Sourcing

How to Identify Companies Preparing to Sell Before the Competition

Learn how to identify companies preparing to sell before a formal process starts, using behavioral signals that flag seller intent 6–12 months early.

.webp)

The construction industry is booming, and private market investors have more reasons than ever to pay attention.

Infrastructure investment, data center buildout, power-related projects supporting AI, and energy transition projects are generating strong demand for construction services.

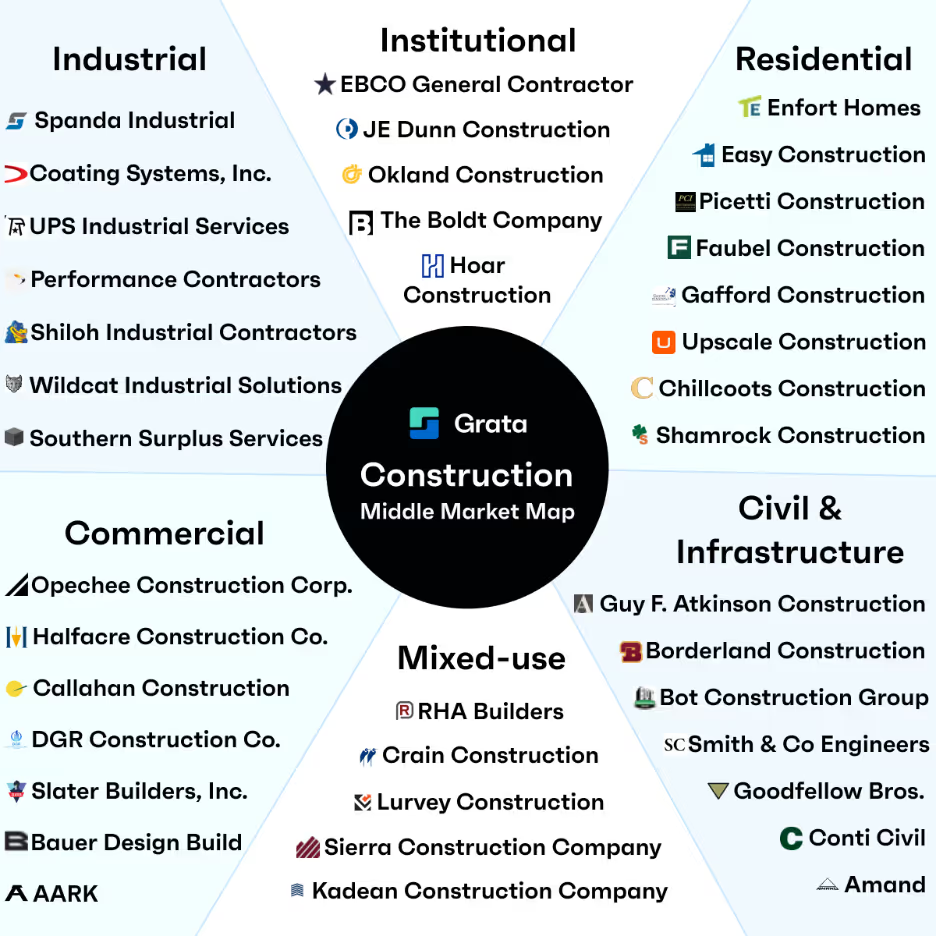

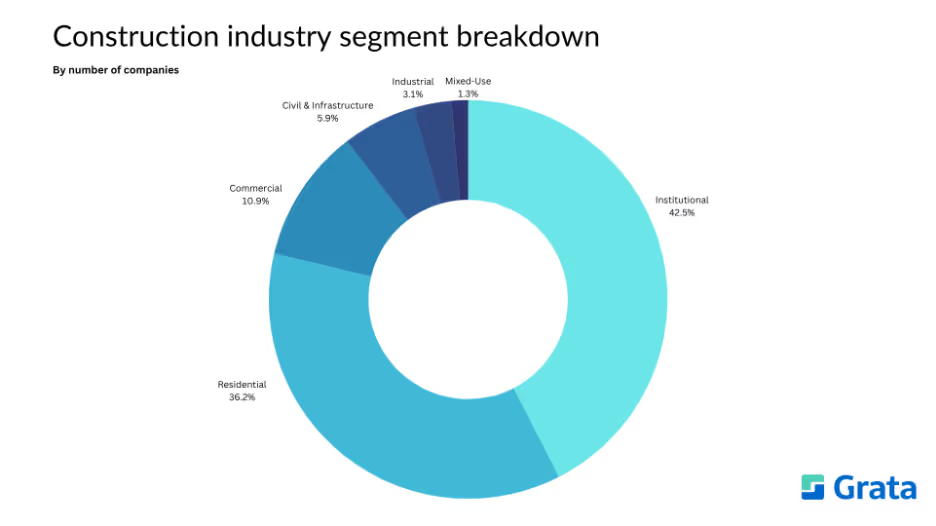

With well over 600,000 privately owned companies across the industrial, institutional, residential, civil & infrastructure, mixed-use, and commercial sectors, the construction industry offers a wealth of opportunities for private market dealmakers.