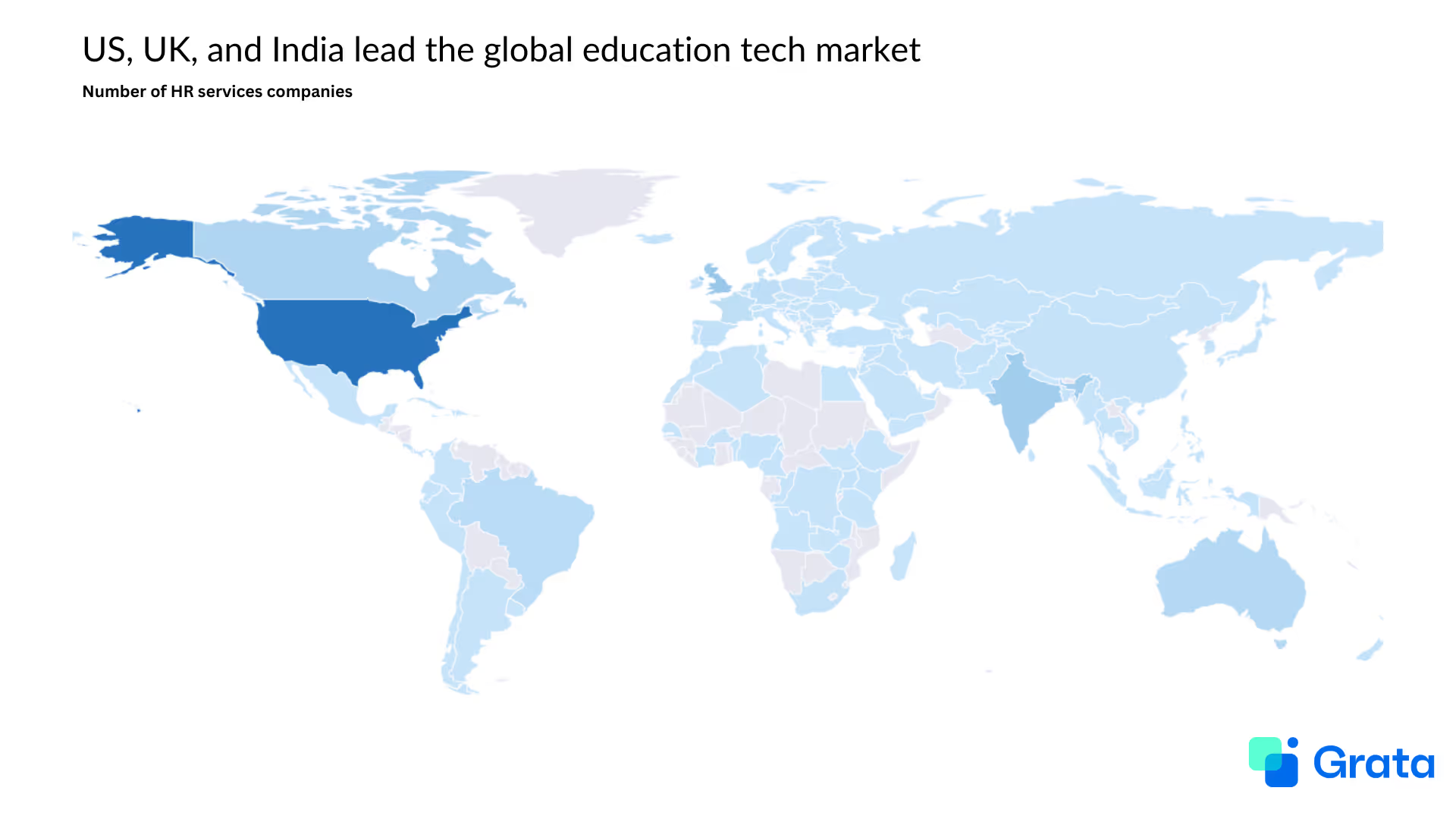

Ed tech is a globally distributed market, with the vast majority of companies located in the US, the UK, and India.

All three countries saw ed tech funding swell during the pandemic years, driving innovation and growth.

