AI & Automation

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

.webp)

The data center industry is exploding. As of 2023, the space was valued at $219.2B, and it’s expected to grow to $585B by 2032.

Driving the trend is rising demand for data and cloud computing as more industries adopt AI, machine learning, and IoT technologies.

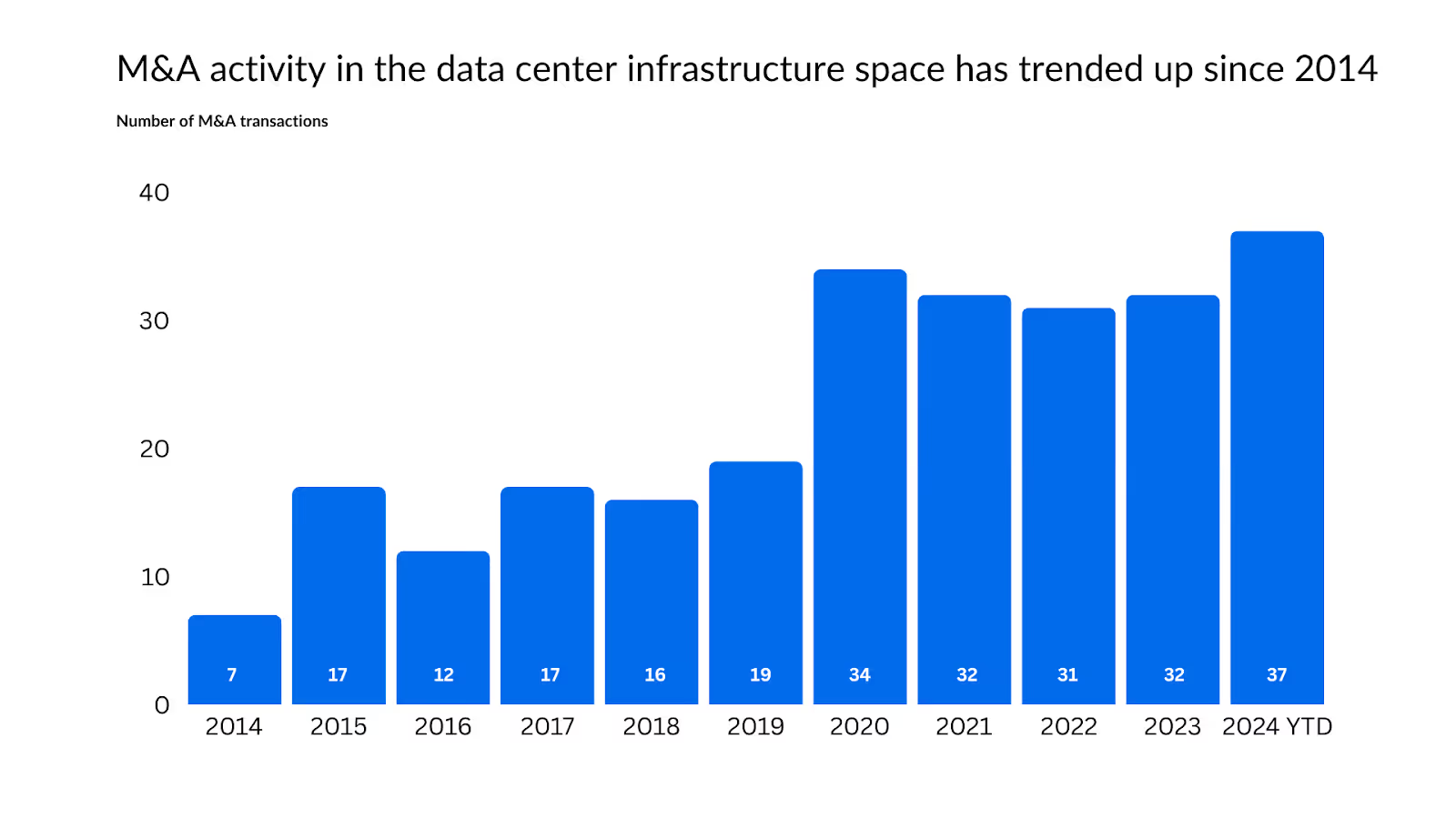

Private equity (PE) investors are getting in on the action. They’re buying up companies that provide critical services to data centers, including tech support, power, cooling, cleaning, and network equipment. M&A activity in the data center infrastructure industry has more than tripled over the last decade, as the graph below shows.

