Sourcing

How to Identify Companies Preparing to Sell Before the Competition

Learn how to identify companies preparing to sell before a formal process starts, using behavioral signals that flag seller intent 6–12 months early.

.webp)

Private equity (PE) in healthcare seems to be in for a shake-up.

Last month, California’s legislature voted to approve Assembly Bill 3129, which requires the state’s Attorney General to be notified and to review healthcare transactions involving PE groups and hedge funds. Healthcare organizations included in the scope of the bill include clinics, outpatient settings, ambulatory surgery centers, clinical laboratories, and imaging facilities.

Though governor Gavin Newsome vetoed the bill, PE activity in healthcare is still under the microscope. At least 5 others are considering legislation that would regulate how — and if — PE firms acquire healthcare facilities. With larger deals likely to come under scrutiny in the near future, PE investors should focus on smaller deals and improving the industry.

With larger deals likely to come under scrutiny in the near future, PE investors should focus on smaller deals and improving the industry.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the healthcare practices market, including:

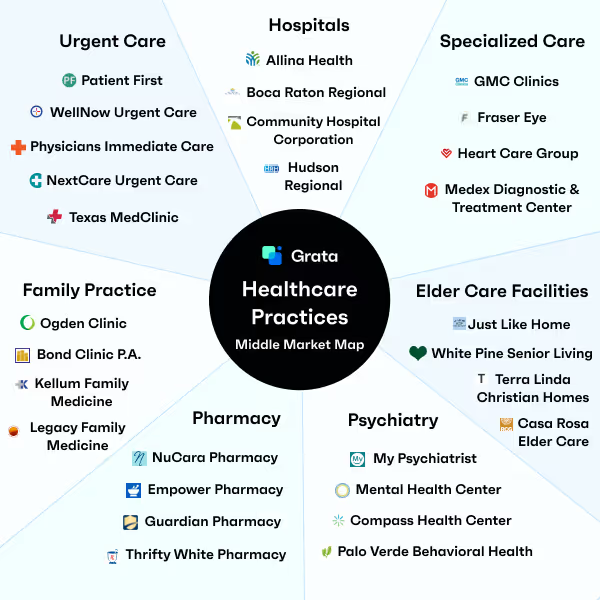

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

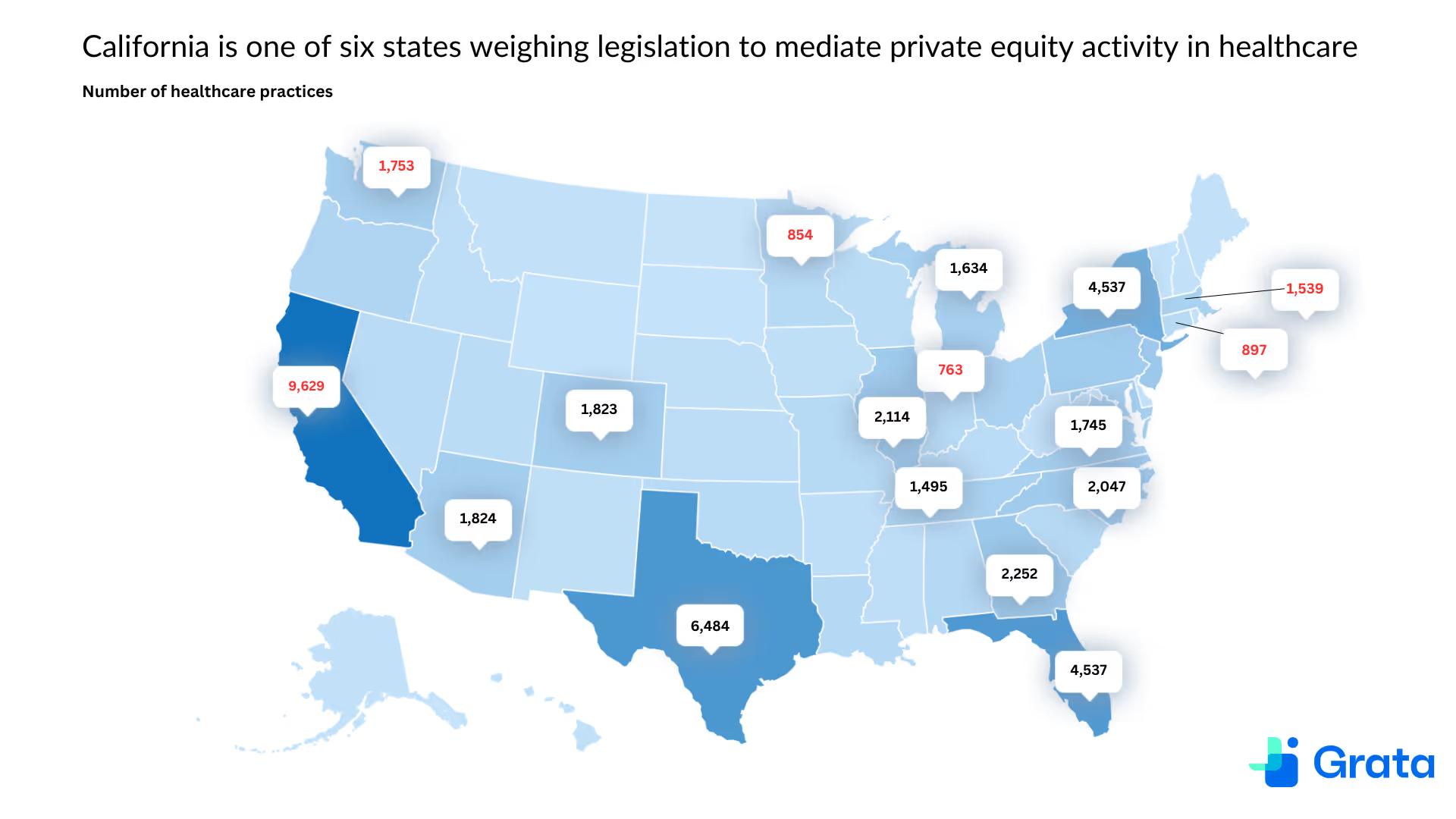

Source: Grata. Red text indicates the state has either enacted or is considering legislation to regulate private equity activity in the healthcare space.