India’s market is also bolstered by significant government investment, the growing availability of high-speed internet, falling costs of smartphones, and increasing popularity of online learning.

Source: Grata

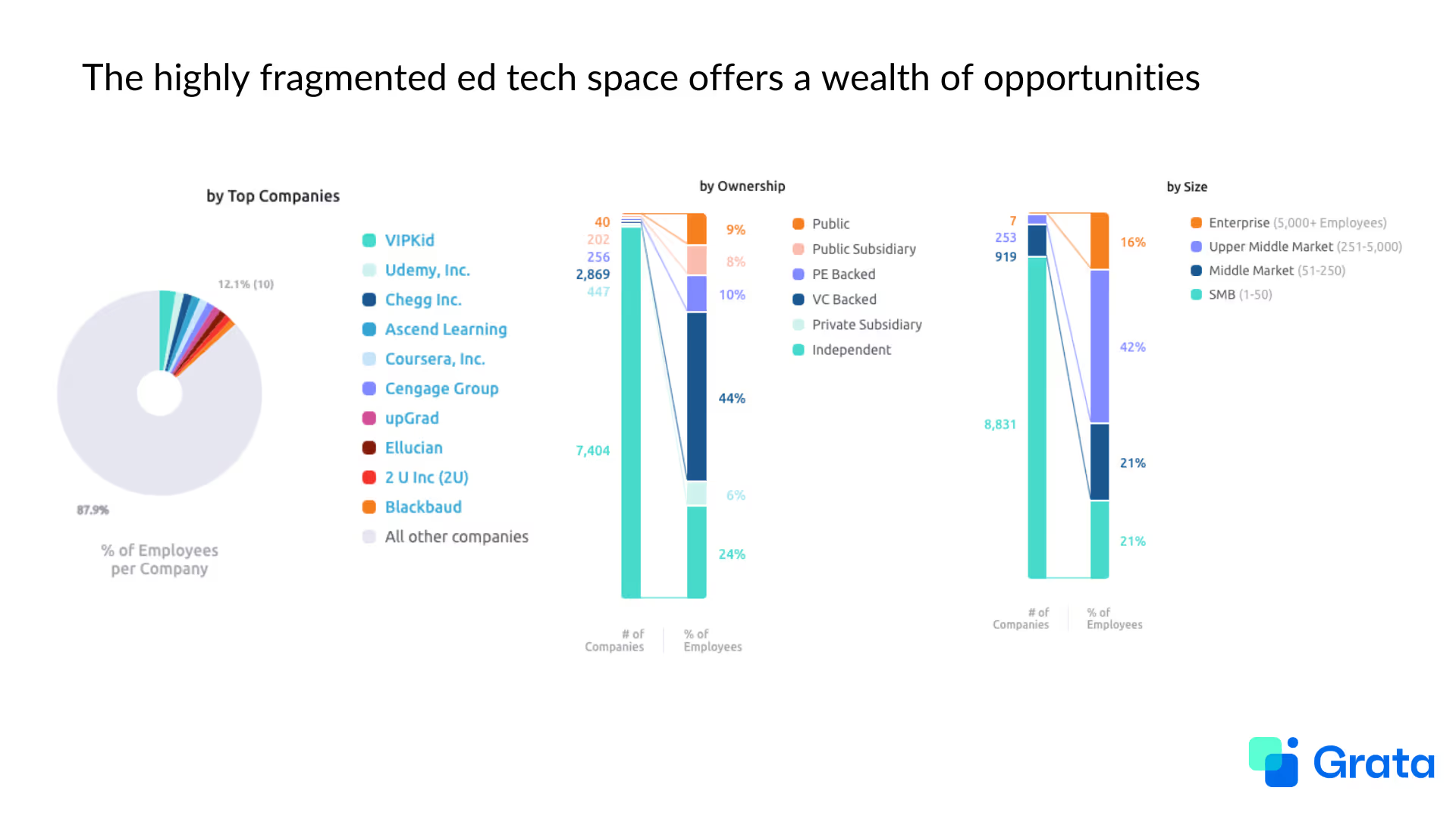

The vast majority of companies in the ed tech space are independently owned, offering a wealth of acquisition opportunities for PE dealmakers.