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the construction industry, including:

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Source: Grata

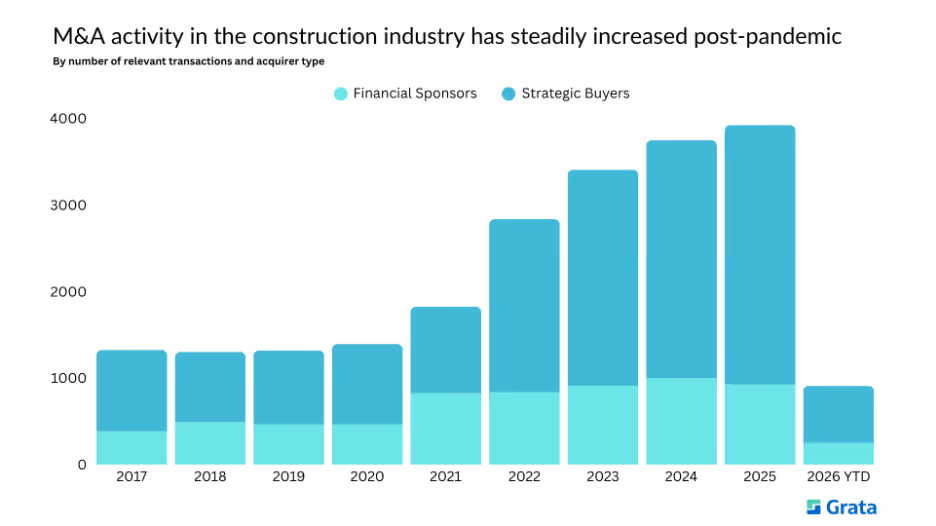

Total M&A transactions in the construction industry have nearly quadrupled since 2017. The space really gained momentum after 2020 amid a rush of boomer-owned business successions and over $5T in government infrastructure programs unlocked massive project pipelines.

Source: Grata

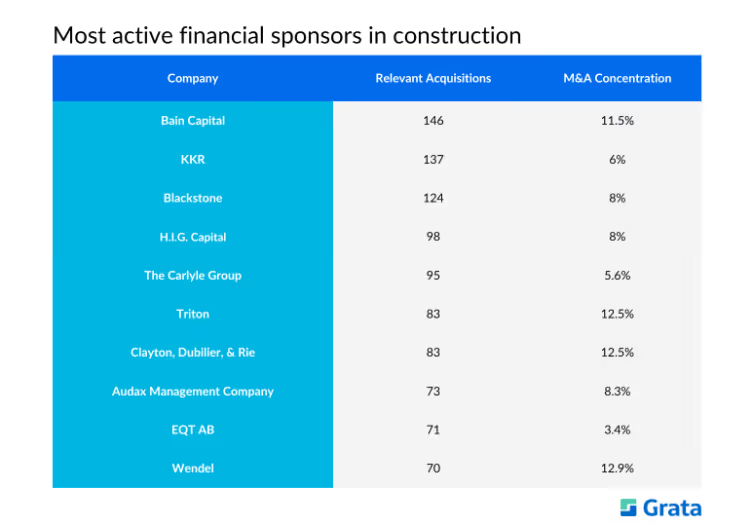

Bain Capital tops the list of most active financial sponsors in the construction industry with 146 relevant deals. Several of its transactions are focused on the mixed-use sector.