So far, Indiana is the only state that has enacted restrictions on PE transactions in healthcare. This July, the state’s min-HSR Act went into effect, making a transaction between a “private equity partnership” and a “health care entity” — which could include a healthcare provider, payor, health maintenance organization, pharmacy benefit manager, or third-party administrator — “likely reportable,” according to Morgan Lewis. The law can also be interpreted as covering out-of-state PE sponsors acquiring healthcare organizations based in Indiana.

Similar mini-HSR acts are already in effect in California, Connecticut, Massachusetts, Minnesota, and Oregon. These states are also considering new private equity disclosure regulations, which would supplement the mini-HSRs if they pass.

These six are among the states with the most healthcare practices, but there are also a plethora of states with no current regulations and well over 1,000 healthcare practices ripe for acquisition.

Source: Grata

There are currently over 58,000 healthcare practice companies that are ripe for acquisition. Private equity dealmakers looking to make moves in the space will need to take extra care to stay up to date on transaction disclosure laws as they move through state legislatures.

PE investors targeting pharmacies may have an added challenge in going up against leading corporations like Walmart, Walgreens, CVS, and Rite Aid. However, the high-growth, high-revenue space could offer high returns. We dig into this more in the comps sections.

.avif)

Source: Grata

This report focuses on the following healthcare practice segments. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