But private equity investors aren’t the only ones who have poured funds into the ed tech industry. Venture capitalists (VC) have been drawn to the space’s technology-driven innovation for years. As shown above, VC-backed companies account for 44% of industry share.

Like PE transactions, VC activity in the ed tech space also surged during 2020 and 2021, but has since cooled. Over the last 12 months, VCs have closed a flurry of investments to early-stage startups in the industry, which we cover more later in the report.

Meanwhile, Grata data shows that there are currently at least 267 late-stage startups in the space, with a combined total of $7.7B in funding. PE investors should keep an eye on these companies as they could offer opportunities for exit deals later on.

Source: Grata

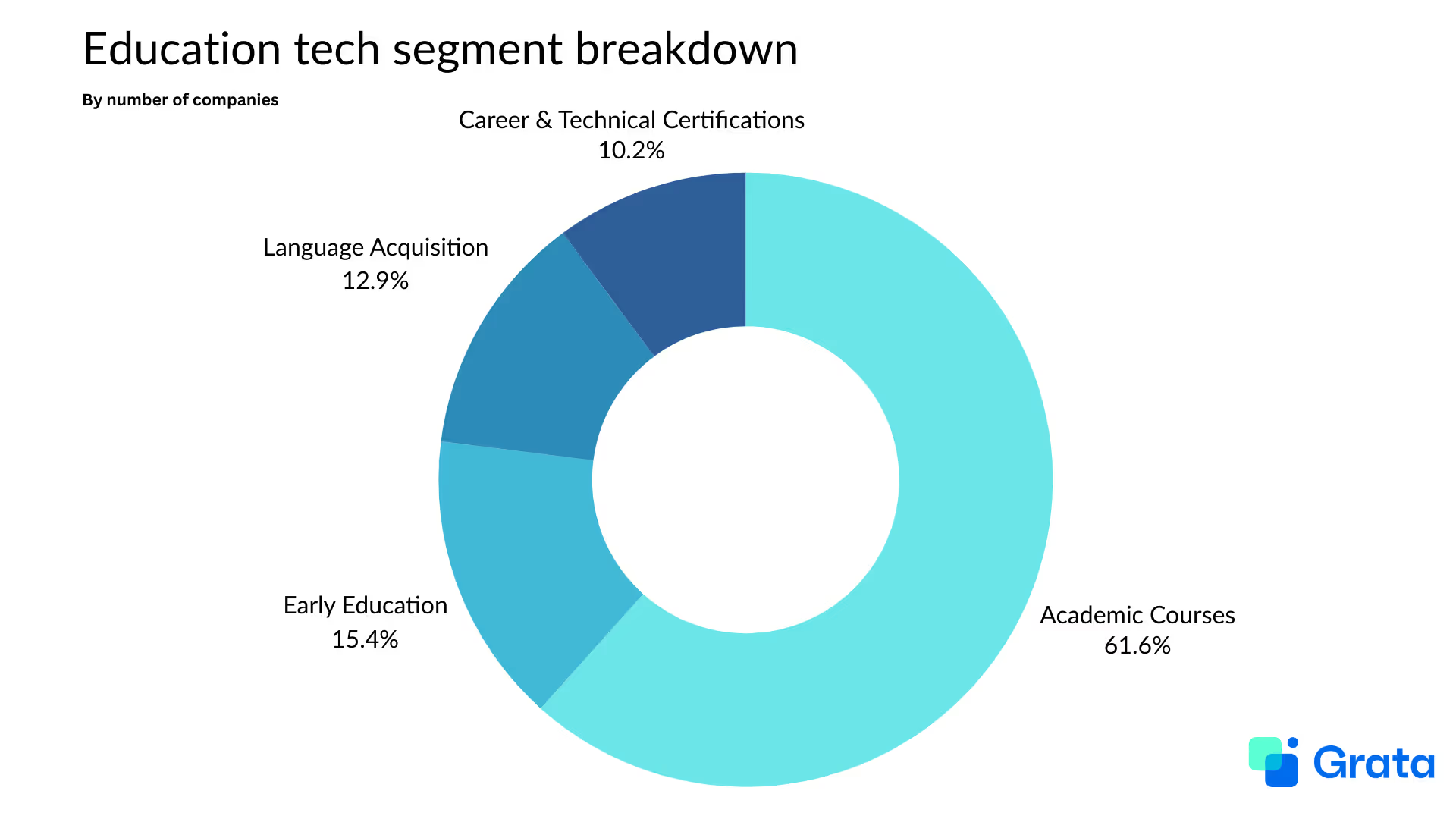

This report focuses on the following segments of the education tech industry. Grata users can see a curated list of some of the companies used to create each segment by clicking the links below.

Source: Grata

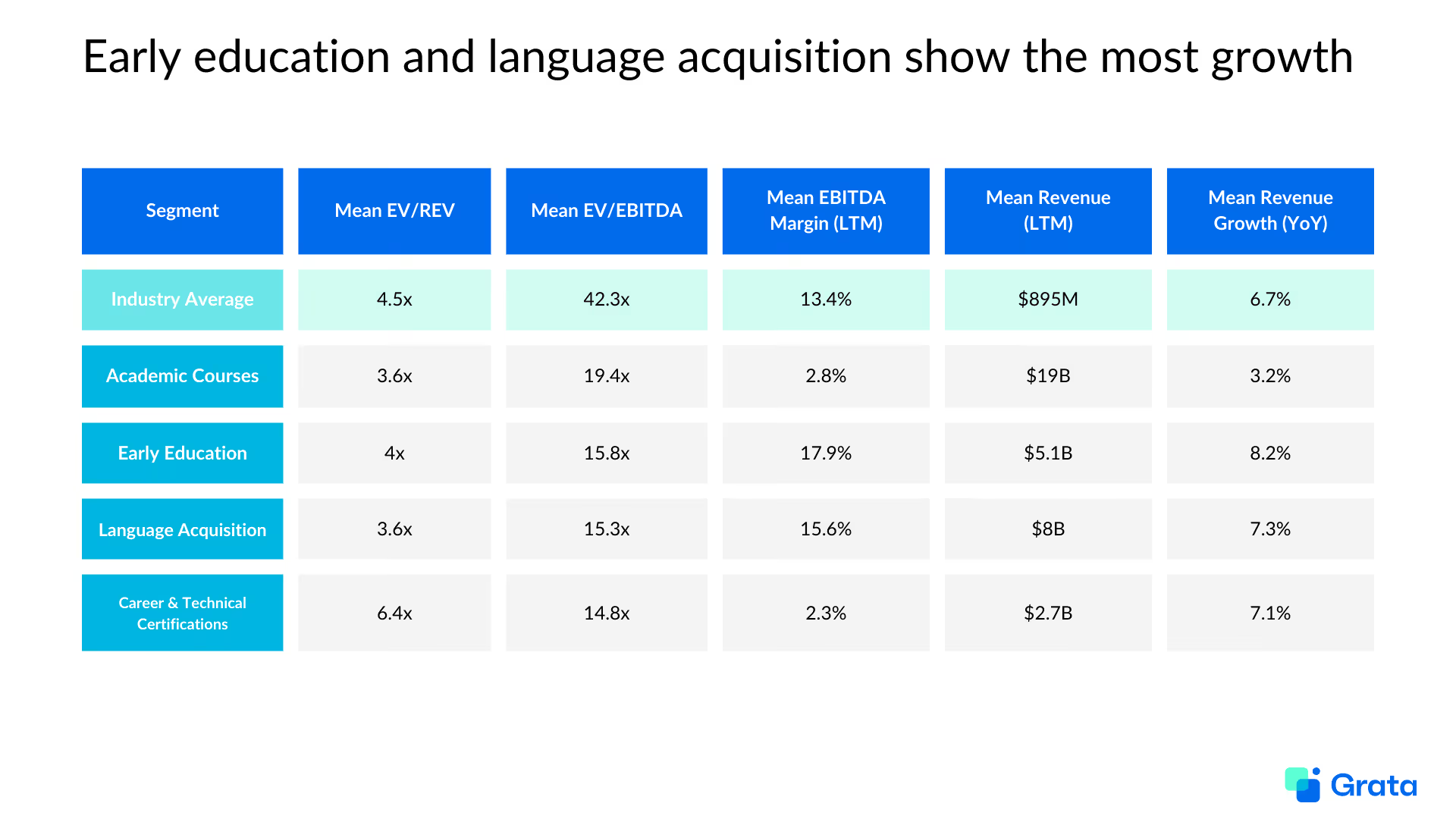

Investors looking to make moves in the ed tech space should look to early education, the fastest-growing of the segments analyzed in this report.

