The global cannabis industry is currently worth some $70B. That number is expected to reach a heady $216.8B by 2033.

Still, there's a significant amount of uncertainty baked into the cannabis space. H1’25 was a financial mixed bag for the industry at large, with many players posting net losses even as revenue grew. This is a result of the industry still trying to find its footing amid regulatory changes and inconsistencies across countries and states.

But that doesn’t have to be a total buzzkill for dealmakers. There are still opportunities to be found across the cultivation, processing & manufacturing, distribution & logistics, retail, and payments tech sectors.

In this PE Playbook, the Grata team has put together the need-to-know trends for investors considering making moves in the cannabis infrastructure market, including:

The geographic markets where dealmakers can find the most opportunities

Which sectors are seeing the most growth

Recent acquisitions in the industry

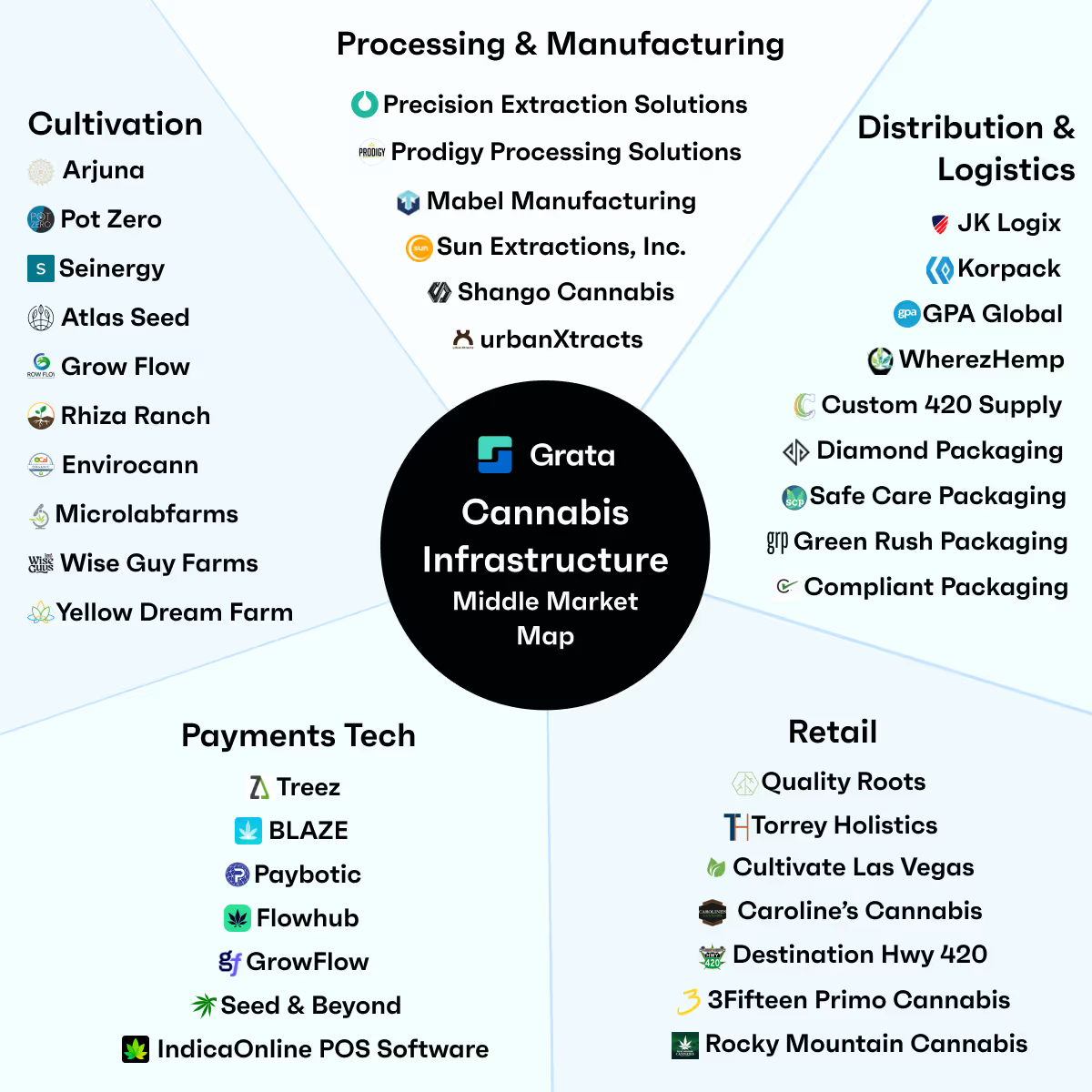

The market map above is not intended to be an exhaustive representation of companies in the space.

Companies that provide services that fall into multiple segments are categorized in this report by their primary offering.

Key Insights into the Cannabis Infrastructure Industry

The US, Australia, and Canada lead the global cannabis infrastructure industry.