Source: Grata

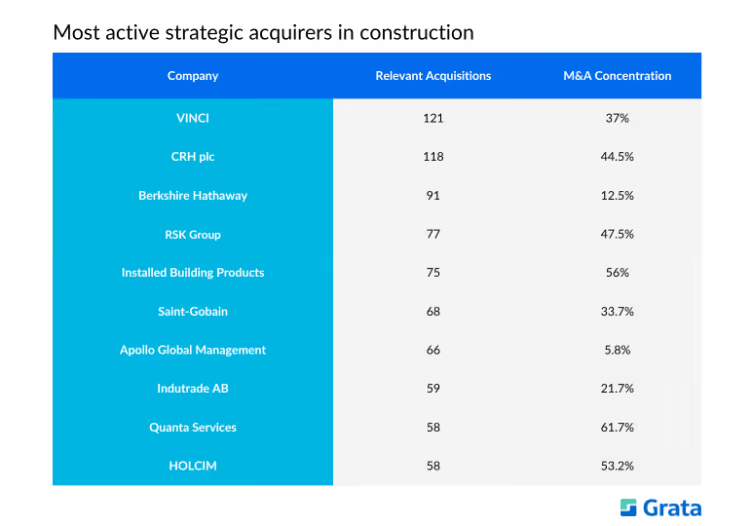

VINCI is the most active strategic acquirer in the construction industry. Many of its relevant acquisitions focus on civil & infrastructure construction.

Source: Grata

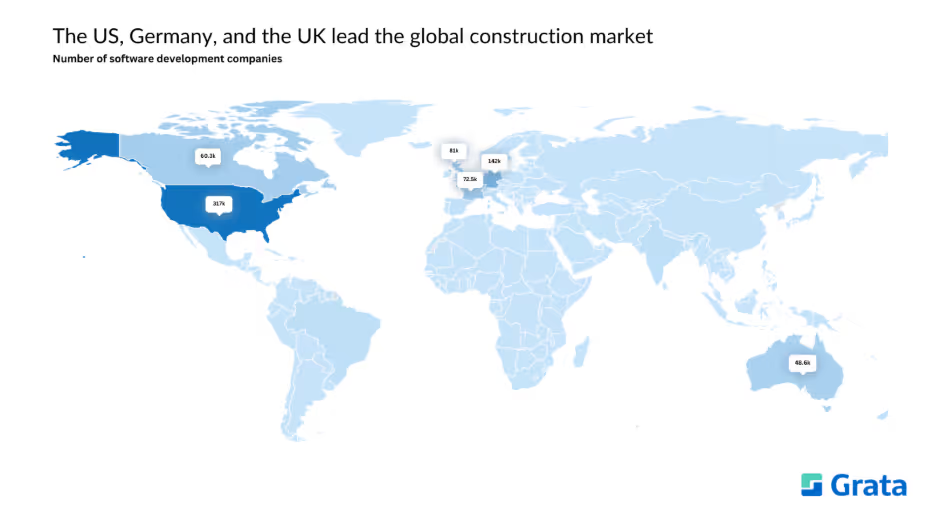

The US, Germany, and the UK lead the global construction market by number of companies in the industry. Other key players include France, Canada, and Australia.

Source: Grata

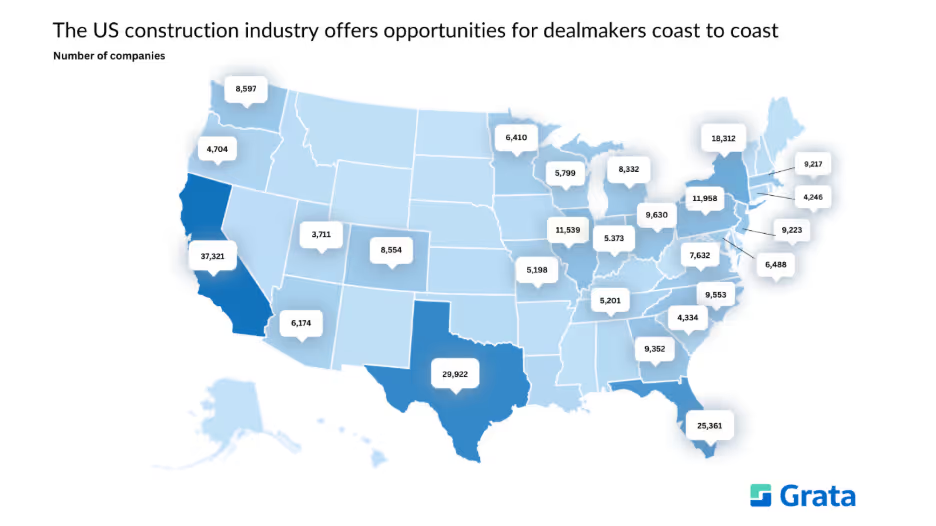

For US-focused dealmakers, there is no shortage of opportunity in the construction industry. Here are some key factors and regions to consider:

