.webp)

The Private Market Data Buyer’s Guide

Private market data helps investors make informed decisions in capital markets - here’s how to evaluate and choose the right data provider.

.webp)

If you’re a college student or a recent graduate interested in breaking into the M&A world, figuring out where to start can be daunting.

In this guide, the Grata team breaks down everything that aspiring M&A professionals need to know about how to break into the industry and how to succeed.

From how the dealmaking process works to acing the job interview to the fundamentals that every analyst must master, this is your go-to source for kickstarting your career and navigating the M&A world.

Middle market: The middle market refers to companies that are larger than small businesses but smaller than large corporations — typically with revenues between $10M and $1B. This is where most private equity and M&A activity happens.

Venture Capital (VC): Venture capital firms invest in early-stage companies with high growth potential, often in tech or innovation-driven sectors. They take equity stakes in exchange for funding and guidance.

Growth equity: Growth equity investors back more mature companies that are already generating revenue but need capital to expand — think new markets, product lines, or acquisitions.

Private equity: Private equity firms invest in established companies, often taking controlling stakes to improve operations, drive growth, and eventually sell the business for a profit.

Business Development (BD): BD teams focus on sourcing investment opportunities — building relationships, finding potential deals, and ensuring a steady pipeline through disciplined relationship development.

Investing: In this context, investing means deploying capital into private companies with the goal of creating long-term value and generating returns for the firm’s investors.

Portfolio operations: Once a firm invests in a company, the portfolio operations team helps improve its performance — from strategy and sales to finance and efficiency — to increase its eventual value.

Public comps: Public comparables are publicly traded companies similar to a target business. Analysts use their financial metrics to estimate what a private company might be worth.

Precedent transactions: These are past M&A deals involving similar companies. Studying them helps investors understand what others have paid and what valuations might be realistic.

Market Sizing: Market sizing estimates the total potential revenue or customer base in a given market — crucial for judging whether a business can scale meaningfully.

Unit economic growth: This measures how profitable a company is at the level of a single product or customer — key for understanding if growth will actually translate into sustainable profits.

LBO (Leveraged Buyout): An LBO is when a private equity firm buys a company primarily using borrowed money (sourced from banks and private credit funds), then works to grow cash flow and pay down debt to earn a return.

Buy-and-build: A strategy where a firm acquires a strong platform company, then adds smaller “bolt-on” acquisitions to expand market share or capabilities.

Deal Sourcing: The process of finding potential investment opportunities through networks, databases, advisors, or inbound leads.

Deal Screening: This is the early-stage evaluation of opportunities to determine if they fit the firm’s investment criteria — before investing time and resources into deeper analysis.

Due Diligence: A deep-dive investigation into a target company’s financials, operations, market position, and risks to validate its true value before closing a deal.

Analyst: Entry-level professionals who handle research, financial modeling, and initial screening to support deal teams.

Associate: Associates dig deeper into deals, managing analyses, coordinating due diligence, and supporting negotiations.

Vice President (VP): VPs lead deal execution — managing associates, interfacing with company executives, and steering transactions through to completion.

Principal: Principals are senior investors responsible for sourcing deals, leading negotiations, and managing relationships — often on track to become partners.

Partner: Partners are firm leaders who drive investment strategy, oversee portfolios, and make final decisions on deals.

Managing Director (MD): The most senior role, often synonymous with Partner in many firms. MDs set direction, lead fundraising, and represent the firm at the highest levels.