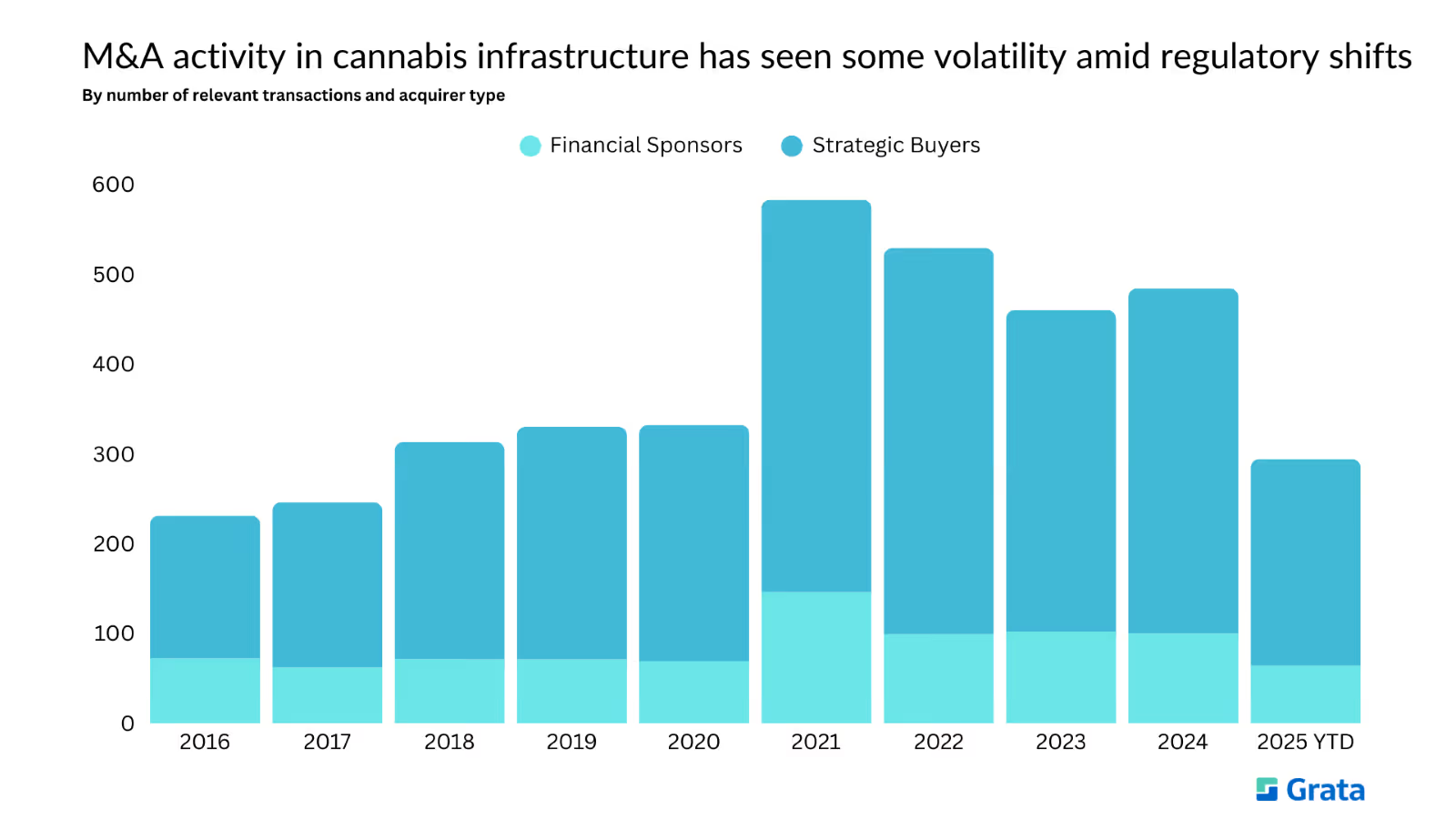

M&A activity in the space has generally trended up over the last decade, though it has experienced a fair amount of volatility amid regulatory changes.