Source: Grata

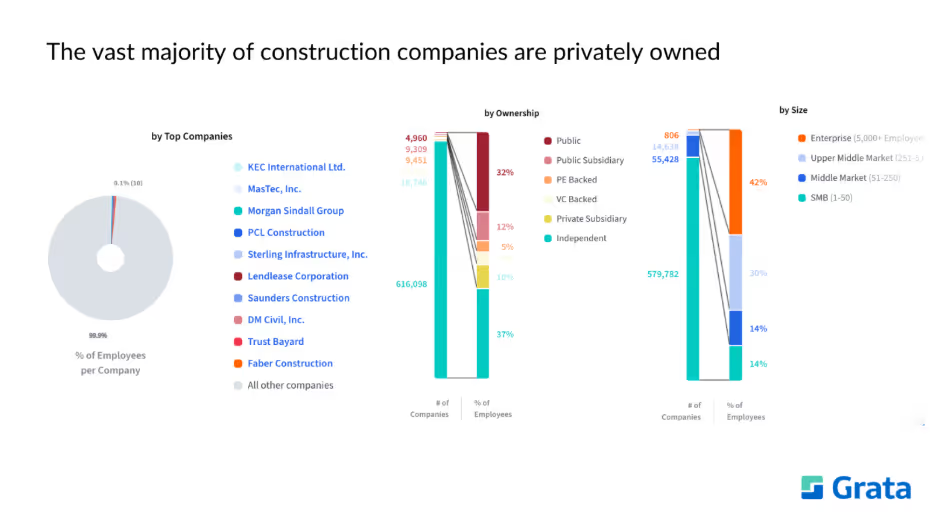

The construction industry is highly fragmented, with the overwhelming majority of companies being independently owned. There are currently over 630,000 private construction companies that are ripe for acquisition.

Source: Grata

This report focuses on the following segments of the construction industry:.

Source: Grata

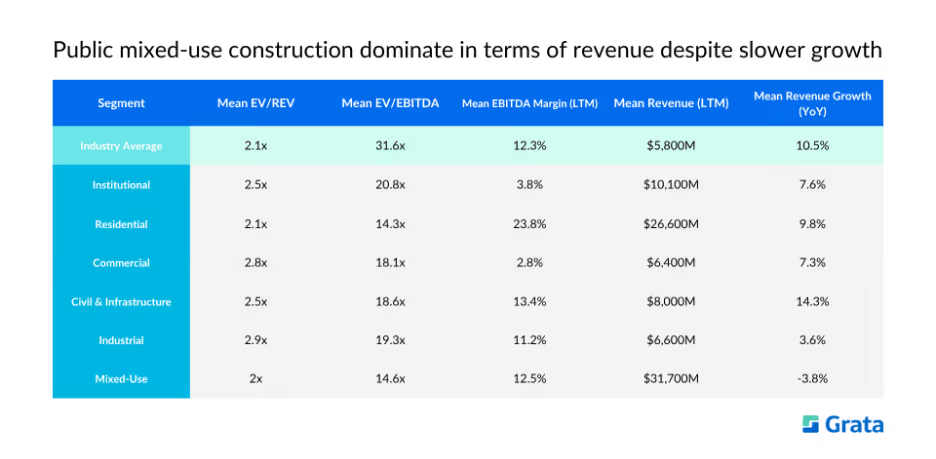

In the public realm, the mixed-use sector is far and away the leader in average revenue, with $31.7B. That number reflects the sheer scale of mixed-use projects. Developments that combine residential, retail, commercial, and hospitality components naturally generate some of the largest single-contract values in the industry. The boom in office-to-residential conversion has also supercharged the sector: converted offices created a record 70,700 apartments in 2025, up from 23,100 in 2022. Major cities like Chicago, New York, and Boston are deploying hundreds of millions in tax incentives to make these projects financially viable.