Source: Grata

The data center tech industry shows no signs of slowing down, offering a wealth of opportunities for PE investors.

In this PE Playbook, the Grata team has put together the need-to-know trends for dealmakers considering making moves in the data center infrastructure market, including:

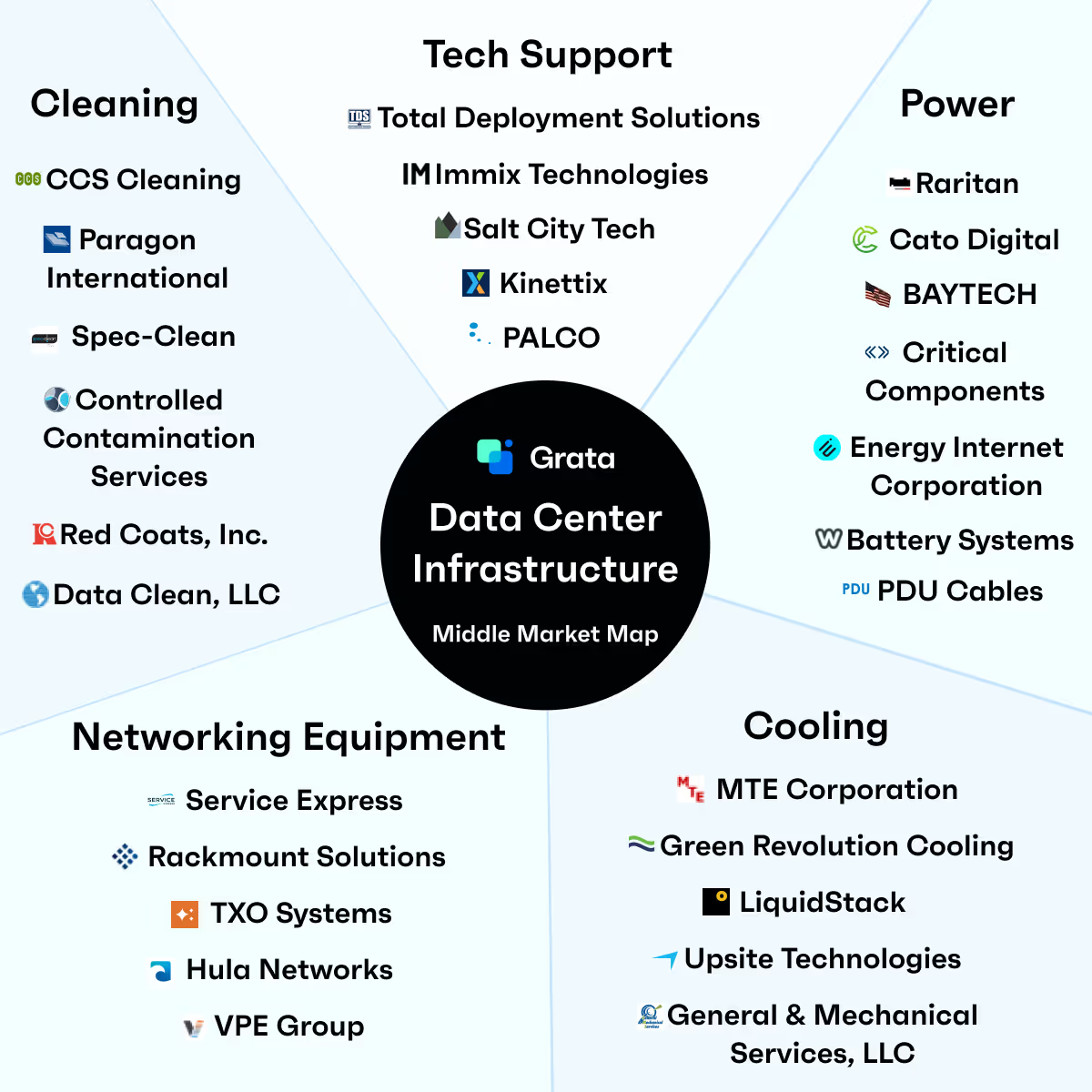

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Source: Grata

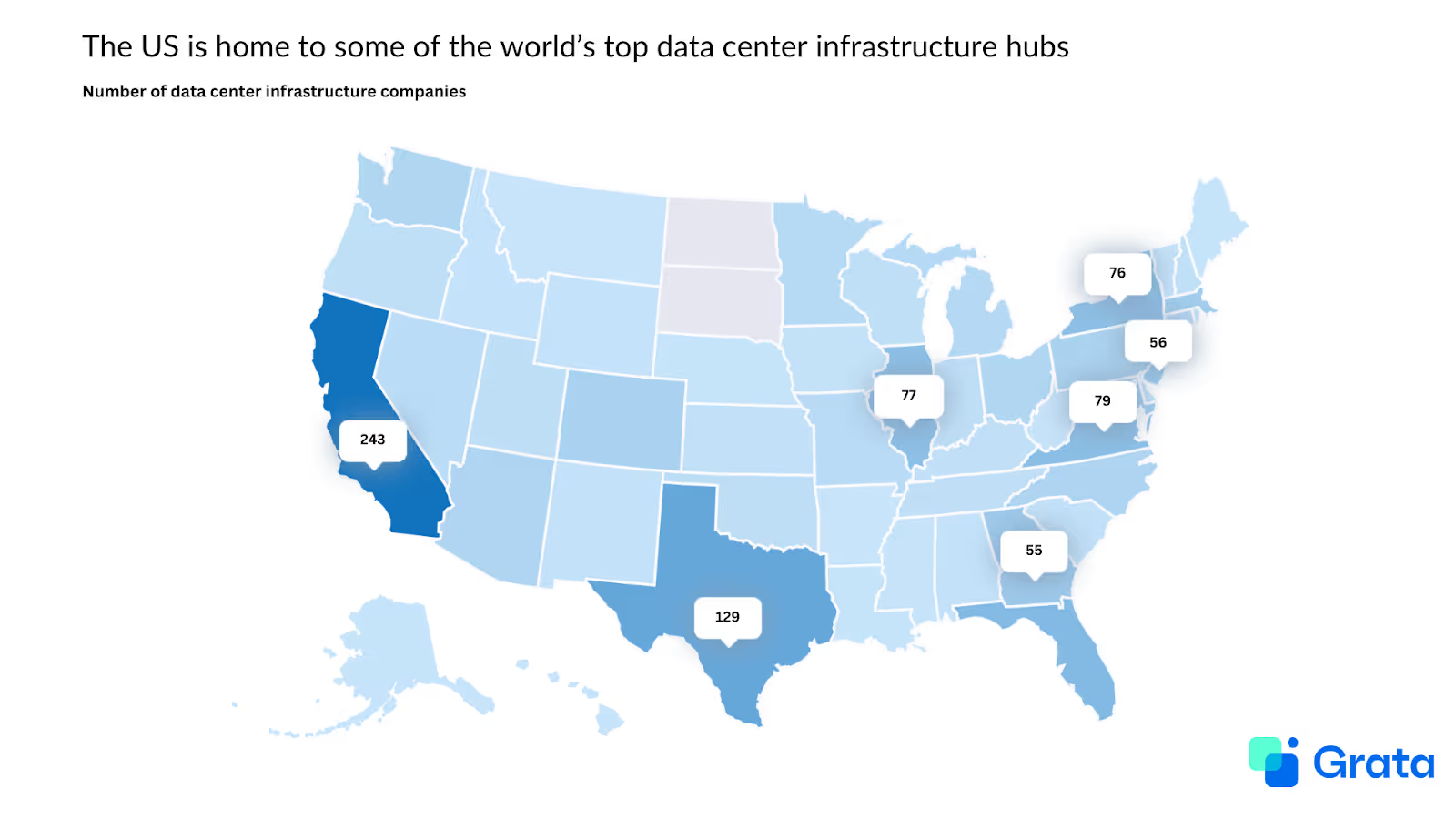

The data center infrastructure market is widespread across the US, with companies in the space headquartered in all but two states.