Demand for quality early childhood education (ECE) programs is on the rise around the globe. In response, ECE facilities are increasingly weaving tech into their programs to provide more holistic and personalized experiences.

With steady demand and an average EBITDA margin of 17.9%, investors could see healthy returns on early education deals.

The language acquisition space is also seeing a growth rate above the industry average and healthy average EBITDA margins. At the macro level, this is driven by globalization. The world is more interconnected and diverse than ever before, and people are becoming increasingly aware of the importance of multilingualism in their personal and professional lives. Meanwhile, the rise of AI is enabling convenient, low-cost language learning tools and apps that can be used just about anywhere.

Combined, these factors make the language acquisition space a great opportunity for any dealmakers who are also interested in HR services, which we dug into here.

.avif)

Source: Grata

Dealmakers who are also interested in the HR Services industry should look to the career & technical certifications segment. As tech continues to infiltrate the workplace, professional upskilling is only becoming more important. Employers estimate that 44% of employee skills will be disrupted in the next five years, and to keep up, six out of 10 employees will need some kind of training before 2027, according to a World Economic Forum report.

The career & technical certification market has raised only a small amount of capital and it’s growing at an average rate of 6.9% per year, signaling an opportunity for dealmakers to establish themselves as leaders in the space.

Similarly, the academic courses segment has relatively little capital raised compared to the industry average, and it has the highest average annual growth rate of the markets analyzed in this report.

Even with in-person learning back in session after the pandemic, there is still ample demand for options that give students more flexibility with scheduling and costs.

As the largest ed tech segment analyzed here, the academic courses sector offers a wealth of opportunities for dealmakers to find targets that fit their investment theses.