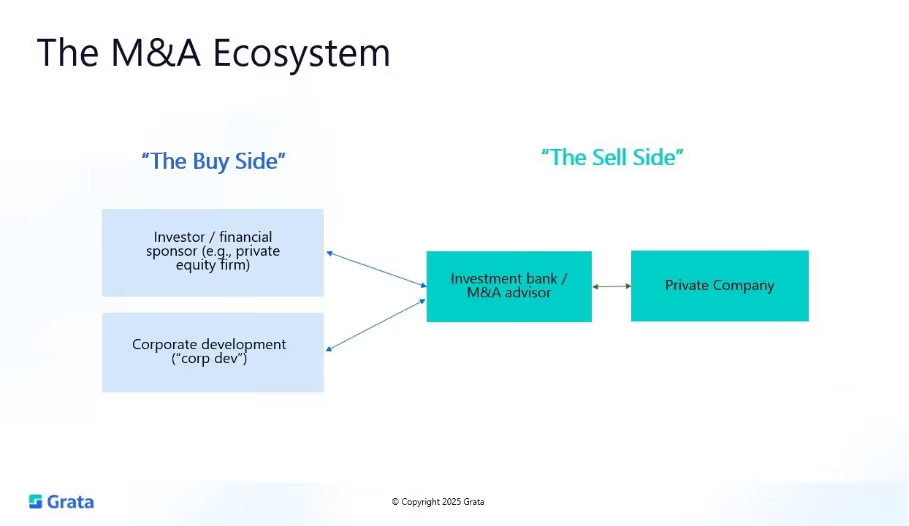

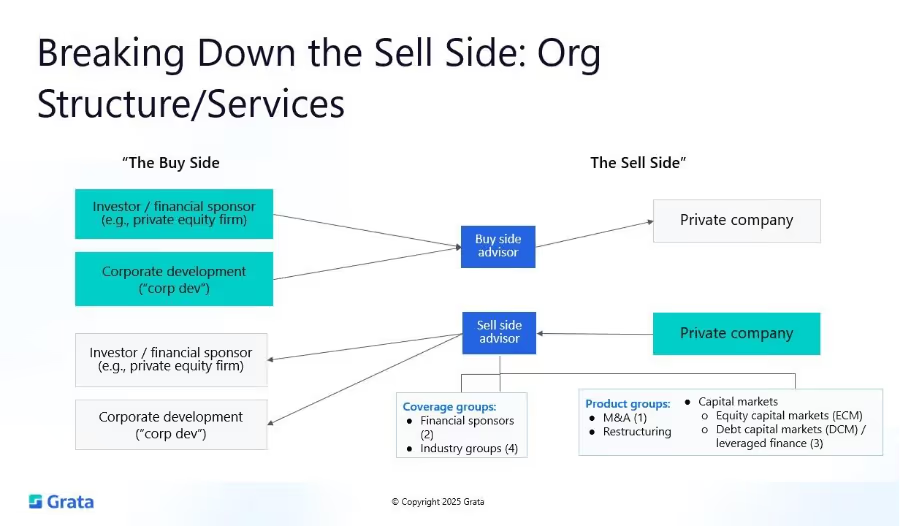

So how does the M&A process work? Let's start by understanding the two different sides of this picture.

The buy side refers to anyone who is buying a company. That can be two different groups of firms:

Maybe you want to acquire a new technology or enter a new market or get some talent OR break into a new product line you've never provided before. That's what corp dev does.

The sell side, on the other hand, refers to the private company that’s up for sale. Executives from the selling company typically work with an investment bank or an M&A advisor to help broker the deal with a buyer.

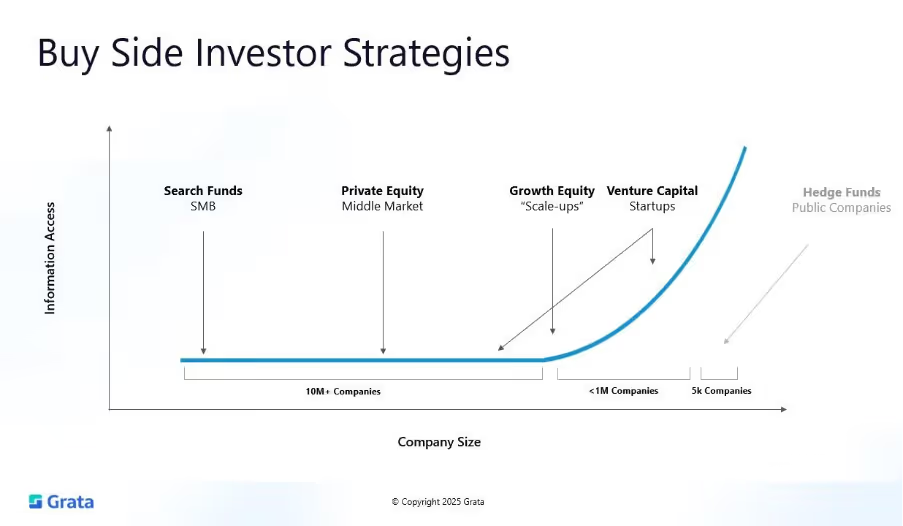

Each buy-side firm has its own investment strategy, risk tolerance, and time frame.

The graph below illustrates company size (x-axis) and how much information that investors can uncover in due diligence (y-axis).

Search funds are small (think: as few as one person) private equity firms focused on acquiring a single small to medium-sized business.

PE firms buy controlling stakes in established bootstrapped, middle-market companies. Often, their goal is to improve the target company’s performance and sell it for a profit within a few years.

VCs invest in early-stage startups with high growth potential. They take minority stakes and provide funding to help these young companies scale. Some also provide

Think of growth equity as a hybrid of PE and VC. These firms focus on more mature businesses, known as “scale-ups,” that are expanding and need funding to support that growth.