While California and Texas are home to hundreds of data center infrastructure companies, Virginia has emerged as the real powerhouse in the industry. The state is often referred to as the “data center capital of the world.” It has a dense concentration of data centers due to the state’s favorable business climate, reliable power sources, access to fiber optic networks, and skilled workforce.

Source: Grata

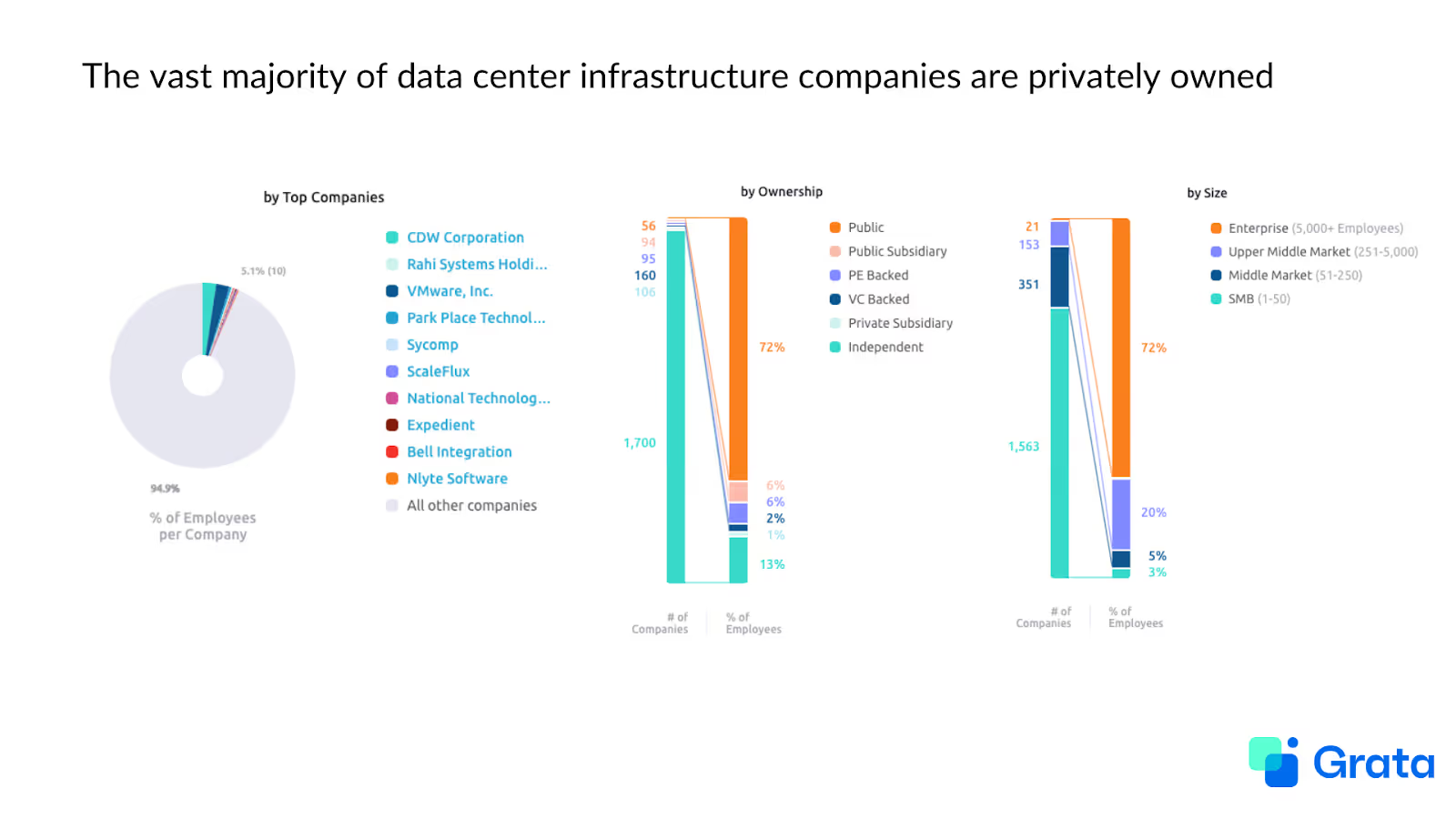

While a handful of public companies control 79% of the data center infrastructure industry, private companies comprise the overwhelming majority.