Source: Grata

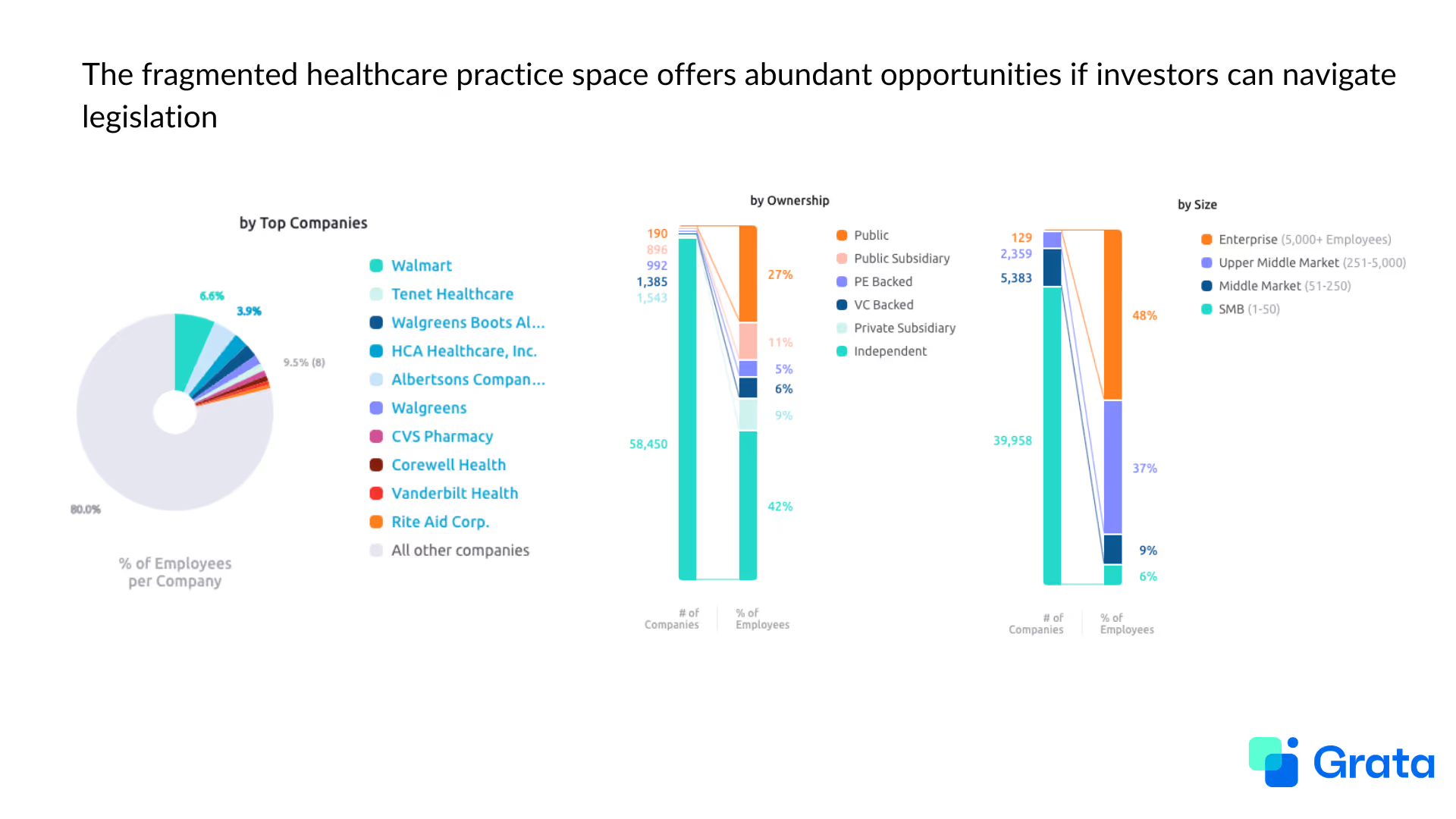

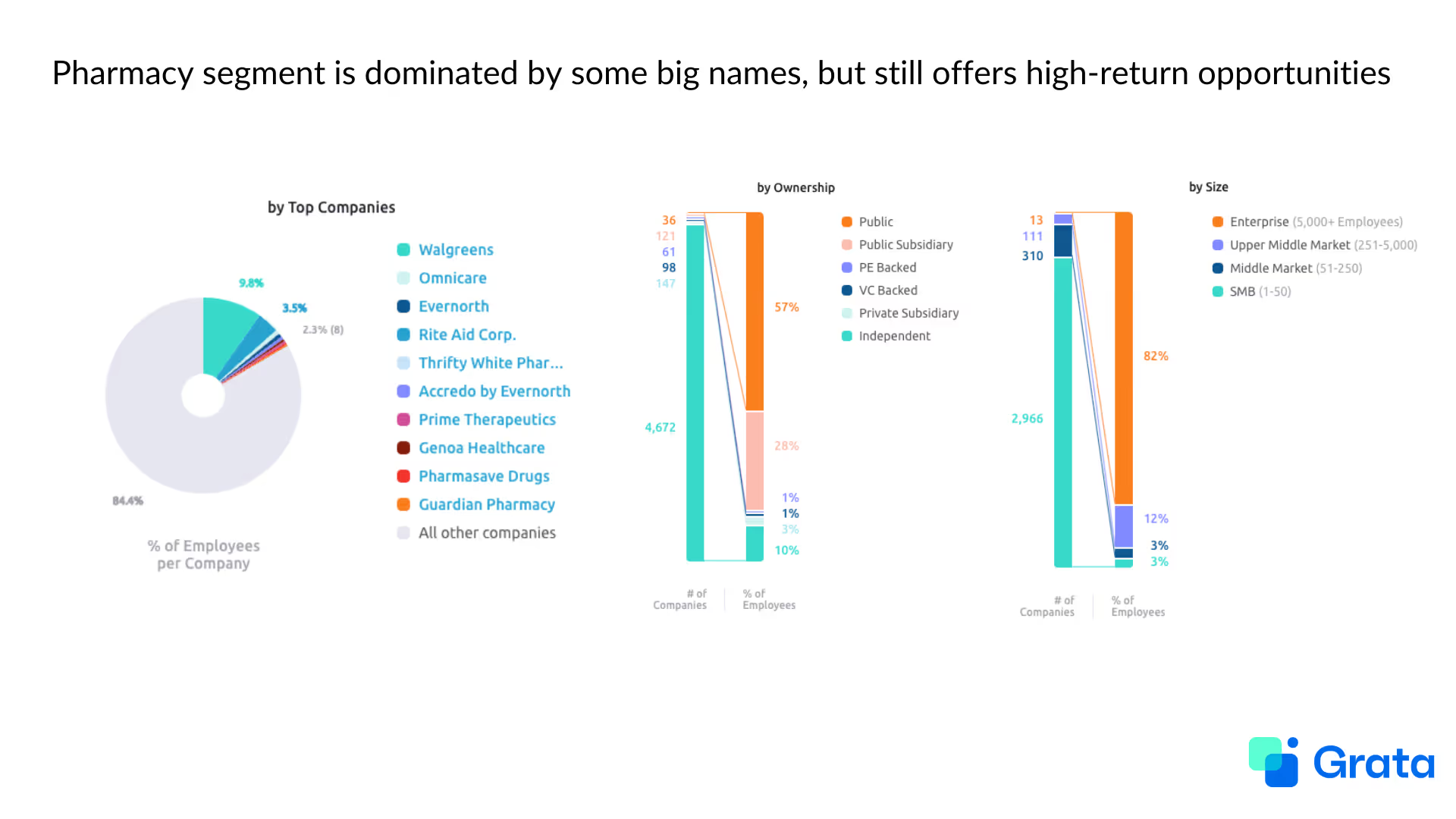

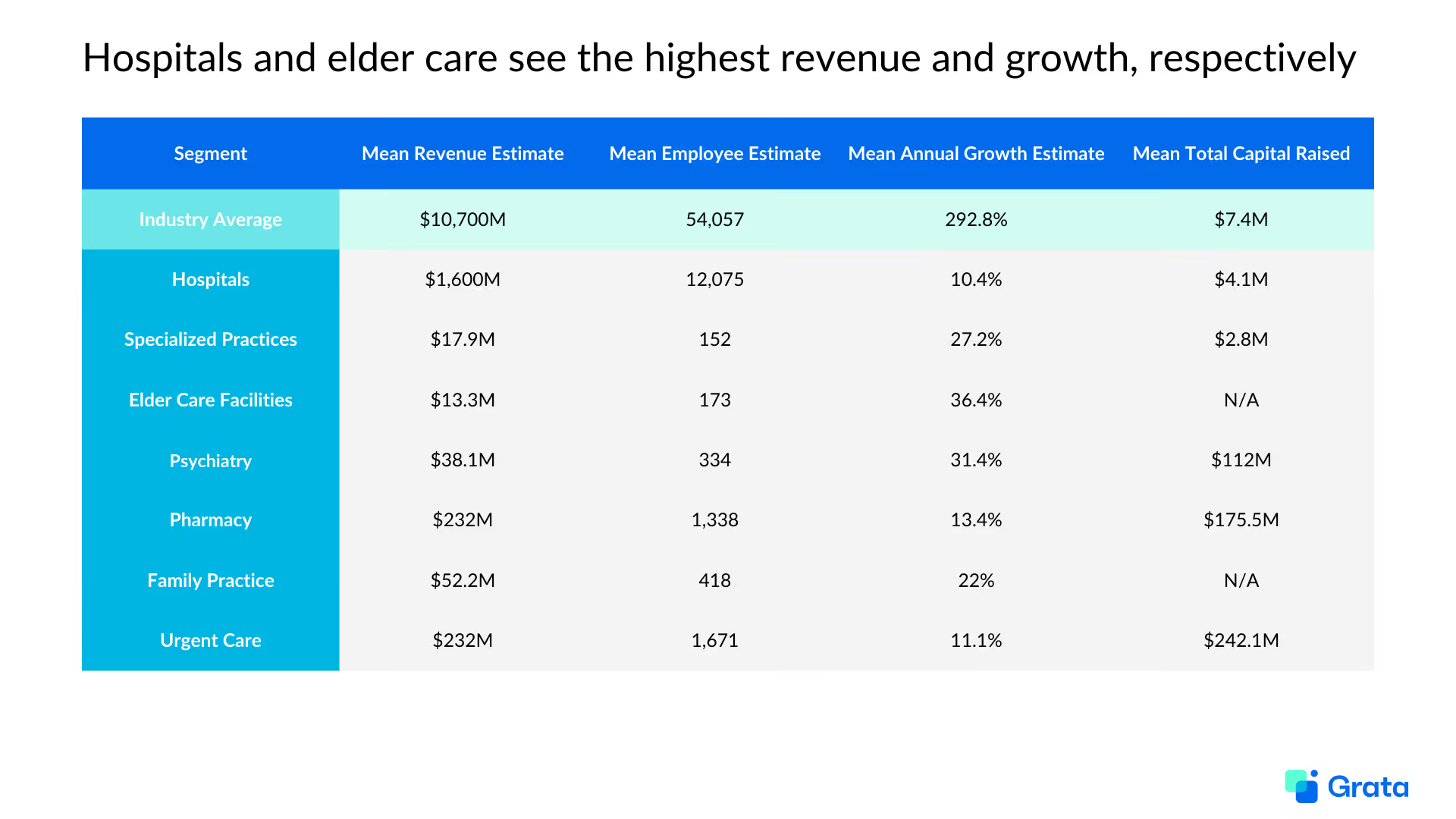

Among the segments analyzed in this report, pharmacy and elder care stand out as high-revenue, high-growth opportunities.

Notably, the pharmacy segment has the lowest percentage of private companies of the markets we analyzed. Private pharmacies and their subsidiaries account for just 13% of industry share, compared to 72% of family practices, 61% of psychiatry practices, etc. The pharmacy space is dominated by major corporations including Walgreens and Rite Aid.

Source: Grata

Still, the space sees the highest revenue and revenue growth of the markets analyzed here, which suggests the relatively few opportunities are worth pursuing.

Meanwhile, the elder care segment, which comprises 46% privately owned facilities, sees the highest average EV/Rev multiple and EBITDA margins of the group. Private equity activity in the elder care space has been steadily increasing over the last several years, particularly in assisted, independent, and dementia care facilities, according to Liberty Mutual. Key factors driving the trend are increased life expectancy and the growing number of Baby Boomers who require additional care.