Hedge funds and asset managers typically focus on public markets. Note that some hedge funds also participate in M&A transactions by buying stakes in public companies to influence strategic moves like spin-offs or sales.

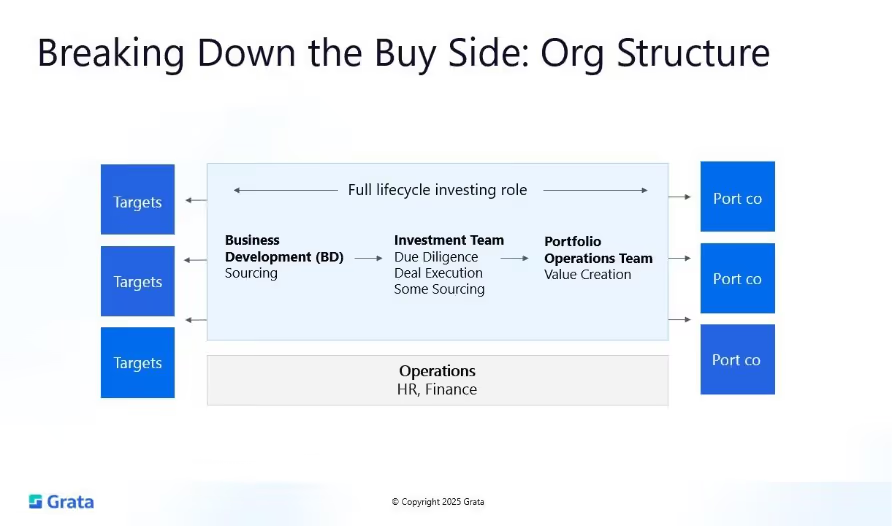

While these firms invest in different parts of the company life cycle, they share a significant amount of overlap in terms of structure.

Most roles for M&A professionals with 0-4 years of experience sit within the business development or investment teams:

Larger funds also have a portfolio operations team, which is responsible for value creation. Think of this team as consultants who help port cos become better companies.

Firms also have Operations teams, which include HR and Finance functions, to take care of logistical and operational support.