Grata data shows that there are currently just under 1,700 independently owned data center infrastructure companies that are ripe for acquisition.

Source: Grata

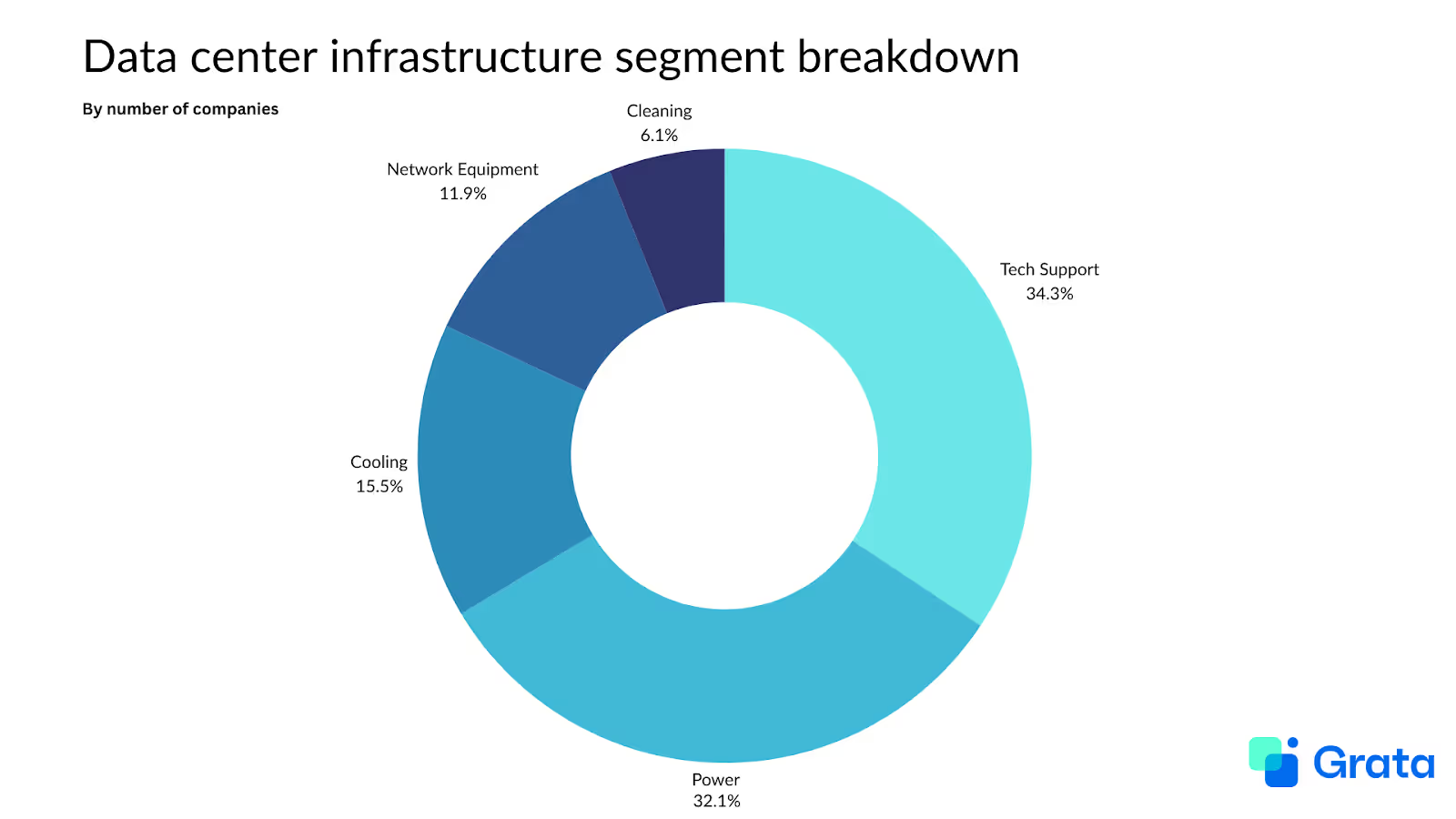

This report focuses on the following segments of the data center infrastructure industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