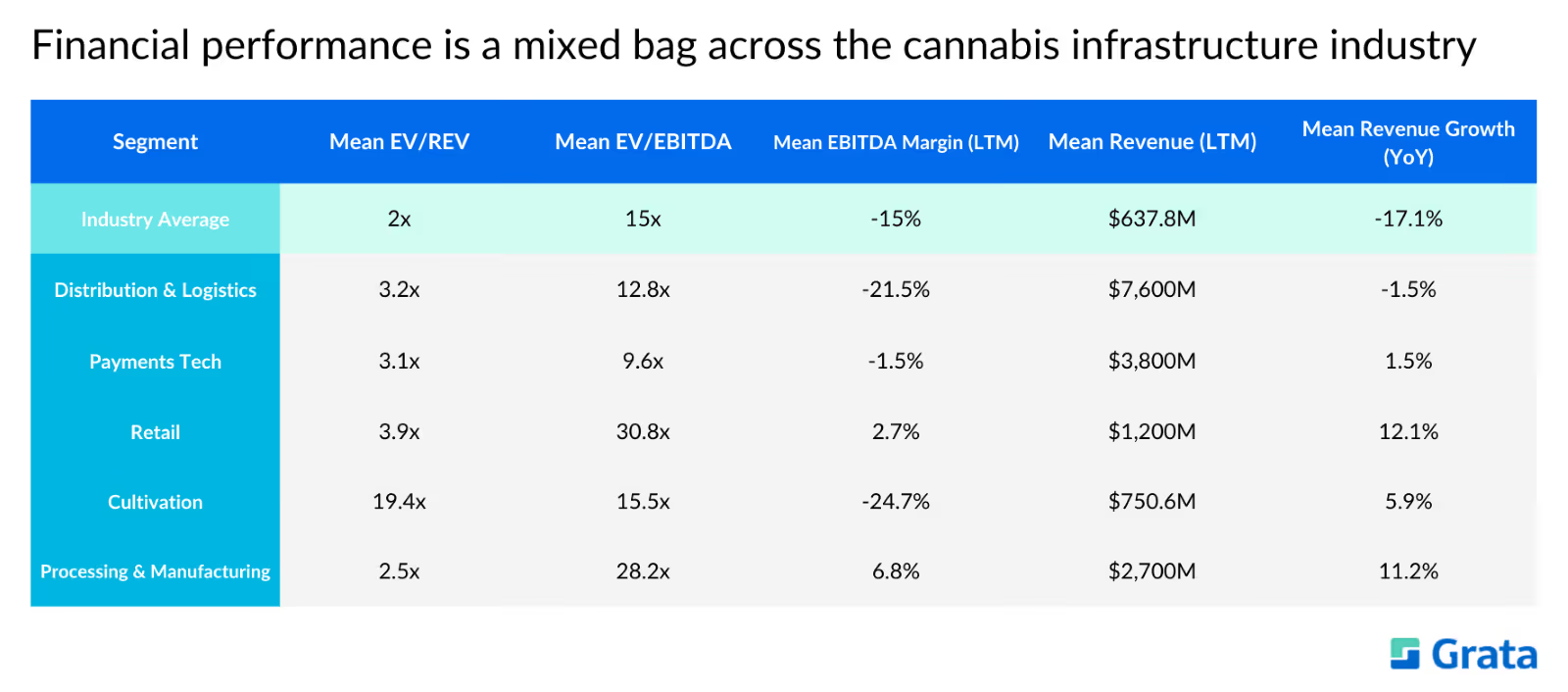

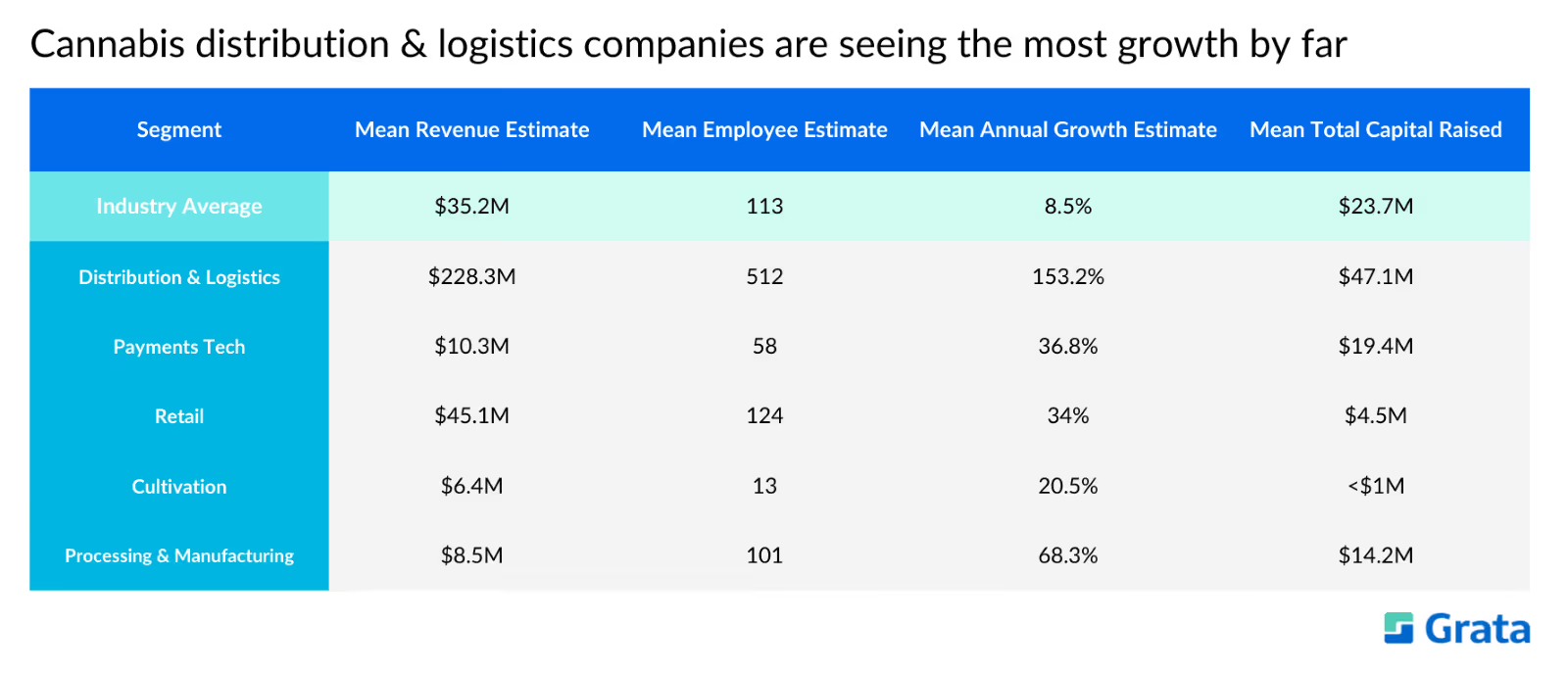

The cannabis infrastructure space could be a gold mine for private equity firms looking for distressed assets. The vast majority of companies in the cannabis industry are not consistently profitable at this point. However, private companies across the cultivation, processing & manufacturing, retail, and payments tech sectors are each seeing double-digit average annual growth.

The cannabis distribution & logistics sector is expanding, with the space seeing an impressive 153.2% average growth rate. Now consolidation in the market is ramping up, enabling new cannabis distributors of various sizes and across multiple states.

Dealmakers willing to take on a little risk and complexity could find opportunities to establish themselves as leaders in the cannabis cultivation space. The cultivation market is the second smallest in the cannabis infrastructure industry, and it raised very little funding.

M&A Trends in the Cannabis Infrastructure Industry

Transactions

Source: Grata

M&A activity in the cannabis infrastructure space has fluctuated, though generally trended up, in the last 10 years.

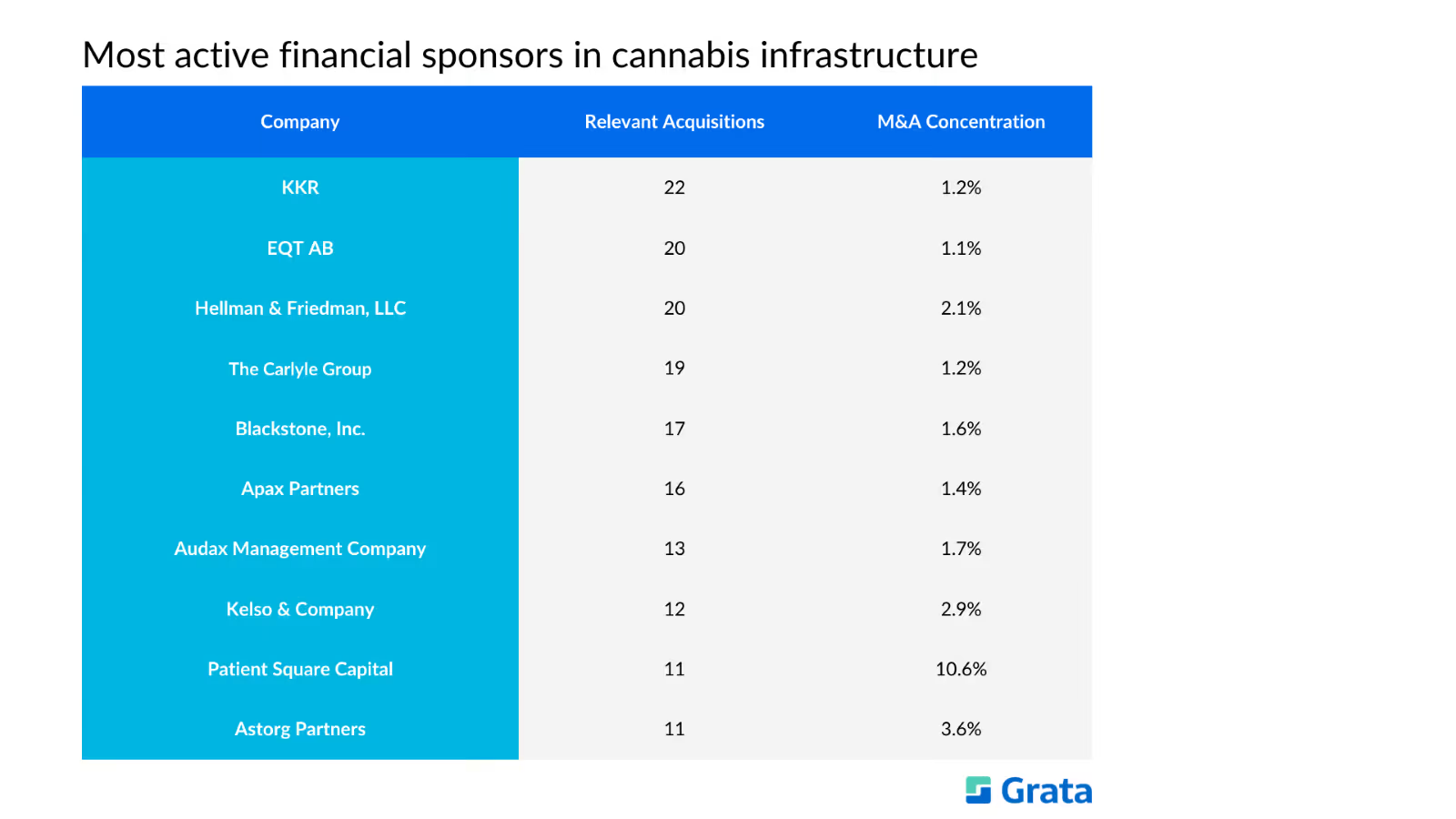

Most Active Financial Sponsors

Source: Grata

KKR tops the list of most active financial sponsors in the cannabis infrastructure industry with 22 relevant deals. Many of its acquisitions in the space deal with solutions and services related to medical cannabis.