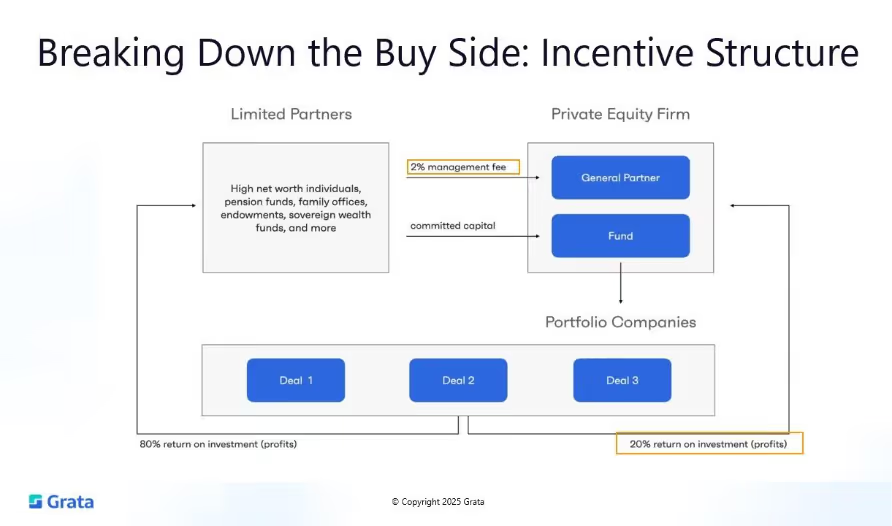

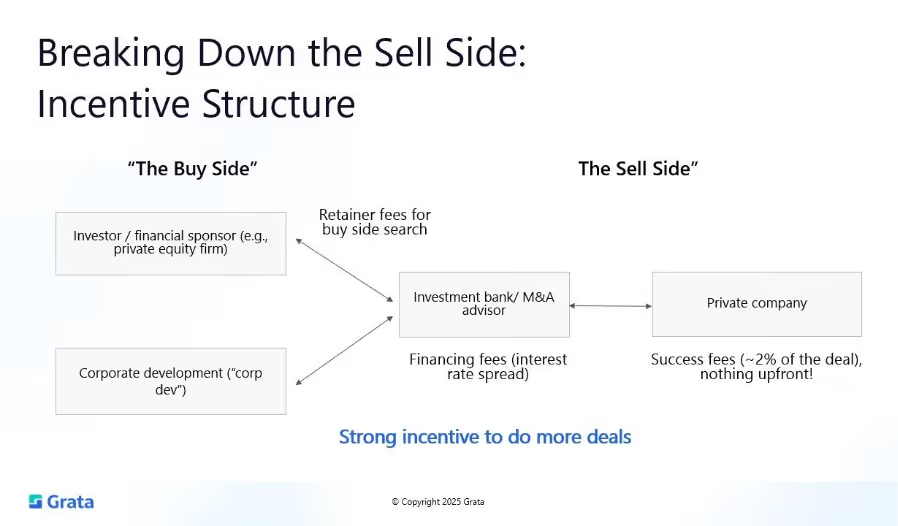

So how do these firms actually make money? Here’s how the key players work together.

Limited partners (LPs) are the investors who provide the capital for a PE fund. LPs can include high net worth individuals, pension funds, family offices, endowments, or sovereign wealth funds. Their goal is to earn high returns over the life of the fund.

General partners (GPs) manage the PE fund and use the LPs’ capital to acquire companies. They charge management fees — usually around 2% of assets under management — to cover operating costs, employee salaries, etc.

The businesses that a PE firm acquires are known as portfolio companies, or port cos. The PE firm’s goal is to make the port cos more valuable and ultimately generate returns. The returns are split: 80% goes to the LPs while GPs retain 20% of the profit, which is known as “carry” or “carried interest.” Many PE firms earn the bulk of their income on carried interest, which is directly tied to performance. This structure ensures that the PE firm’s goals and successes are directly aligned with those of their investors.

When executed correctly, this system generates wins for everyone involved:

Now let’s dig into the sell side. Firms operating on this side of the equation help companies raise capital, prepare for acquisitions, and navigate the process of selling their business.

Most investment banks and advisory firms break their teams into coverage groups and product groups:

On the sell side, incentives revolve around deal flow and transaction success. Unlike the buy side, where returns are earned over years, sell-side rewards are tied to completing deals efficiently and profitably.

Investment banks and advisory firms earn fees for completed transactions. These are often a percentage of the deal’s value, known as a success fee.

Firms may also charge retainer fees for ongoing advisory work. The more deals a firm closes — and the bigger those deals are — the higher the firm’s revenue.

The best way to lay the foundation for a career in M&A is to land an internship in the industry and learn as much as you possibly can. Then, when you go to interview for analyst or associate roles, you’ll have a strong knowledge base to pull from.

Here are some tips for getting the most out of your internship and bringing that knowledge into your interviews later on.

Excelling at your internship isn’t just about learning to build financial models. Don’t get us wrong — financial models are certainly part of it. But succeeding at your internship requires a holistic approach.

Here are the six most important things that the majority of interns overlook:

Now, how do you actually land the analyst job? There are two components to each interview: technical and behavioral.

The technical portion assesses your understanding of the financial fundamentals that underpin the job. Because it's essentially a “check the box” exercise, it’s difficult to differentiate yourself in this portion — but you have to get it right to move forward.

You need to demonstrate that you can think like an analyst. That means demonstrating a strong understanding of:

Pro Tip: Don’t just memorize these concepts — make the effort to really understand them. That way, you’ll be able to explain them in your own words. Clarity is just as important as technical prowess.

Your opportunity to stand out from other candidates comes in the behavioral portion of the interview. Here’s how to do that.

So let’s say you’ve landed the job. Congratulations! Now the real work begins. The role of the analyst is centered around analyzing data and thinking strategically about where deals come from and why they work.