Another area worth investigating is psychiatry. There are currently nearly 2,500 independently owned psychiatric practices ripe for acquisition, and the space sees the second-highest average growth rate of the segments analyzed here. Demand for mental health services is on the rise, and ongoing developments in telehealth are making the services more accessible. In the US, jobs in the mental healthcare space are expected to increase at 3x the rate of jobs in all other fields over the next 10 years, according to the US Bureau of Labor.

Source: Grata

In the private sphere, hospitals see the most average revenue by far. It’s no wonder, then, that private equity activity firms have been snapping them up — with PE firms owning 8% of private hospitals in the US as of January 2024.

With the impressive financials and nearly 8,500 privately owned facilities in the space, hospitals might seem like a no-brainer for PE investors. However, criticism of PE firms buying hospitals has grown louder over the last few years. Many say that the business model hinders hospitals’ ability to provide quality care. A recent JAMA study showed that hospitals owned by PE firms reported higher rates of patient complications than other facilities. This issue has contributed to more states considering new disclosure laws around PE/healthcare transactions.

Meanwhile, elder care facilities top the list in terms of average annual growth. And with no reported capital raised in the space, and a high percentage of privately owned companies, private equity investors could find an opportunity to establish themselves as leaders here.

Family practices and specialized practices could also offer investors opportunities to establish leadership, as both spaces have little to no funding raised, high percentages of privately owned facilities, and positive growth rates. However, to reiterate, investors must thoroughly research the status of states’ disclosure requirements around PE transactions in healthcare.