The -3.8% mean revenue decline in the mixed-use sector, however, tells the other side of the story. The pool of ideal conversion candidates is shrinking, while high labor costs, materials prices, and financial constraints are making new speculative mixed-use development projects increasingly difficult to underwrite. In short, the revenue is real, but it's being sustained by a wave of conversion activity that has a natural limit.

Meanwhile, the civil & infrastructure sector leads in terms of average revenue growth at 14.3%. Global infrastructure construction output grew by around 4.7% last year amid ongoing urbanization and investment across energy, transport, and utility systems. Aging infrastructure, energy transition investments, and digitization continue to push governments around the world to spend heavily on civil projects.

And then there’s the residential sector, the obvious margin leader. With an average margin of 23.8%, residential construction companies are typically more profitable than their peers in other segments. However, higher mortgage rates have slowed both single-family and multifamily construction. Many homeowners are staying put to preserve the low rates they locked in previously. This could be an attractive entry point for dealmakers looking toward the medium-term. The underlying housing shortage hasn't disappeared, and margins should hold once financing conditions ease.

Source: Grata

In the private sphere, institutional construction companies see the most average revenue. However, the sector’s story is really about stability rather than growth, underpinned by non-profit and government funding instead of private demand. Individual contracts can be enormous, skewing the sector’s average. In the US, for example, major projects like IU Health's $4.3B Indianapolis Hospital and Tutor Perini's $960M UCSF Children's Hospital illustrate that point. But institutional planning dropped in January 2026 due to slowdowns in education, healthcare, and public building plans. and new federal legislation is introducing funding uncertainties for health systems that could slow the pipeline if hospitals tighten capital budgets.

Still, the institutional sector does contain large, cash-generative businesses with no significant outside capital raised. These are classic founder-owned firms with sticky institutional client relationships that have never needed external financing, meaning they could be prime succession candidates as owners age out.

The private industrial sector dominates in terms of average growth. At 19.5%, private industrial construction companies are growing significantly faster than their private peers and their public counterparts. This gap likely has to do with smaller private firms being more agile, and thus better able to capture niche manufacturing and data center-related work than larger public players. Dealmakers may be able to create significant value by snapping up high-growth private industrial construction companies before they reach scale.

Source: Grata

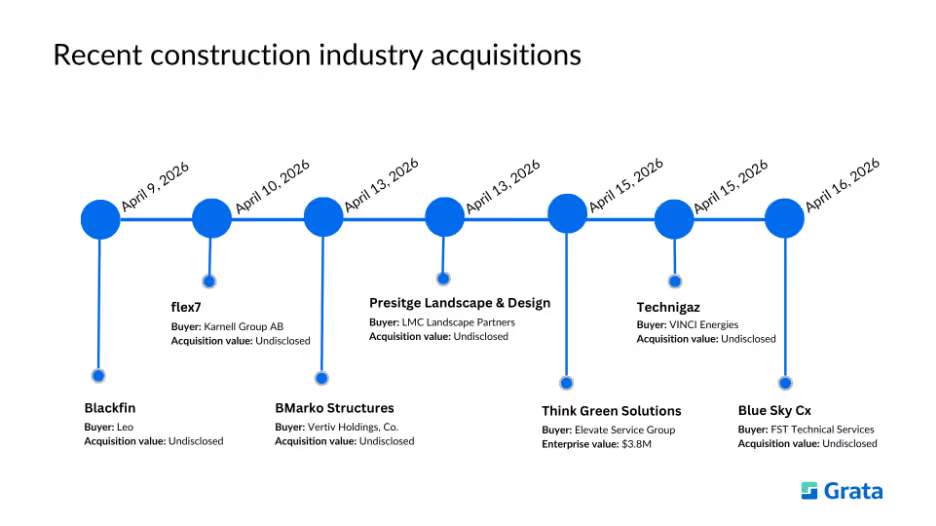

Earlier in April, Leo, which provides commercial facilities maintenance services to businesses, acquired Blackfin. Blackfin is a Kansas-based building engineering and facility operations firm specializing in commercial real estate maintenance. The company provides outsourced building engineering, preventative maintenance, emergency response, and strategic facility consulting services. Its customers consist of commercial property managers, real estate investment firms, and healthcare facility directors.