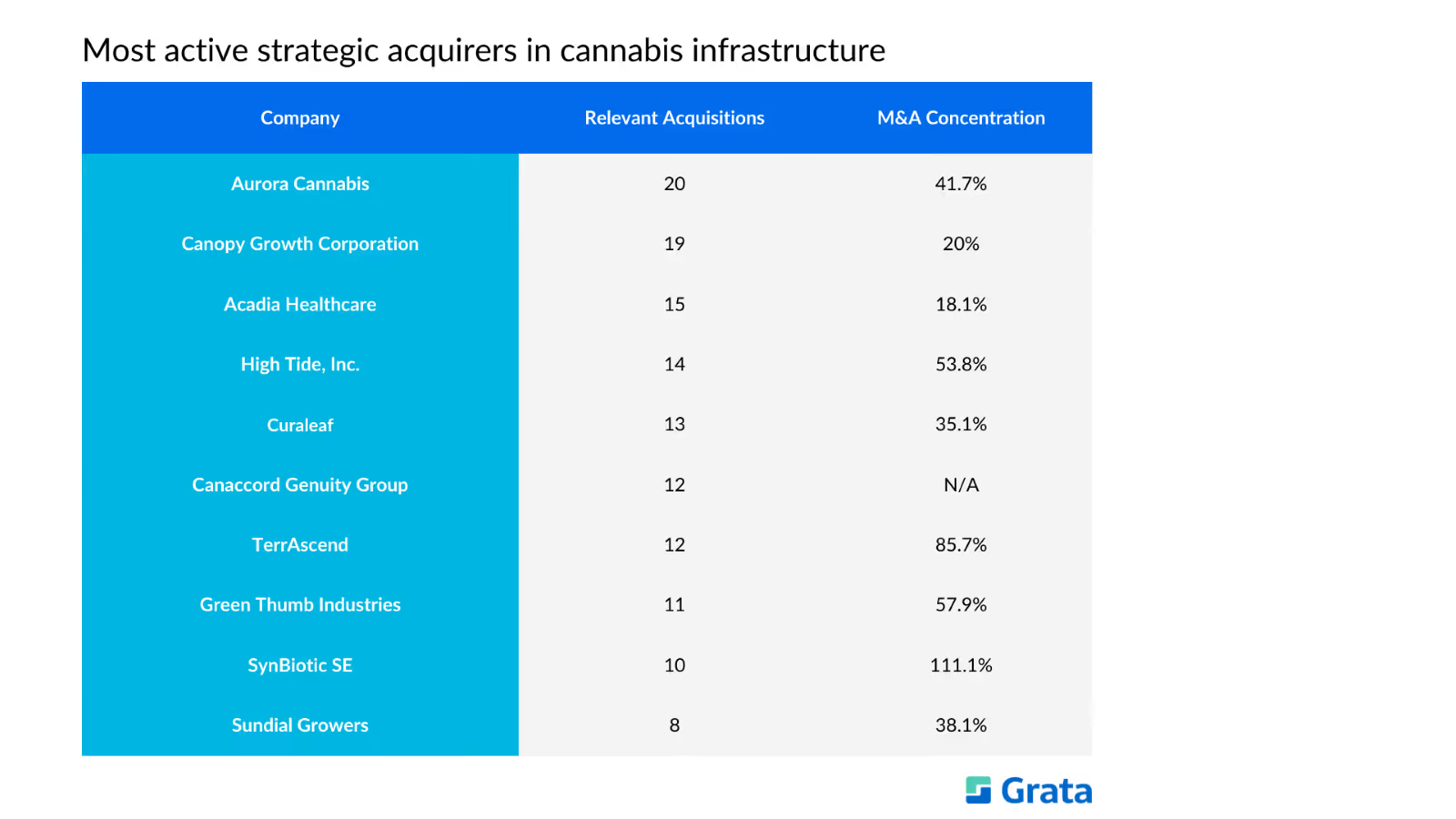

Most Active Strategic Acquirers

Source: Grata

Aurora Cannabis is the most active strategic acquirer in the cannabis infrastructure space. Medical cannabis companies account for the vast majority of its acquisitions.