Source: Grata

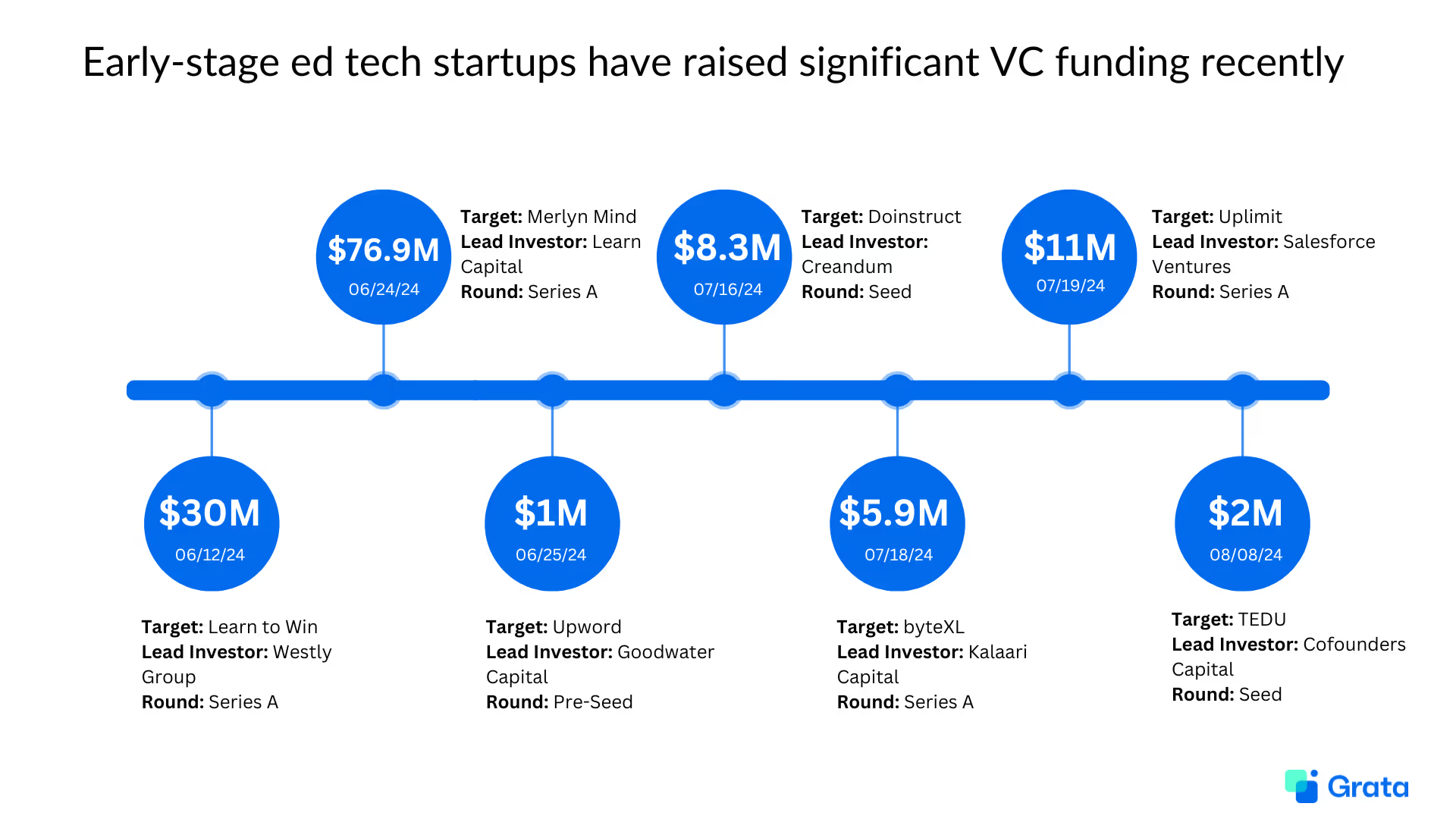

The vast majority of VC and growth deals in the ed tech space in the last year have gone to early-stage (Pre-Seed, Seed, or Series A) companies. Tony Wan, head of product at Reach Capital, says that generative AI is a major reason for the continued optimism in early-stage startups, because the tech “makes it easier to build a prototype, ship it out, and test your product.”

In just the last two months, early-stage companies across ed tech segments have raised sizable rounds from investors like Salesforce Ventures, Cofounders Capital, Kalaari Capital, and more.