Source: Grata

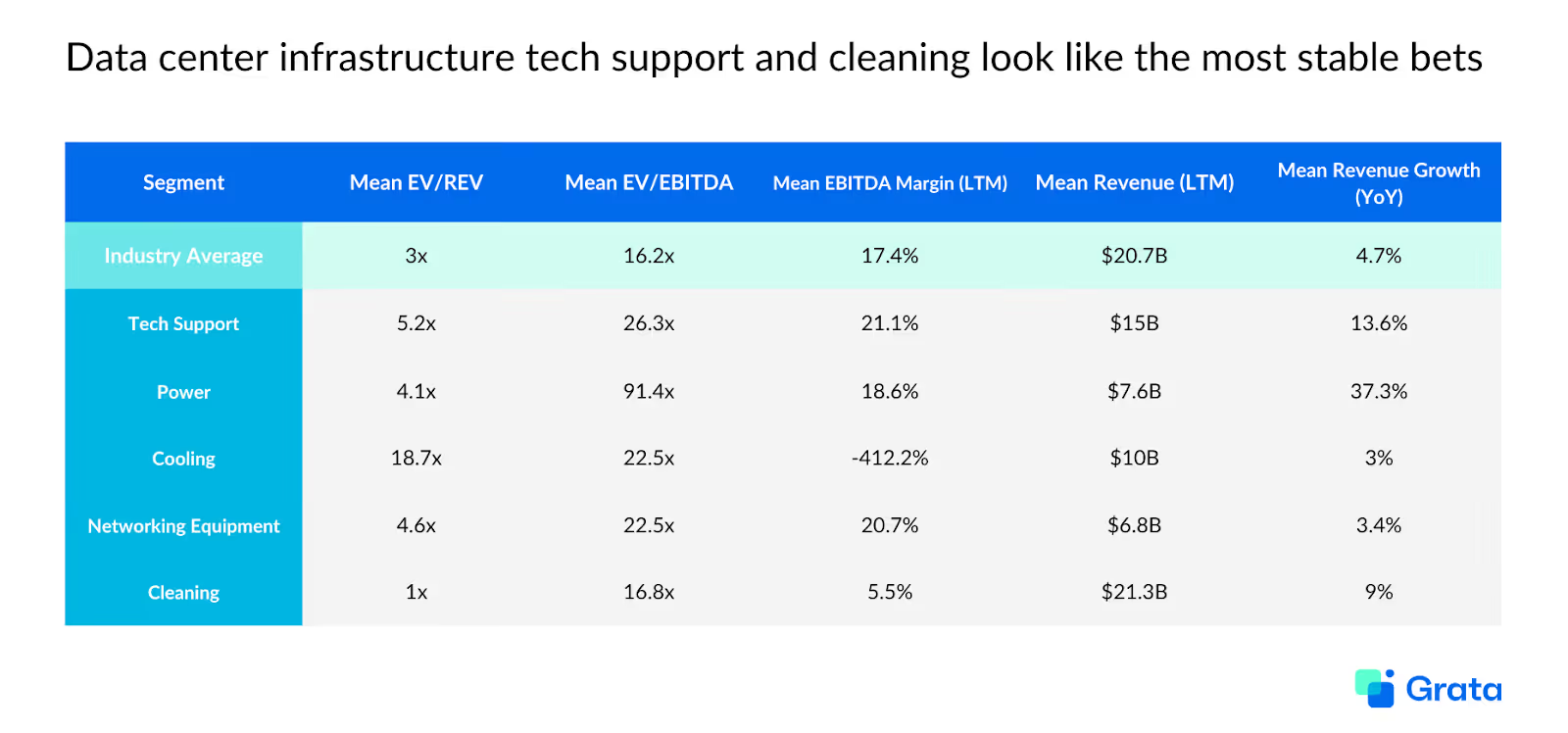

For dealmakers interested in the data center infrastructure space, tech support and cleaning should be the first segments on your list. These sectors bring in the most annual revenue on average, and their growth rates considerably outpace the industry average. Many companies offering tech support also provide other data center support services, including power.