Cannabis Infrastructure Industry Overview

Market Distribution

Geography

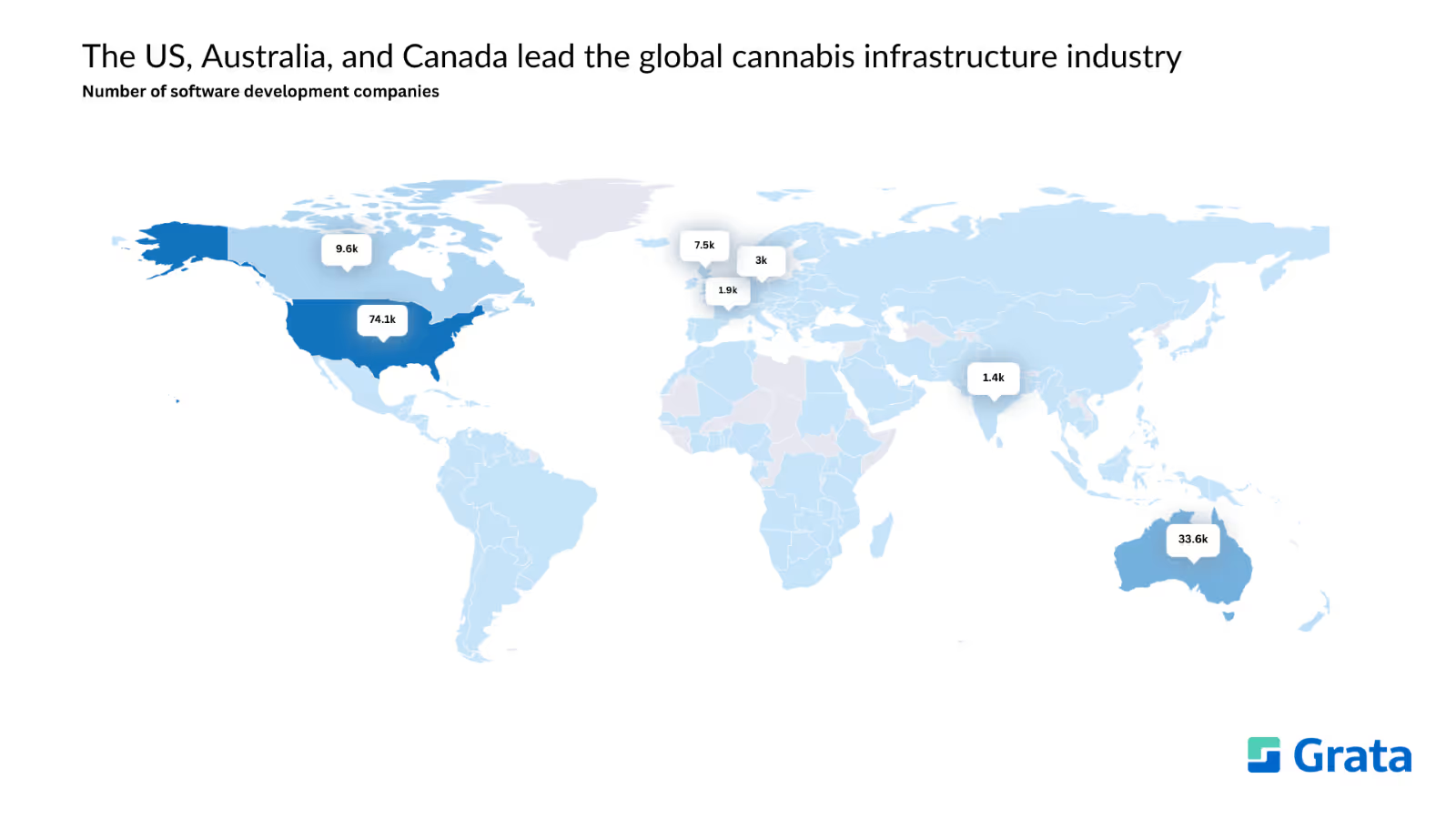

The Global Market

Source: Grata

The US, Australia, and Canada are the top three countries for cannabis infrastructure companies. Yet navigating legal nuances continues to be sticky business for cannabis players across the board.

In the US, for example, the Drug Enforcement Agency's move to reschedule marijuana from a Schedule I classification to a Schedule III last year didn’t bring as much regulatory clarification as industry players had hoped. Now, with the Trump administration introducing new complexities, the future of the US’ federal cannabis policy is even more hazy.

Banking and payments also continue to pose a critical challenge for US-based cannabis companies. The SAFER Banking Act, which would provide a legal framework for banks and financial organizations to serve cannabis businesses in states where the substance is legal despite the federal ban, is currently pending in the Senate.

Marijuana is legal for medical and recreational use across Canada, but each province sets its own age limit for purchase and possession. This ranges from 18 in Alberta to 21 in Quebec. There are also strict limits on how much cannabis an adult can possess, the THC content in products, and where cannabis products are allowed to be used.

In Australia, medical marijuana is legal at the federal level; recreational use is illegal but decriminalized. Similar to the US, recreational marijuana regulations vary by territory.

Dealmakers interested in cannabis infrastructure businesses anywhere in the world must be diligent about staying current on local and federal regulations in their market of interest.

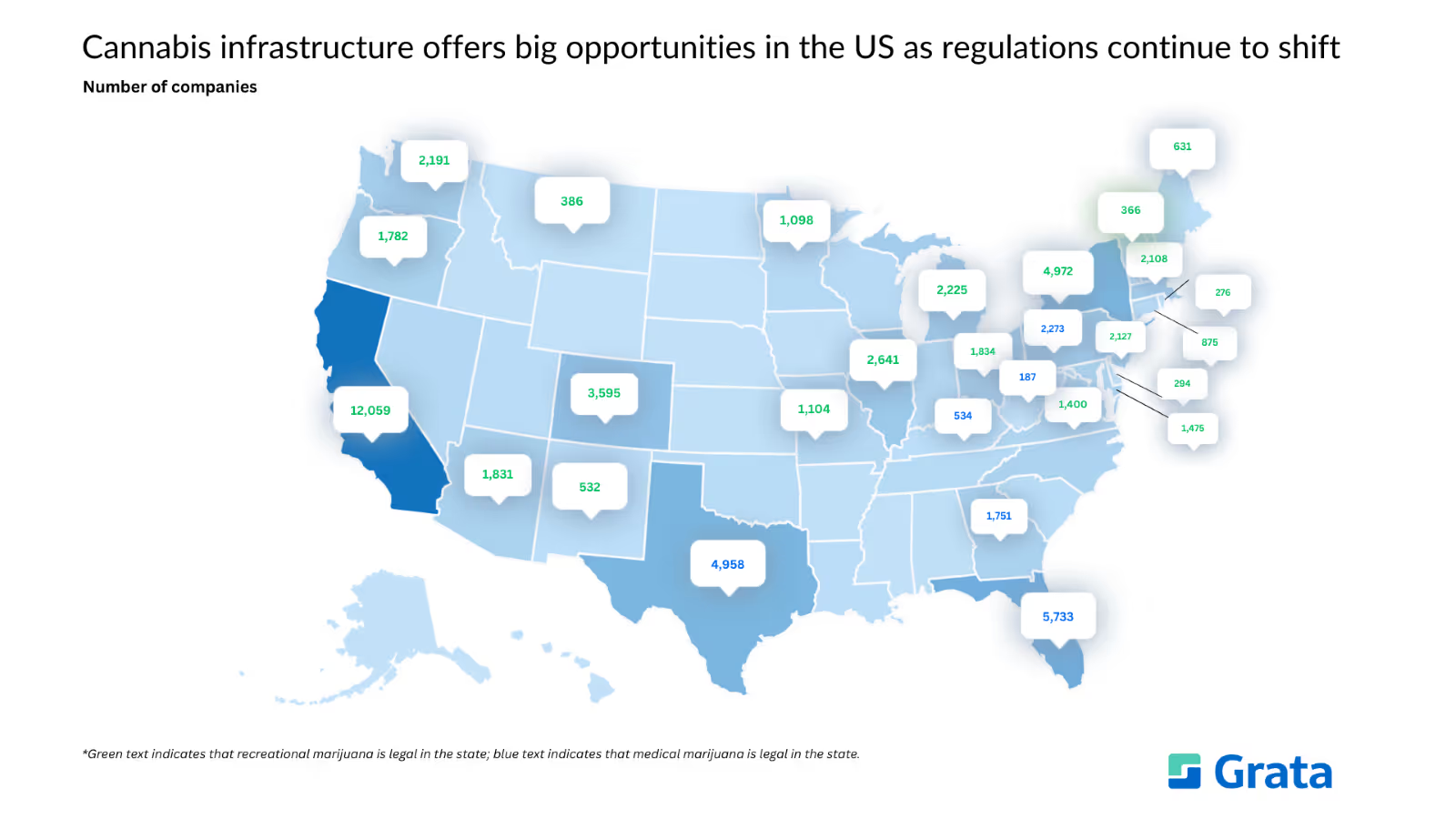

The US Market

Source: Grata

Dealmakers focused on the US have a growing number of geographic markets to explore as more states loosen their cannabis restrictions. Marijuana is currently legal for medical use in 40 states and recreational use in 24 states.