Source: Grata

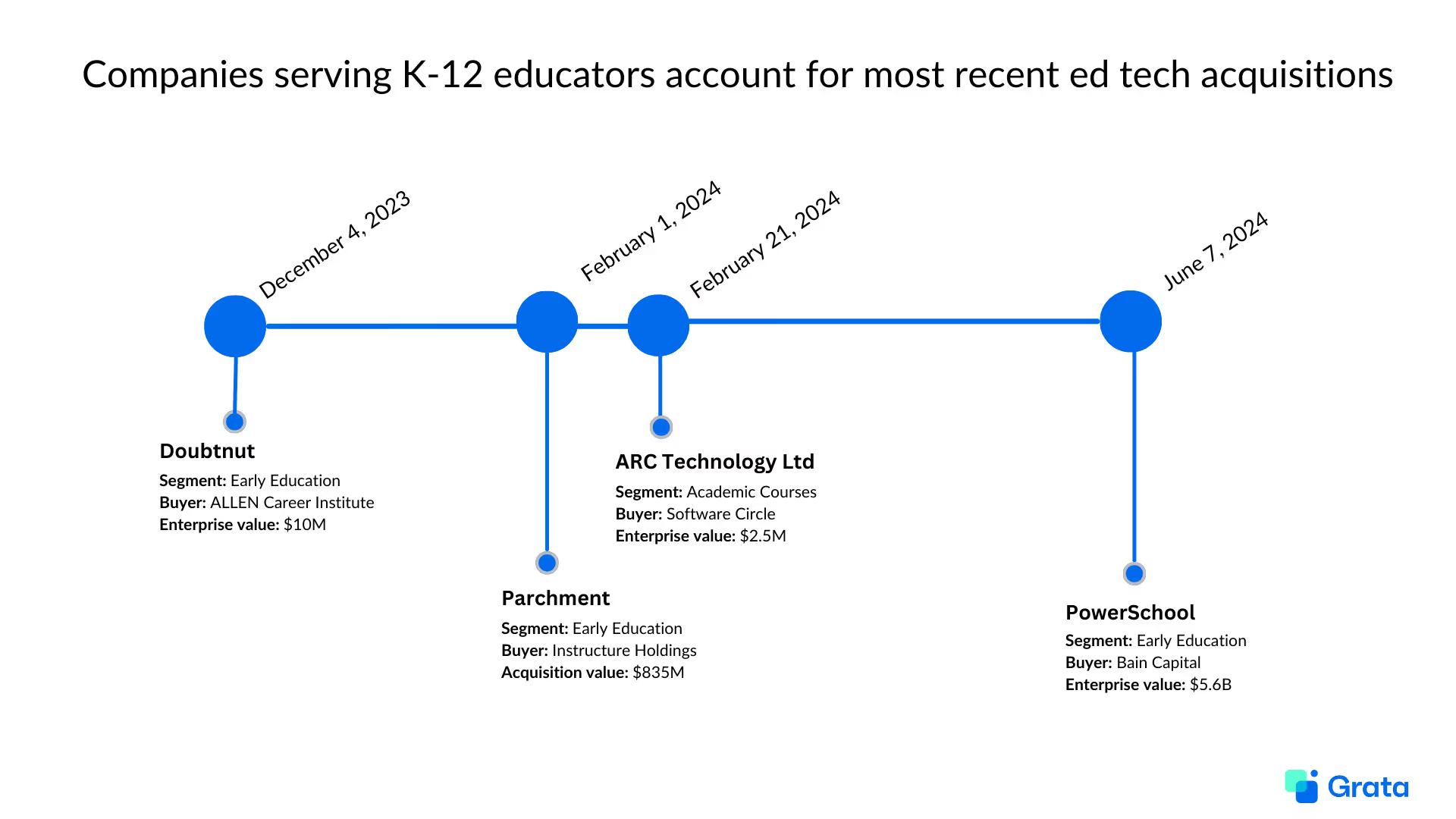

As mentioned earlier, tech solutions that cater to the early education sector are in high demand. Early education tech companies account for the vast majority of recent acquisitions in the ed tech industry.

In December, Allen Career Institute acquired Doubtnut, a problem solving and test prep platform with an enterprise value of $10M.

Allen Career Institute is a coaching business that has operated primarily offline. The company said acquiring Doubtnut would help build out its learning tech arsenal.

If you’re an investor interested in companies similar to Doubtnut, try these:

Ed tech leader Instructure completed its $835M acquisition of Parchment in February. Parchment’s platform allows academic institutions, mainly in the K-12 space, the ability to manage transcripts, diplomas, digital certifications, and more.

Steve Daly, Instructure’s CEO, said the deal “enables [Instructure’s] customers to offer flexible lifelong learning experiences to meet the needs of the ever-growing sector of non-traditional learners.”

If you’re an investor interested in companies similar to Parchment, try these:

In June, Bain Capital announced its acquisition of K-12 SaaS company PowerSchool in a deal that valued the company at $5.6B.

Hardeep Gulati, CEO of PowerSchool, said the deal would give the company the additional resources and flexibility to grow its genAI platform PowerBuddy and help schools personalize education for their students.

If you’re an investor interested in companies similar to PowerSchool, try these:

Software Circle, fka Grafenia, purchased ARC Technology, which provides higher education software to universities and colleges in the UK. The deal valued ARC at around $2.5M.

If you’re an investor interested in companies similar to ARC Technology, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here’s an example of a mandate related to the education techindustry:

If you’re interested in this deal and you want to source more live deals in the education tech space, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

If you’re an investor interested in making moves in the ed tech space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

Schedule a demo today to get started.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)