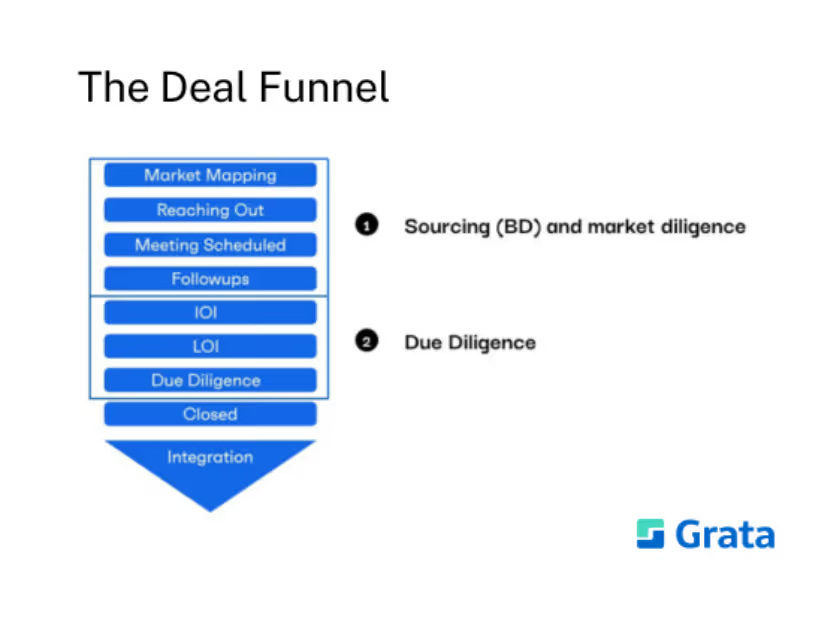

As an analyst, you need to have a deep understanding of the deal funnel. This is how an idea becomes an actual closed transaction.

First, firms conduct market mapping. This is where they assess how many and what kinds of companies fit the firm’s investment thesis and compile a list of potential targets. Members of the BD team reach out to executives at those companies to schedule meetings to kick things off.

After any necessary follow-ups, the firm submits an indication of interest (IOI). This is a formal notice that the firm is interested in acquiring the company. Next comes the letter of intent (LOI), which outlines the terms of the offer, including a valuation range.

Then the due diligence process begins. This is where the team dives deep into the target company’s financials, operations, strategy, competitive standing, growth potential, legal and regulatory compliance — everything. Once everything is aligned, the deal can close and integration can begin.

Additional Reading:

Analysts support the deal sourcing process in several key ways:

The best analysts don't just crunch numbers. They understand why a company might be an attractive target, what risks it presents, and how it fits into the firm’s overall strategy.

Thematic sourcing starts with an idea rather than a target list. Deal teams look for patterns in market behavior, such as emerging technologies, regulatory changes, or evolving consumer habits, and analyze what industries or business models will benefit from the shifts.

Once a theme is identified, analysts map the ecosystem, identifying the companies driving or benefiting from the trend. For example, if your team believes that the outsourced healthcare services sector is poised for consolidation, you would research specialized clinics, diagnostic providers, and staffing platforms to find acquisition targets.

BD analysts have to write a lot of cold emails. Here’s what you’ll need to compose emails to executives that not only get opened, but get responses:

Avoid these common mistakes that BD analysts make:

Additional Reading

Analysts also play a key role in the diligence process:

The diligence phase also includes a heavy amount of financial modeling. Here are the most common model types you need to know as an analyst:

One of the most important skills for an M&A analyst is knowing how to value private companies. This process begins with analyzing companies that are comparable to your firm’s target, aka “comps.” Comps help deal teams determine what a company might be worth based on how similar businesses are performing.

Here are the different kinds of comps analysis you need to know.

M&A Comps (aka Precedent Transactions)

M&A comps, or precedent transactions, look at past deals involving similar companies to estimate what a business might sell for today. These are especially important for the sell side, as they help set expectations for valuation.

For this kind of analysis, analysts focus on:

Public Comps

Public comps analysis compares the target company to a set of publicly traded firms in the same industry. This helps the deal team understand how similar businesses are valued in the current market.

For public comps analysis, analysts gather data from financial statements, investor presentations, and stock market metrics such as:

Private comps

Private comps analysis uses valuation multiples from similar companies in the private market. These can be sourced from holistic dealmaking platforms like Grata, industry reports, or firm deal history.

Private comps are especially useful for evaluating mid-market and lower-middle-market deals, where private companies dominate. Analysts use them to fill the gap between precedent transactions and public comps, ensuring valuations are realistic for the target industry.

Market fragmentation

Analysts conduct market fragmentation analysis to understand the competitive landscape and structure of the target industry. They assess market opportunity using:

A fragmented market is one in which many small players compete. Fragmented spaces often present attractive M&A opportunities, especially for buy-side firms pursuing roll-up strategies.

Other key technical skills that analysts should master include:

Additional Reading:

The analyst role sets the foundation for advancement in M&A. Understanding the typical path will help you prioritize learning and career development opportunities.

Analysts who show initiative, strong analytical skills, and business judgment are often given early exposure to client meetings, deal strategy sessions, and more — all of which can help accelerate their path to associate and beyond.

Additional Reading

If you’re an undergraduate interested in pursuing a career in M&A, the Grata Scholars program can give you a serious edge.

The five-week program takes place twice a year, once in the fall and once in the spring. Over the course of each semester, Grata Scholars boost their resumes with industry-specific skills and knowledge. This includes learning to navigate the Grata platform like a pro. Scholars also compete for an opportunity to work with a private equity firm, investment bank, or corporate development team focused on M&A.

Learn more about the program and submit your application here.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)