The New York and Ohio markets, in particular, are seeing robust expansion and job growth as they build out their legal footprints. Dealmakers should consider targeting states where recreational marijuana is newly legal, as fewer licenses and less competition could lead to higher profits.

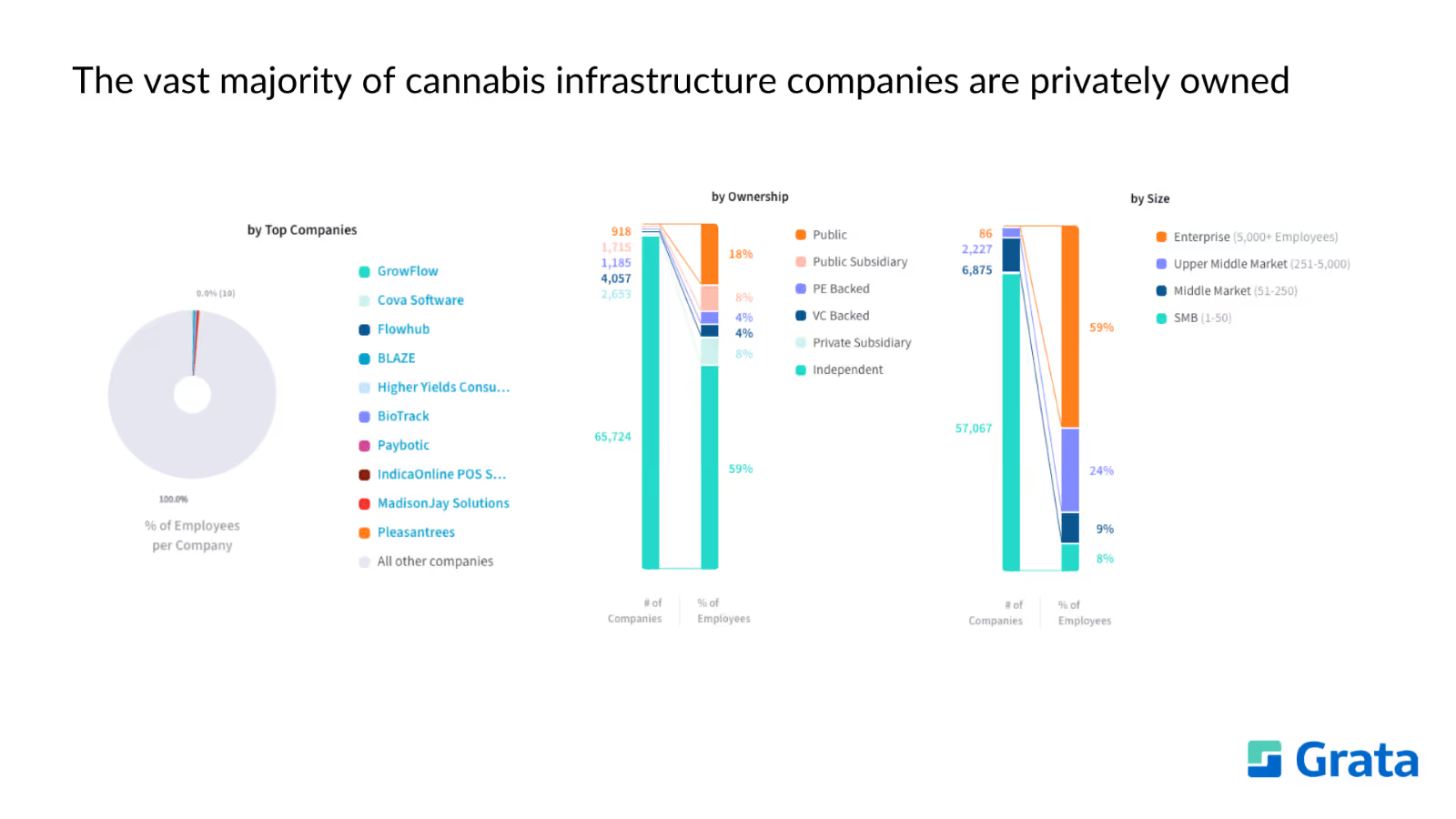

Ownership

Source: Grata

Privately owned companies comprise 75% of the cannabis infrastructure industry. Currently, there are nearly 66,000 independent companies in the space that are ripe for acquisition.