The data center power sector also offers strong opportunities for investors. The space has the highest average growth rate by far, and EBITDA multiples that exceed the industry averages. Note, however, that the average revenue tends to be among the lowest of the sectors analyzed in this report.

One of the biggest sources of data center power consumption is cooling. The tech is crucial to keep the equipment from overheating and avoid detrimental downtime. But the cooling systems gobble up between 30%-55% of data center power, driving up operating costs. As a result, the sector’s average EBITDA margins are deep in the red. Still, dealmakers interested in data center infrastructure should keep an eye on the space — operational costs will likely decrease over time as cooling systems become more energy-efficient.

Source: Grata

In the private sphere, networking equipment companies see the most average revenue by far. The space has also far outpaced the other sectors in terms of capital raised, with an average of $1.5B. While this clearly signals strong opportunity for dealmakers, competition in networking equipment is likely much higher than the other sectors.

Meanwhile, the tech support space sees the highest mean growth rate of the markets analyzed here, and it has raised no capital thus far. Dealmakers could have a stronger opportunity to establish themselves as leaders here, as well as in the cleaning sector.

.avif)

Source: Grata

Cloudpoint Technology Berhad acquired a 75% stake in Unique Central in February. Unique Central provides data center infrastructure services including design, construction, integration, monitoring, and sustainability evaluation.

“This strategic move positions Cloudpoint as a comprehensive and end-to-end solutions provider for data center and cloud needs, allowing its existing and potential customers to source, build, and manage their infrastructure from a single provider,” a spokesperson from Cloudpoint said.

If you’re an investor interested in companies similar to Unique Central, try these:

In June, Freshworks announced that it had completed its acquisition of Device42, which offers full-stack IT discovery and dependency mapping services. Freshworks reported that, as a result of the acquisition, its customers would have access to “a unified platform that delivers enhanced ITSM (IT Service Management) and ITAM (IT Asset Management Software) capabilities including advanced asset discovery and application dependency mapping, enabling them to anticipate risks better and resolve incidents faster.”

If you’re an investor interested in companies similar to Device42, try these:

ABM Industries purchased Quality Uptime Services, a data center power services provider, for $119M in June. Following the move, Quality Uptime Services’ employees joined ABM’s Mission Critical Solutions group within the company’s Technical Solutions segment. ABM plans to use the deal to enhance its services and reach new customers.

If you’re an investor interested in companies similar to Quality Uptime Services, try these:

Schneider Electric SE, a global energy management and automation company, announced in October that it had entered an agreement to acquire a controlling share of Motivair Corporation. Motivair provides liquid cooling and advanced thermal management solutions for data centers.

The deal bolsters Schneider Electric’s liquid cooling and high-capacity thermal solutions offerings.

If you’re an investor interested in companies similar to Motivair Corporation, try these:

Last month, global manufacturing and supply chain solutions company announced its intent to acquire Crown Technical Services for $325M. Crown Technical Services provides power distribution and control services to data centers, utilities, and power generation companies.

Norm Siddiqui, president of Crown Technical Systems, said, “this deal brings together complementary products and teams, marking a superb outcome for Crown's employees and customers."

If you’re an investor interested in companies similar to Crown Technical Services, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. If you’re interested in sourcing live deals in the data center infrastructure space, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

If you’re an investor interested in making moves in the data center infrastructure space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

Schedule a demo today to get started.

Monthly tactics from Grata’s team and operators.

From market trends to career advice, Grata’s content fuels smarter decisions.

.webp)

.webp)