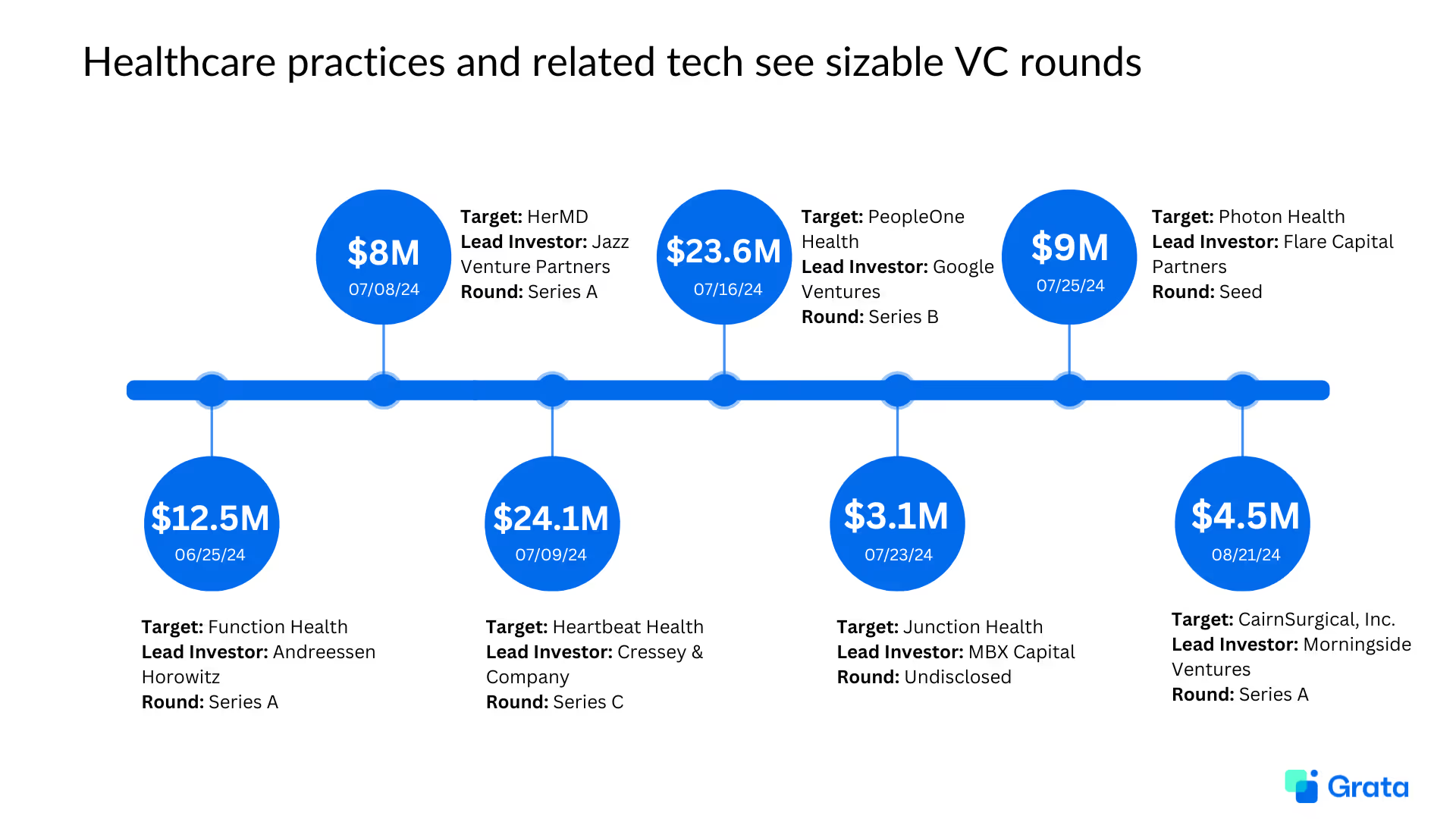

Source: Grata. This graphic does not represent a complete list of VC and growth transactions in the healthcare space in the last two months.

The healthcare industry is constantly innovating and evolving, making it a prime focus area for venture capital (VC) and growth investors. In the last two months alone, healthcare companies across segments and across funding stages have raised tens of millions of dollars from VCs.