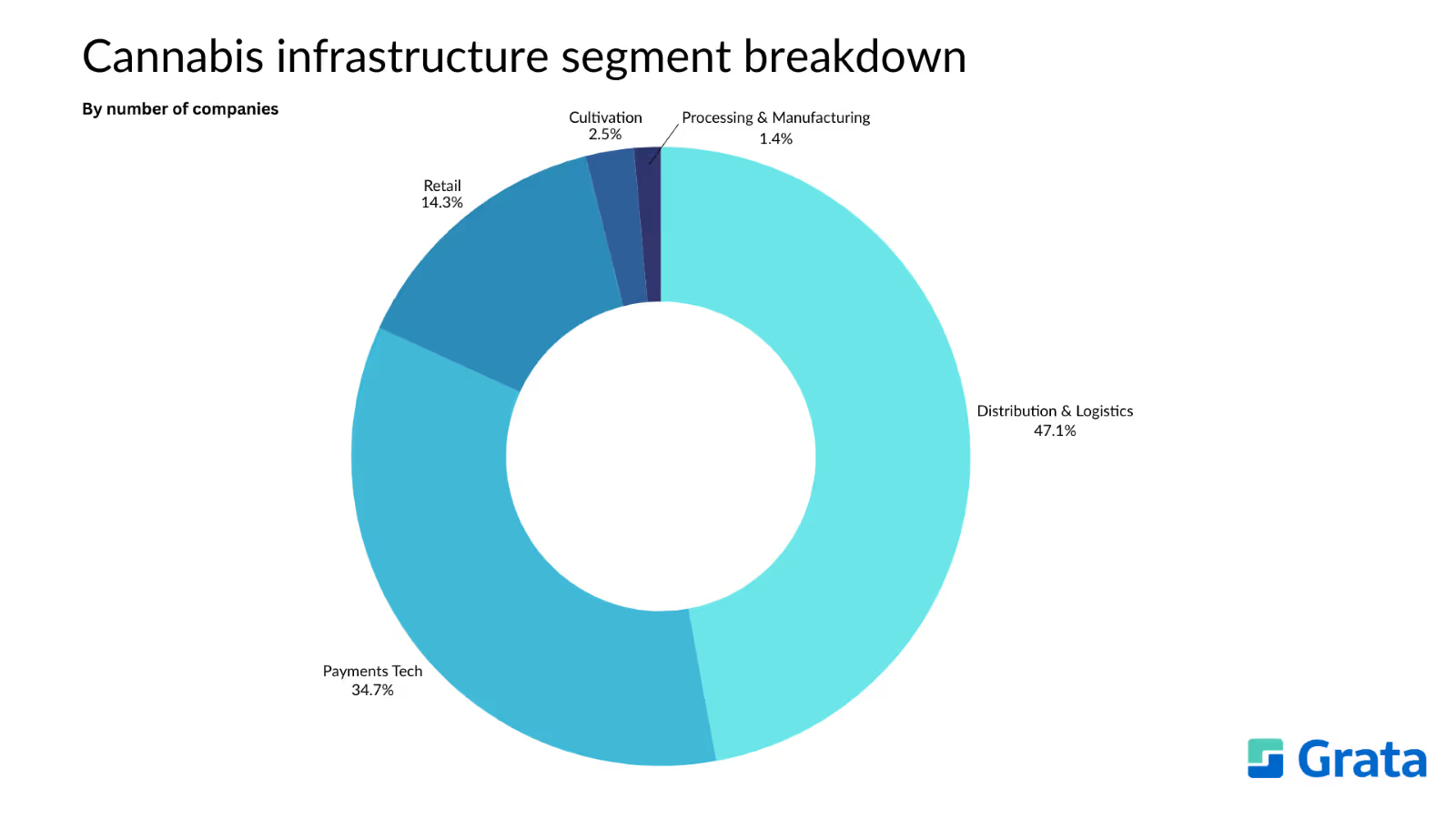

Segment Distribution

Source: Grata

This report focuses on the following segments of the cannabis infrastructure industry. Grata users can see curated lists of some of the companies used to create each segment by clicking the links below.

While companies in the cannabis industry generally see fairly high revenue, profitability continues to be an issue. This is because companies in the space are hamstrung by a number of complex challenges, including:

Inconsistent regulations. As mentioned in the Industry Overview section, cannabis legality varies widely by country, state, and territory. Companies in the industry have to navigate all of the nuanced rules across licensing, marketing, supply chain management, and more — which adds significant overhead and operational expenses.

High taxes. In the US, cannabis is still an illegal substance under federal law. That prevents businesses operating in states where cannabis is legal from deducting most of their standard expenses (rent, payroll, etc.). As a result, effective tax rates can exceed 50%.

Intense competition in a crowded market. Because the barrier to entry in states where cannabis is legal is quite low, the industry is seeing highly saturated pockets — particularly in the retail sector. The subsequent price wars have led to a sizable drop in average retail prices for cannabis products, shrinking profit margins. For example, California saw the average retail price fall by 32% between 2021 and 2023.

Restricted access to traditional banking services. As mentioned in a previous section, illegality at the federal level prevents most cannabis companies from accessing traditional financial institutions. This forces many retailers to operate on a cash-only basis, which presents a security risk. It also makes approval for business loans and lines of credit difficult to get.

A robust illicit market. High taxes and complex regulations make legal cannabis notably more expensive than illegal products. Even in states where the substance is legal, the illicit market continues to thrive, undercutting business for licensed dispensaries.

As a result, factions of the industry are flagging. The cannabis industry cut more than 15,000 jobs in 2024 even as sales surpassed $30B. Many smaller players are struggling to make ends meet. This is leading to a period of consolidation in the market, as PE firms and larger players swoop in to acquire distressed assets and underperformers. This could be an appealing avenue for dealmakers looking to streamline operations in the cannabis space.

Cannabis Infrastructure Private Comparables

Source: Grata

But even with the industry’s high-level challenges, certain pockets are thriving. Cannabis product sales in the US continue to grow, with projections showing a total of $45B in 2025. Dealmakers interested in the retail end of cannabis operations should look to areas that have recently legalized recreational cannabis, as those markets will be less saturated.

Rising demand for cannabis products around the world will lead to higher demand for services along the supply chain. Private companies in the distribution & logistics sector are seeing explosive growth, as noted in the table above. These companies also tend to see the highest amount of revenue, on average.

Naturally, cannabis processing & manufacturing companies — which take the marijuana plant and create various products from it — are also gaining momentum.

Dealmakers could find opportunities to establish themselves as leaders in the cultivation sector. It’s one of the smallest spaces in the industry, and its average revenue is comparatively modest, but it is also seeing consistent growth with little notable capital raised.