If you’re an investor interested in companies similar to Blackfin, try these:

Learn more about this acquisition — or any of the others listed below — anytime, anywhere using the latest version of the Grata Go mobile app. Get all of the ownership and investment data you need right in the palm of your hand.

Sweden-based industrial holding group Karnell purchased Flex7 for an undisclosed amount. Flex7 is based in the UK. It manufactures and supplies a modular lighting connection and control system for commercial building projects across the education, healthcare, public, retail, and transport sectors.

If you’re an investor interested in companies similar to Flex7, try these:

Earlier this month, Vertiv Holdings purchased BMarko Structures, which manufactures configurable steel modular buildings and shipping-container conversions for commercial and industrial customers. It also supplies engineered power distribution and equipment enclosures. BMarko Structures targets businesses and institutions that need prefabricated site-ready structures, such as offices, retail, industrial enclosures, data and energy systems.

If you’re an investor interested in companies similar to BMarko Structures, try these:

LMC Landscape Partners bought Prestige Landscape & Design for an undisclosed amount earlier this month. Prestige offers residential and commercial landscape design-build services focused on designing and installing outdoor living spaces and hardscapes. It provides irrigation, drainage, lighting, turf, tree care, and maintenance. The company also delivers 2D/3D designs, transparent proposals, climate-appropriate materials, and end-to-end project management.

If you’re an investor interested in companies similar to Prestige Landscape & Design, try these:

Also in April, Elevate Service Group, which provides facility maintenance and commercial services in Canada, acquired Think Green Solutions in a deal valued at $3.8M. Think Green provides turnkey commercial and industrial LED lighting retrofit services — including design, installation, financing, and maintenance — targeting businesses with large, long-hours facilities.

If you’re an investor interested in companies similar to Think Green Solutions, try these:

France-based technical engineering firm VINCI Energies purchased Technigaz in April. Technigaz is a Canada-based industrial construction and contracting firm that focuses on industrial electrical systems, instrumentation, automation, combustion systems, piping, and engineering. It serves industrial clients such as chemical, petrochemical, energy, manufacturing, metallurgy, mining, pulp and paper, and water treatment businesses.

If you’re an investor interested in companies similar to Technigaz, try these:

Arizona-based FST Technical Services, which provides testing, inspection, certification, and engineering services, acquired Blue Sky Cx in April. Blue Sky Cx provides building commissioning and retro-commissioning, facility assessments, and mechanical and HVAC testing for building owners, facility managers, healthcare facilities, and similar organizations. The company emphasizes commissioning, retro-commissioning, and specialized testing as core offerings to optimize building systems.

If you’re an investor interested in companies similar to Blue Sky Cx, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the construction industry:

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

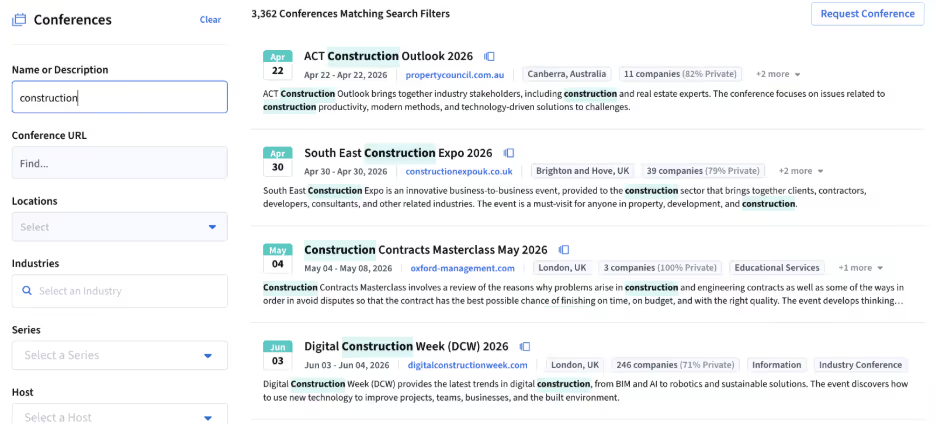

Grata makes it easy for dealmakers to find conferences, events, and trade shows in their industries. See attendee lists so you can set up meetings beforehand and make the most of your travel time. Check out which companies attended past events to find more potential targets.

Here are a few of the events related to the construction industry that dealmakers can find and track in Grata:

Source: Grata

If you’re an investor interested in making moves in the construction space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

Schedule a demo today to get started.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)