Source: Grata

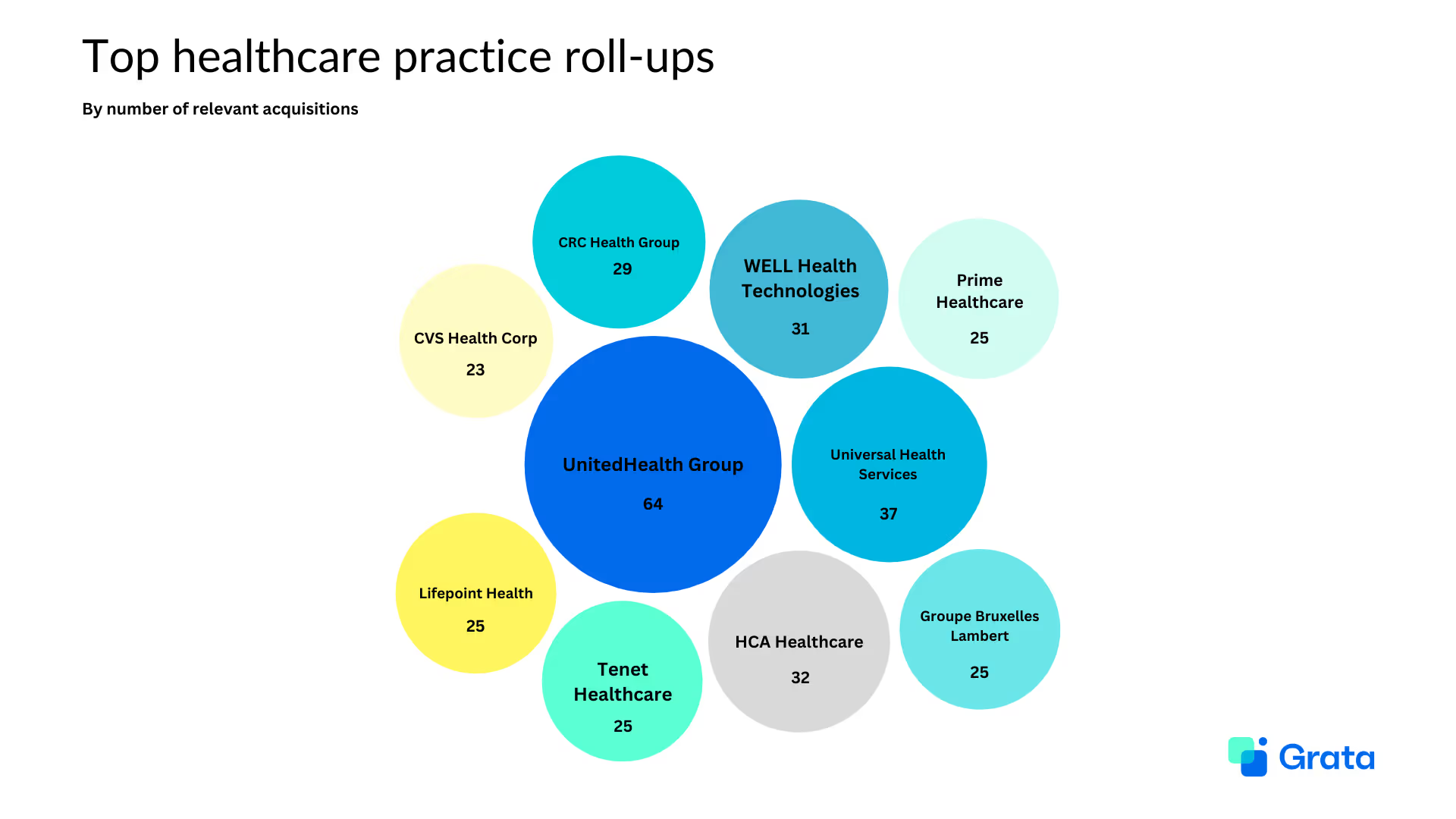

The healthcare space has seen a significant amount of roll-ups over the last several years. Major healthcare companies like UnitedHealth Group, Universal Health Services, HCA Healthcare, and others are buying up facilities including hospitals, clinics, specialized care practices, urgent care centers, and pharmacies.

.avif)

Source: Grata

In March, the clinical enterprise of the University of California, Irvine (UCI), purchased four hospitals and their associated outpatient locations from Tenet Healthcare Corporation. Among the acquired facilities were Los Alamitos Medical Center, Fountain Valley Regional Hospital, Lakewood Regional Medical Center, and Placentia-Linda Hospital.

UC Irvine Chancellor Howard Gillman said the deal would “bridge gaps in regional care and advance the University of California’s mission to serve our communities.”

If you’re an investor interested in companies like Los Alamitos Medical Center, try these:

Orlando Health signed a definitive agreement in August to acquire Tenet Healthcare’s majority share in Alabama-based Brookwood Baptist Health. Brookwood comprises five hospitals in Central Alabama that offer over 1,700 patient beds, 70+ primary and specialty care clinics, and around 1,500 affiliated physicians.

If you’re an investor interested in companies like Brookwood Baptist Health, try these:

Private equity activity in healthcare isn’t just limited to the US. In July, European PE firm Exponent acquired Kingsbridge Healthcare, a Northern Ireland-based healthcare provider, for $383.5M.

Exponent reported that the deal would help scale its operations and bolster its ability to “provide world-class medical services” to patients in Ireland.

If you’re an investor interested in companies like Kingsbridge Healthcare, try these:

Earlier this month, Cardinal Health entered a definitive agreement to purchase Integrated Oncology Network (ION) for $1.1B. ION comprises over 50 practice sites across 10 states.

Cardinal Health CEO Jason Hollar said of the deal, “With their proven model providing extensive support of community oncology across the cancer care continuum and healthcare ecosystem, we're confident Integrated Oncology Network will further accelerate our oncology strategy and enable us to create value for providers and patients."

If you’re an investor interested in companies like Oncology Network, try these:

Medication management tech company Scriptology acquired its direct competitor RxLive earlier in September. Executives said the deal would help Scriptology build out its tech stack, particularly through RxLive’s AI-based risk stratification system, which reportedly predicts when involving clinical pharmacists in patient care will have the greatest impact.

If you’re an investor interested in companies like RxLive, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the healthcare practices industry:

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

If you’re an investor interested in healthcare practices, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

Schedule a demo today to get started.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)