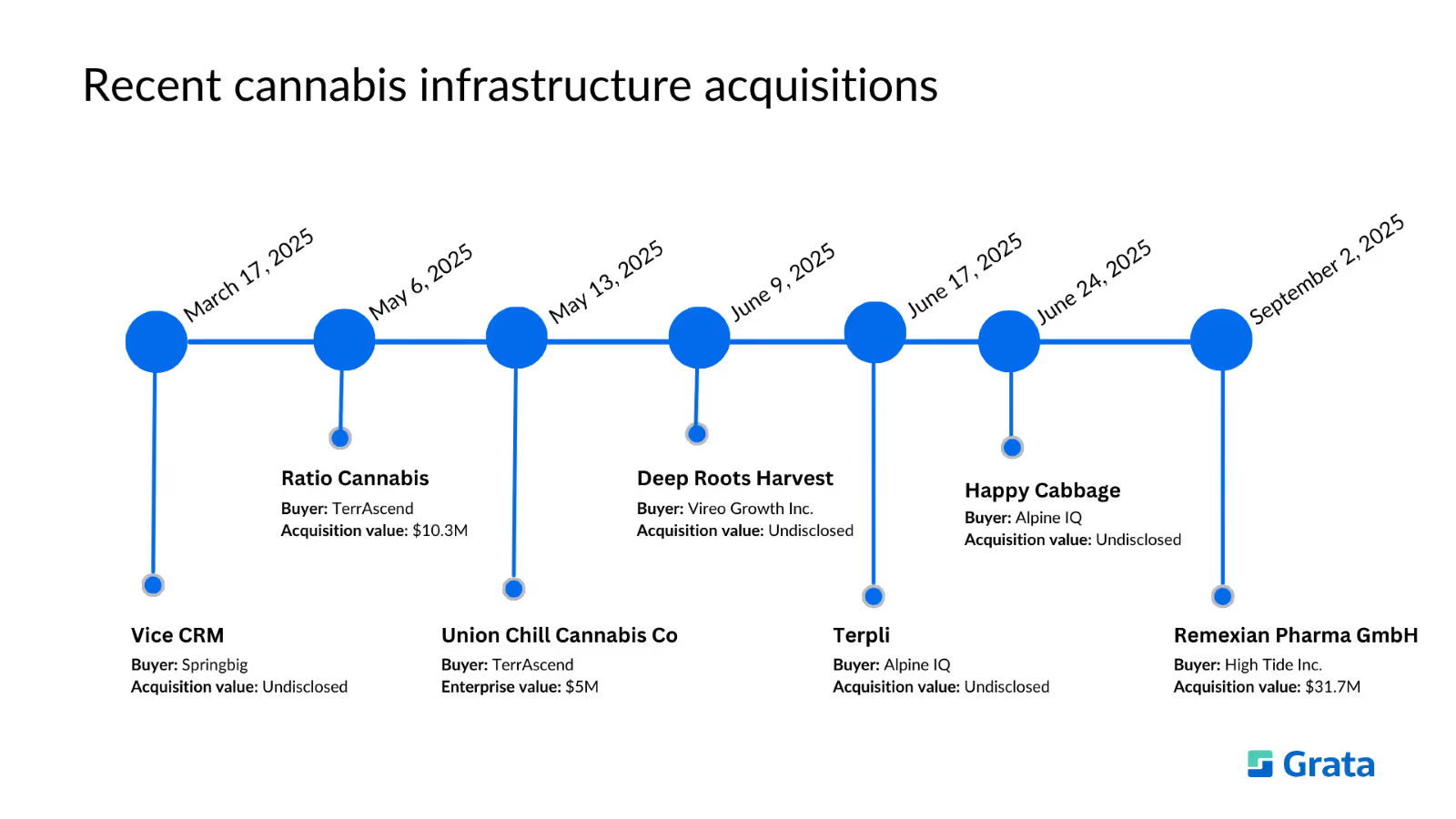

Notable Acquisitions in the Cannabis Infrastructure Industry

Source: Grata

Springbig Acquires Vice CRM

In March, Springbig, a company offering loyalty marketing and communications software for cannabis dispensaries, acquired Vice CRM for an undisclosed amount. Vice CRM is a mobile marketing platform that enables SMS and MMS marketing automations for regulated industries.

If you’re an investor interested in companies similar to Vice CRM, try these:

Learn more about this acquisition — or any of the others listed below — anytime, anywhere using the latest version of the Grata Go mobile app. Get all of the ownership and investment data you need right in the palm of your hand.

TerrAscend Purchases Ratio Cannabis

TerrAscend, a vertically integrated cannabis company, purchased Ohio-based Ratio Cannabis at a valuation of $10.3M in May. Ratio offers an online system for caregivers to order medical cannabis products on behalf of their patients.

If you’re an investor interested in companies similar to Ratio Cannabis, try these:

TerrAscend quickly followed with its acquisition of Union Chill Cannabis, also in May. Union Chill is a women-owned cannabis retailer based in New Jersey. It was valued at $5M at the time of the deal.

If you’re an investor interested in companies similar to Union Chill Cannabis Co, try these:

Vireo Growth, which cultivates, processes, and distributes medical and recreational cannabis products, acquired Deep Roots Harvest in June. Deep Roots Harvest produces and sells a variety of cannabis strains, pre-rolls, edibles, and other cannabis products. Financial terms of the deal were not disclosed.

If you’re an investor interested in companies similar to Deep Roots Harvest, try these:

Alpine IQ, which offers a suite of marketing, analytics, and employee engagement software for companies in regulated industries, purchased Terpli in June for an undisclosed amount. Terpli is a Washington, D.C.-based company that provides AI-powered recommendation and personalization services for cannabis retailers.

If you’re an investor interested in companies similar to Terpli, try these:

Only a week later, Alpine IQ completed its acquisition of Happy Cabbage, which offers revenue optimization, inventory management, and customer engagement solutions for companies operating in the cannabis industry. Terms of the deal were undisclosed.

If you’re an investor interested in companies similar to Happy Cabbage, try these:

Retail cannabis corporation High Tide purchased Remexian Pharma GmbH, a Germany-based pharmaceutical company specializing in importing and distributing medical cannabis, for $31.7M. This is the second acquisition for High Tide in 2025, following its purchase of Purecan GmbH, a pharmaceutical wholesaler, in January.

If you’re an investor interested in companies similar to Remexian Pharma GmbH, try these:

Hundreds of live deals and active mandates are being showcased on the Grata Deal Network. Here are some examples of mandates related to the cannabis infrastructure industry (Grata users can see the deals directly in the Grata platform using the links below):

If you’re interested in these deals and you want to see more, register to learn more here.

Are you a sell-side advisor interested in generating inbound leads for your data center infrastructure deal? Get started here.

Cannabis Infrastructure Conferences

Grata makes it easy for dealmakers to find conferences, events, and trade shows in their industries. See attendee lists so you can set up meetings beforehand and make the most of your travel time. Check out which companies attended past events to find more potential targets.

Here are a few of the events related to the cannabis infrastructure industry that dealmakers can find and track in Grata:

Get the Most Out of the Playbook

If you’re an investor interested in making moves in the cannabis infrastructure space, Grata can help you put the insights in this article into action.

From in-depth market research to sourcing to pipeline management and relationship nurturing, Grata’s end-to-end dealmaking platform streamlines your workflows so that you can close more deals.

From market trends to career advice, Grata’s content fuels smarter decisions.

Data

Energy/Infrastructure

Hidden Gems: Actionable, Undiscovered Opportunities in IT Infrastructure

Learn about the undiscovered IT infrastructure opportunities in the Grata platform. Explore trends in ownership, market segments, and emerging M&A opportunities.

Why Proprietary Deal Flow Is Getting Harder — and How Leading Teams Are Adapting

Proprietary deal flow is getting harder as generalist AI closes the access gap. See how verified private-market data and Seller Intent help dealmakers source before the competition does.

The New Deal Team: How AI Is Changing Every Role in M&A

AI is reshaping every role on the M&A deal team — from analyst to partner. Here's what that means for the firms building for the next generation of dealmaking.

Hidden Gems: Actionable, Undiscovered Opportunities in the HVAC Industry

Discover 79 undiscovered HVAC companies with high Seller Intent scores. See ownership, geographic, and sector breakdowns from Grata's proprietary private market data.

.webp)

.png)

.png)

.webp)